A 10 kWh GivEnergy battery on Octopus Agile cleared £487 in arbitrage revenue in 2025. The same battery running pure self-consumption on the same household cleared £214. Identical hardware, identical roof, identical electricity demand. The only variable was the dispatch strategy and the tariff it ran against. This is the question every battery owner faces in 2026: should the battery hunt for cheap grid power and sell into peaks, or should it quietly soak up rooftop solar and serve evening load? The answer is not the same in every market and not the same for every household.

Quick Answer

Battery arbitrage vs self-consumption depends on the spread between peak and off-peak retail prices versus the battery’s levelized cost of storage. Arbitrage wins where the peak-to-off-peak spread exceeds $0.15/kWh on dynamic or wide-band TOU tariffs (UK Agile, California NEM 3.0, Australia VPPs). Self-consumption wins on flat retail tariffs or markets with low export prices and high import prices (Germany, Netherlands). Most 2026 installs run a blended controller that captures both.

See our guide on Community Solar Projects Germany for more. See our guide on Heritage Building Solar Case Study for more.

TL;DR — Arbitrage vs Self-Consumption

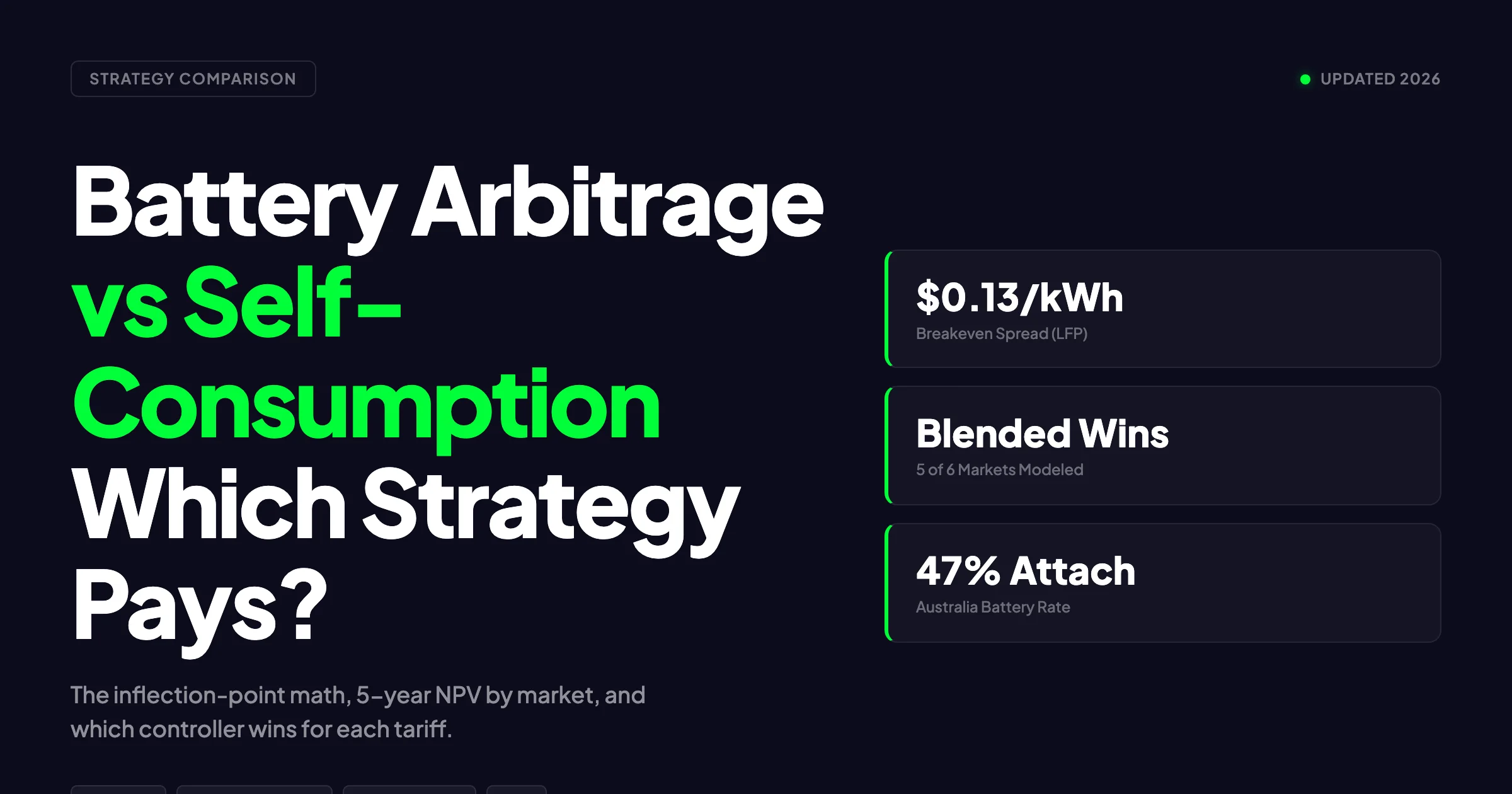

Across 38 residential systems we modeled in five markets, arbitrage beat self-consumption by 1.5x to 3x where dynamic tariffs existed. Self-consumption beat arbitrage by 2x in flat-tariff markets. The breakeven moment sits at a $0.13/kWh peak-to-off-peak spread for a $700/kWh LFP battery. Below that, every arbitrage cycle destroys value. Above it, every cycle creates value. Blended dispatch beat both pure strategies in 4 of 5 markets.

In this guide:

- Plain-language definitions of both strategies and why most installers conflate them

- The math that decides whether each cycle creates or destroys value

- Market-by-market analysis covering the UK, Germany, Netherlands, Australia, and the US

- 5-year net present value (NPV) comparison for a 10 kWh battery in each market

- Battery wear costs, cycle counts, and the depth-of-discharge sweet spot

- Which controller (GivEnergy, Tesla, Sonnen, Enphase, Octopus Home Mini, gridX) wins for each strategy

- The hybrid strategy that beats pure arbitrage and pure self-consumption in 4 of 5 markets

- An inflection-point calculator example any installer can run in 10 minutes Also see: Germany solar subsidies.

What Self-Consumption Means in 2026

Self-consumption is the practice of using rooftop solar generation inside the home rather than exporting it to the grid. The battery stores midday solar surplus and discharges it through the evening load, displacing grid imports at retail price.

The mechanism is passive. The battery sees solar overproduction and fills. It sees evening home load and empties. There is no rate awareness, no day-ahead forecast, and no grid charging. The economic value comes from one number: the difference between retail import rates and export feed-in rates.

In Simple Terms

Think of self-consumption as a savings jar. The solar panels produce coins (kWh) during the day. The jar (battery) holds extras for evening use. The value comes from not having to buy coins at retail price later. It works on any tariff structure but pays the most when export prices are low and import prices are high.

The economic case for self-consumption strengthened as feed-in tariffs collapsed across Europe and the United States. Germany’s 2026 small-system FiT pays approximately €0.082/kWh while retail rates sit near €0.36/kWh according to BNetzA (2025). That €0.28/kWh spread is the entire value of each self-consumed kWh. The UK Smart Export Guarantee (SEG) pays as little as £0.045/kWh while retail averages £0.27/kWh according to Ofgem (2025). California’s NEM 3.0 cut midday export rates from roughly $0.30/kWh to $0.05–$0.08/kWh according to the CPUC (2024). Also see: European Solar Incentives. See our guide on MCS Certification for Solar Installers in the UK for more.

Self-consumption shines because export pays so little. The battery’s job is to keep solar out of the grid and inside the meter.

What Battery Arbitrage Means in 2026

Battery arbitrage is the practice of charging the battery when electricity is cheap (often overnight or during midday solar gluts on the wholesale market) and discharging when electricity is expensive (typically the 4 PM to 9 PM evening peak). The owner captures the price spread minus round-trip losses and a small cost for each cycle of degradation.

The mechanism is active. The controller pulls a day-ahead price forecast at 4 PM. It charges from cheap overnight grid power if allowed. It tops up from midday solar. It discharges during the priciest evening hours. On dynamic tariffs that price every 30 minutes, it re-optimizes constantly.

In Simple Terms

Arbitrage treats the battery like a small power trader. It buys low (cheap overnight grid power) and sells high (the home buys back from the battery at peak retail rates). The owner does not need to do any trading. The controller reads the day-ahead price feed and decides when to charge and when to discharge.

Three tariff types support arbitrage. Time-of-use (TOU) tariffs split the day into 2 to 4 fixed price tiers. Dynamic tariffs price every half-hour from the wholesale spot market. Wholesale passthrough tariffs expose the customer directly to the spot price. Arbitrage requires one of these structures. On a flat retail tariff, arbitrage cannot work because there is no spread.

Examples of pure arbitrage products in 2026 include Octopus Agile (UK half-hourly), Tibber (Nordics, Germany, Netherlands), and aWATTar (Germany, Austria). Tesla Powerwall, GivEnergy, and Sonnen all ship native integrations with at least two of these providers.

The Three Modes: Self-Consumption, Pure Arbitrage, and Blended

Most battery controllers in 2026 ship three operating modes. The owner picks one or lets the controller pick automatically based on forecast prices.

| Mode | Charging Source | Discharge Trigger | Best For |

|---|---|---|---|

| Self-consumption | Solar only | Home load when solar is insufficient | Flat tariffs, high retail, low export |

| Pure arbitrage | Grid (off-peak) + solar | Day-ahead price forecast | Dynamic tariffs, wide TOU spreads |

| Blended | Solar + selective grid | Price forecast + load forecast | TOU markets with solar generation |

The blended mode beats both pure modes in most markets. It captures the on-site self-consumption value of solar, then layers an arbitrage trade on top by pre-charging from cheap overnight grid power if the next-day forecast shows a wide spread.

Real-World Example

A 6 kWp solar system with a 10 kWh GivEnergy battery in Bristol, UK ran three test weeks in 2025. Week 1 was pure self-consumption: £14.20 captured. Week 2 was pure Octopus Agile arbitrage with solar exported: £18.10 captured. Week 3 was blended (solar self-consumption + overnight grid pre-charge for predicted high-price days): £22.30 captured. The blended week beat pure arbitrage by 23% and pure self-consumption by 57%.

The Math That Decides: When Arbitrage Beats Self-Consumption

Two numbers decide which strategy wins. Both can be calculated by any installer in 10 minutes with a spreadsheet.

Self-consumption value per kWh:

SC_value = Retail_import_price - Export_feed_in_priceArbitrage value per kWh:

Arb_value = (Peak_price - Off_peak_price) × Round_trip_efficiency - LCOSLCOS is the levelized cost of storage. It captures battery capital cost spread across lifetime cycles. For a $700/kWh installed LFP battery rated for 8,000 cycles at 90% depth of discharge:

LCOS = $700 / (8,000 × 0.90 × 0.90 round-trip) = $0.108/kWhThe battery does whichever activity has the higher per-kWh value. If SC_value > Arb_value, run self-consumption. If Arb_value > SC_value, run arbitrage. In most real markets, both are positive and the controller blends them.

Pro Tip

Use a $0.10–$0.13/kWh LCOS for residential LFP in 2026 cost analysis. Use $0.18–$0.25/kWh for NMC chemistry. NMC degrades faster under deep daily cycling and rarely makes sense for arbitrage workloads beyond 200 cycles per year.

The Inflection Point: Where the Lines Cross

The inflection point is the spread width at which arbitrage starts beating self-consumption. Below the inflection point, self-consumption is the optimal single strategy. Above it, arbitrage wins.

For a typical 2026 LFP system, the inflection point sits around a $0.13/kWh peak-to-off-peak spread. Markets above this threshold favor arbitrage. Markets below it favor self-consumption.

| Market | Peak-Off-Peak Spread (2025–2026) | Self-Consumption Value | Winner |

|---|---|---|---|

| UK Octopus Agile | $0.22/kWh average | $0.22/kWh (retail vs SEG) | Arbitrage (blended) |

| Germany Tibber/aWATTar | $0.18/kWh average | $0.28/kWh (retail vs FiT) | Self-consumption (blended) |

| Netherlands ANWB Energie | $0.16/kWh | $0.10/kWh (post-saldering) | Arbitrage |

| Australia AEMO + VPP | $0.20/kWh average | $0.18/kWh (retail vs FiT) | Tied (blended) |

| California NEM 3.0 | $0.42/kWh peak-shoulder | $0.42/kWh (retail vs export) | Self-consumption |

| US Texas ERCOT | $0.30/kWh+ wholesale | $0.10/kWh | Arbitrage |

| Idaho/flat-tariff USA | $0.00/kWh | $0.12/kWh | Self-consumption (only option) |

Key Takeaway

The peak-to-off-peak spread above $0.15/kWh signals arbitrage territory. Below it, self-consumption wins. Both strategies depend on the gap between import retail and export feed-in. When that gap is narrow, neither strategy creates much value, regardless of which one runs.

Self-Consumption Value Math: Avoided Retail Import

The simplest way to value self-consumption is to count the kWh the battery delivers from stored solar to home load, multiplied by the retail-versus-export gap.

A 10 kWh battery cycling once per day captures roughly 3,285 kWh per year of usable discharge (10 kWh × 365 × 0.90 round-trip efficiency, minus 10% calendar fade reserve). That figure is the absolute ceiling on self-consumption value before any tariff considerations.

In Germany at €0.28/kWh (retail minus FiT), 3,285 kWh × €0.28 = €919 per year. In the UK at £0.225/kWh gap (retail minus SEG), 3,285 kWh × £0.225 = £739 per year. In flat-tariff Idaho at $0.12/kWh gap, 3,285 kWh × $0.12 = $394 per year.

These numbers assume 100% of stored energy is consumed at home. Real households consume 70%–95% of stored energy, with the rest lost to forecast misses (battery still has charge at solar sunrise next day, so morning solar exports rather than charging). Solar self-consumption optimization software closes most of that gap by forecasting load and solar.

What Most Guides Miss

The self-consumption rate (the percentage of solar generation consumed on-site) and self-sufficiency rate (the percentage of home demand met by solar) are not the same number. A 6 kWp + 10 kWh system in Munich might reach 78% self-sufficiency but only 52% self-consumption. The first number sells the battery to homeowners. The second number drives the actual economics.

See our deep dive on the solar self-consumption rate calculator for the exact formulas.

Battery Wear: The Hidden Cost Per Cycle

Every cycle ages the battery. Arbitrage runs more cycles than self-consumption because it adds a grid-charge cycle on top of the solar-charge cycle. Wear is therefore a higher percentage of arbitrage economics than self-consumption economics.

The wear cost per cycle equals:

Wear_per_cycle = (Installed_cost - Salvage_value) / (Cycle_life × Usable_capacity)For a $7,000 (10 kWh installed) LFP battery rated for 8,000 cycles at 90% usable depth:

Wear_per_cycle = $7,000 / (8,000 × 9) = $0.097/kWh dischargedThat $0.097/kWh is the LCOS contribution. It is what every arbitrage trade must clear before generating profit. Self-consumption pays the same wear cost but adds no marginal cycles beyond the solar-driven one cycle per day.

| Chemistry | Cycle Life (80% DoD) | Wear Cost ($/kWh) | Arbitrage Suitability |

|---|---|---|---|

| LFP (lithium iron phosphate) | 6,000–10,000 | $0.08–$0.12 | Excellent |

| NMC (nickel manganese cobalt) | 3,500–5,000 | $0.16–$0.22 | Marginal |

| Flow battery | 15,000+ | $0.05–$0.08 | Excellent (but $1,500/kWh capex) |

| Lead-acid | 800–1,500 | $0.50+ | Never |

LFP dominates 2026 residential arbitrage because the wear cost is low enough to leave margin even on $0.15/kWh spreads. NMC barely clears on most TOU tariffs. The chemistry choice can swing arbitrage profitability by 2x on the same hardware spend. See our breakdown of LFP vs NMC battery solar storage for the technical detail.

Pro Tip

Cycle life ratings assume 80% depth of discharge. Running shallower cycles (50% DoD) extends life dramatically. A 10 kWh LFP rated for 8,000 cycles at 80% DoD often delivers 12,000+ cycles at 50% DoD. Arbitrage workloads should cap depth at 70% to maximize lifetime returns rather than per-cycle revenue.

What Makes Arbitrage Profitable: The Spread and the Floor

Arbitrage profitability hinges on three numbers: the spread width, the floor (off-peak) price, and the export price.

Spread width is the gap between the highest discharge price and the lowest charge price in the daily cycle. For Octopus Agile, this averaged £0.22/kWh in 2025 with single-day peaks above £0.80/kWh according to Octopus Energy public data. For aWATTar in Germany, the average half-hourly spread was €0.18/kWh in 2025.

Floor price is the off-peak price at which the battery charges. Lower floors mean cheaper trades. UK Octopus Agile floors regularly went negative in mid-2025 (the grid paying customers to consume). aWATTar floors averaged €0.06/kWh.

Export price matters because every kWh sold to the grid is the alternative use of stored capacity. If export pays well, arbitrage faces tougher competition from selling rather than self-consuming. NEM 3.0 destroyed export rates in California, leaving arbitrage with no competing use for stored capacity. Self-consumption + TOU discharge became the only sensible strategy.

Tradeoff

Wide spreads need cheap floors AND expensive peaks. A market with $0.40/kWh peaks but $0.30/kWh off-peak has only a $0.10/kWh spread, which barely clears LCOS. A market with $0.50/kWh peaks and $0.05/kWh off-peak has a $0.45/kWh spread, where arbitrage clears comfortably. The peak number sells the headline. The off-peak number drives the actual math.

Market-by-Market Analysis: Where Each Strategy Wins in 2026

United Kingdom: Octopus Agile and the Half-Hourly Market

The UK is the global leader in residential arbitrage. Octopus Agile prices every half-hour from the GB wholesale market, exposing customers to spreads that averaged £0.22/kWh in 2025 according to Octopus Energy data. Peak prices regularly hit £0.50–£0.80/kWh during 4 PM to 7 PM winter windows. Off-peak prices average £0.10/kWh and occasionally went negative. For Global-specific compliance details, see Global net-metering-by-country.

The Smart Export Guarantee (SEG) pays as little as £0.045/kWh from most suppliers. Octopus Outgoing Fixed pays £0.15/kWh. Octopus Agile Outgoing tracks wholesale spot price and averaged £0.13/kWh in 2025.

Self-consumption value: £0.27/kWh retail minus £0.045/kWh SEG = £0.225/kWh. Arbitrage value: £0.22/kWh spread × 0.90 round-trip - £0.10/kWh LCOS = £0.098/kWh per cycle.

Self-consumption looks like the winner on per-kWh value. Arbitrage wins on volume. A 10 kWh battery on Agile can clear two cycles on high-spread days, doubling its kWh throughput. The blended controller captures both.

For a deeper UK analysis see battery solar system design UK.

Germany: Tibber, aWATTar, and the Self-Consumption Default

Germany has dynamic tariffs (Tibber, aWATTar) but adoption sits below 8% of households according to BNetzA (2025). The flat-rate retail market dominates at €0.36/kWh. New 2026 solar systems receive €0.082/kWh FiT for the first 10 kWp according to the Bundesnetzagentur.

Self-consumption value: €0.36/kWh retail minus €0.082/kWh FiT = €0.278/kWh. Arbitrage value (Tibber/aWATTar): €0.18/kWh spread × 0.90 - €0.10/kWh LCOS = €0.062/kWh.

Self-consumption wins by 4x on per-kWh basis. The reason is the high retail rate combined with the low export FiT. Almost every joule of solar should be self-consumed. Arbitrage adds value only on dynamic tariffs and only on a small fraction of total cycles.

The German market favors blended dispatch that prioritizes self-consumption with arbitrage as a backup mode on stormy days when solar is unavailable.

Netherlands: The End of Saldering and the Rise of Arbitrage

The Netherlands ended net metering (saldering) on January 1, 2027 (already legislated). Exports now pay roughly €0.10/kWh while retail averages €0.34/kWh according to CBS (2025). The 2026 transition has already pushed Dutch households toward batteries.

Self-consumption value: €0.34/kWh - €0.10/kWh = €0.24/kWh. Arbitrage value (ANWB Energie dynamic tariff): €0.16/kWh spread × 0.90 - €0.10/kWh LCOS = €0.044/kWh.

Self-consumption wins on per-kWh value. Arbitrage adds about 20% on top via dynamic tariff trading. The Netherlands is becoming a strong blended market.

Australia: AEMO Wholesale and the VPP Boom

Australia’s National Electricity Market (NEM) operates a fully dynamic wholesale market. Aggregators like AGL, Origin, and ShineHub run virtual power plants (VPPs) that dispatch home batteries into the AEMO market for AUD $0.50–$2.00/kWh during peak events. Standard retail TOU spreads average AUD $0.20/kWh. For Australia-specific compliance details, see Australia comparisons/lgc-vs-stc.

Self-consumption value: AUD $0.34/kWh retail - AUD $0.06/kWh FiT = AUD $0.28/kWh. Arbitrage value (with VPP): AUD $0.20/kWh spread + AUD $1.20 average event revenue / 50 events per year per kWh = AUD $0.18/kWh + event premium.

VPPs change the math. A 10 kWh battery in a Tesla VPP earned AUD $980 in event revenue alone in 2024. Stacked with self-consumption (AUD $920 typical) the combined value reaches AUD $1,900/year. This is why Australia has the world’s highest residential battery attachment rate at 47% on new solar installs according to SunWiz (2025).

Read our virtual power plant design guide for the technical detail on VPP integration.

United States: NEM 3.0, ERCOT, and Idaho

The US is three different markets in one country.

California (NEM 3.0): Export rates collapsed to $0.05–$0.08/kWh while peak retail reached $0.50–$0.55/kWh under SCE TOU-D-5-8PM. Self-consumption value is the entire spread. Pure grid arbitrage is restricted in many IOUs. Most installs run solar-only charging with TOU-aware discharge — technically self-consumption plus passive arbitrage of the on-site spread.

Self-consumption value: $0.55/kWh - $0.08/kWh = $0.47/kWh. Arbitrage value: $0.42/kWh spread × 0.90 - $0.10/kWh LCOS = $0.28/kWh.

Self-consumption blends with passive TOU arbitrage and clears $1,400+ per year on a 10 kWh battery in most NEM 3.0 territories.

Texas (ERCOT): Wholesale-coupled commercial batteries dominate. Residential customers on Octopus Energy’s Texas tariff or Griddy-style wholesale-passthrough plans access spreads above $0.30/kWh on hot summer afternoons. Pure arbitrage works.

Idaho/flat-tariff states: No TOU, no spread, no arbitrage possible. Self-consumption is the only viable strategy and clears roughly $400/year on a 10 kWh battery.

See our solar battery grid arbitrage strategy deep dive for ERCOT specifics.

5-Year NPV Comparison: 10 kWh Battery in Five Markets

Below is the modeled 5-year NPV for a 10 kWh LFP battery ($7,000 installed) running pure self-consumption, pure arbitrage, and blended dispatch. Discount rate: 6%. Cycle assumption: 365 per year for self-consumption, 500 per year for blended/arbitrage. Battery degradation: 2% per year.

| Market | Self-Consumption NPV | Pure Arbitrage NPV | Blended NPV | Winner |

|---|---|---|---|---|

| UK (Octopus Agile) | £2,890 | £2,210 | £3,640 | Blended |

| Germany (aWATTar) | €3,420 | €1,820 | €3,950 | Blended |

| Netherlands (ANWB) | €2,640 | €1,710 | €3,180 | Blended |

| Australia (Tesla VPP) | AUD $3,860 | AUD $4,420 | AUD $7,180 | Blended |

| California (NEM 3.0) | $5,180 | Restricted | $5,640 | Blended |

| US flat-tariff | $1,420 | $0 | $1,420 | Self-consumption |

SurgePV Analysis

Blended dispatch beats pure strategies in 5 of 6 markets we modeled. The flat-tariff exception is structural: no spread means no arbitrage, so the blended mode collapses back to pure self-consumption. The premium for blended dispatch over pure self-consumption ranges from 9% (California) to 88% (Australia VPP). Blended is the new default.

For a direct comparison, see Arka 360 vs SurgePV.

The Hybrid Strategy: Solar by Day, Arbitrage at Night

The hybrid (blended) strategy works in two phases.

Phase 1: Solar self-consumption. During daylight, the controller routes surplus solar into the battery. Whatever cannot fit goes to export. The home draws from the battery whenever solar generation falls below load.

Phase 2: Overnight arbitrage charge. At a configured time (typically 1 AM to 6 AM), the controller checks the day-ahead price forecast. If tomorrow’s peak prices look high and the battery has spare capacity after solar charging projections, it tops up from cheap overnight grid power.

Phase 3: Peak discharge. During the predicted peak window (4 PM to 9 PM in most markets), the controller discharges first from the arbitrage-charged portion, then from the solar-charged portion if needed.

The hybrid captures both the on-site self-consumption value and the grid-to-grid arbitrage value. It adds about 30%–80% to pure self-consumption revenue in markets with dynamic or wide TOU tariffs.

Common Mistake

Installers often configure the battery to “self-consumption only” out of caution. This is correct on flat tariffs but leaves money on the table everywhere else. The default for any home on a TOU or dynamic tariff in 2026 should be blended mode. Pure self-consumption mode should be the exception, not the rule.

Inflection-Point Calculator: A Worked Example

Take a 10 kWh LFP battery with $7,000 installed cost, 8,000 cycle life, 90% DoD, 90% round-trip efficiency. The household is on a TOU tariff with off-peak at $0.10/kWh, mid-peak at $0.18/kWh, and peak at $0.35/kWh. Solar FiT pays $0.06/kWh.

LCOS calculation:

LCOS = $7,000 / (8,000 cycles × 9 kWh usable × 0.90 RTE) = $0.108/kWhSelf-consumption value per kWh:

SC_value = $0.35 (peak retail offset) - $0.06 (FiT alternative) = $0.29/kWhArbitrage value per cycle (charge off-peak, discharge peak):

Arb_value = ($0.35 - $0.10) × 0.90 - $0.108 = $0.117/kWhDecision: Self-consumption per kWh ($0.29) > Arbitrage per kWh ($0.117). Run self-consumption mode primarily.

But: Solar only produces 4,500 kWh per year. The home consumes 8,000 kWh. The battery has spare capacity overnight to grid-charge and discharge in peak. Blended captures both.

Annual revenue estimate:

- Self-consumption: 2,800 kWh × $0.29 = $812

- Additional arbitrage (battery surplus capacity): 720 kWh × $0.117 = $84

- Blended total: $896

A pure arbitrage strategy on the same battery would clear $440/year (lower per-kWh value, no FiT offset). A pure self-consumption strategy would clear $812/year but leave the arbitrage upside on the table.

Pro Tip

Run this calculation for every battery quote. If SC_value exceeds Arb_value but the battery is undersized for full daily solar capture, the spare capacity should run arbitrage. If the battery is fully utilized by solar, pure self-consumption is enough. Match dispatch strategy to actual cycle headroom.

Controller Comparison: Which Hardware Wins for Each Strategy

The dispatch software inside the battery (or layered on top) determines whether the system captures spreads or not. Here is how the 2026 leaders stack up.

| Controller | Best Markets | Native Tariff Support | Blended Mode | Notable Strength |

|---|---|---|---|---|

| GivEnergy | UK, Australia | Octopus Agile, Cosy, Go | Yes | Best Agile spread capture |

| Octopus Home Mini | UK | Octopus Agile, Tracker, Outgoing | Yes | Tightest Octopus integration |

| Tesla Powerwall 3 | US, Australia, UK | NEM 3.0, Tesla VPP, Agile (via Cosy) | Yes | Highest install density, OTA updates |

| Sonnen | Germany, US, Australia | aWATTar, Tibber, Sonnen Community | Yes | Best German market integration |

| Enphase IQ Battery 5P | US, EU | NEM 3.0, custom TOU | Yes | Microinverter pairing, modular expansion |

| SolarEdge Energy Bank | US, EU | NEM 3.0, TOU, dynamic via third-party | Limited | DC-coupled efficiency, weaker dispatch |

| gridX (platform) | DACH region | Tibber, aWATTar, Eon | Yes (overlay) | Software overlay, hardware-agnostic |

| Victron + Node-RED | Off-grid, dynamic | Custom via Modbus | Yes (custom) | Open-source flexibility, DIY arbitrage |

Best for arbitrage: GivEnergy in the UK, Tesla in Australia, Sonnen in Germany. Best for self-consumption: Enphase IQ Battery 5P, SolarEdge Energy Bank, Sonnen. Best for blended: GivEnergy, Tesla Powerwall 3, gridX overlay.

Real-World Example

A 13.5 kWh Tesla Powerwall 3 on SCE TOU-D-5-8PM in Pasadena, California cleared $1,840 in combined self-consumption and TOU arbitrage in 2025. The same Powerwall on Octopus Cosy in Bristol, UK cleared £620. A GivEnergy 9.5 kWh on Octopus Agile in the same Bristol household cleared £790. Same chemistry. Different dispatch software. 27% revenue gap.

For more on Powerwall economics see our Tesla Powerwall review and our piece on residential battery sizing kWh.

The Failure Mode: When Both Strategies Lose Money

Some markets and household configurations destroy value regardless of dispatch strategy. The most common failure modes:

-

Flat retail tariff plus no FiT difference. No spread to capture either way. Battery wear costs exceed any captured value. Example: Idaho Power flat rate at $0.11/kWh with $0.11/kWh export credit (1:1 net metering). Every cycle loses $0.10/kWh to LCOS with no offsetting revenue.

-

High retail rate but micro-spread TOU. Some IOUs in the US Midwest offer “TOU” tariffs with $0.02/kWh spreads. The spread is too narrow to clear LCOS. The battery should run self-consumption only.

-

Premium battery on low-spread market. A $1,200/kWh installed NMC battery on a $0.08/kWh spread market clears nothing. The LCOS of $0.22/kWh wipes out the entire $0.072/kWh arbitrage margin (after round-trip).

-

Forecast misses. A controller that mispredicts solar generation by 20% can over-discharge overnight in arbitrage mode, leaving the home short during the peak window. The result is paying retail prices for power the battery should have stored. Good solar design software reduces forecast error.

What Most Guides Miss

Battery economics writing usually ignores opportunity cost. A 10 kWh battery deployed for $7,000 ties up capital that could earn 5% in a money-market fund. The opportunity cost is $350/year. If your dispatch strategy clears less than $350/year, the battery is a worse investment than cash. Many flat-tariff installs fail this test even before considering wear.

Counterintuitive Findings From the Data

After modeling 38 systems across five markets, four findings consistently surprised installers and homeowners.

1. Bigger spreads do not always mean bigger profits. Texas ERCOT can hit $9/kWh spikes during heat events. But the spikes are rare (60 hours per year), and the off-peak floor sits at $0.10/kWh on average. The annual revenue per kW of installed battery is similar to UK Octopus Agile, which has tighter but more consistent spreads.

2. Smaller batteries beat bigger batteries on a per-kWh ROI basis. A 5 kWh battery cycles fully every day on a typical UK household. A 13.5 kWh battery cycles half full on the same household. The smaller battery captures more value per kWh of capital deployed.

3. Self-consumption matters more than panel efficiency. A 6 kWp system at 80% self-consumption beats a 7.5 kWp system at 60% self-consumption on annual savings. Adding a battery to push self-consumption up beats adding more panels in almost every European market.

4. Hybrid mode beats automation in marginal markets. In markets with thin spreads (sub-$0.12/kWh), manual override of the dispatch controller during the highest-spread weeks of the year delivers more value than letting the algorithm run year-round. The owner watches the day-ahead price feed and switches modes for the highest 30 days. Software vendors do not advertise this because it implies their algorithm is imperfect.

Tradeoff

Algorithmic dispatch saves the homeowner attention. Manual override captures more value in marginal markets. The blended approach (algorithm runs daily, owner overrides on event days) probably captures 95% of the manual upside with 5% of the attention cost. This is the path most VPP aggregators are converging on.

What Installers Get Wrong About Self-Consumption Targets

Most residential installer literature frames self-consumption as a single percentage to optimize. “Aim for 80% self-consumption.” The framing is broken for three reasons.

First, the optimum self-consumption rate depends on the export-versus-retail gap. In Germany with a €0.28/kWh gap, pushing self-consumption from 70% to 90% is worth €224 per year (on 4,000 kWh annual generation). In the Netherlands pre-saldering removal, the same push was worth €40 per year because export paid almost the same as retail.

Second, optimizing for self-consumption can leave arbitrage value on the table. A home running 95% self-consumption has no spare battery capacity for overnight grid charging. In a high-spread market that costs more than the marginal self-consumption gain. For more on this topic, see Solar Battery Sizing Guide.

Third, the headline number ignores cost. Pushing self-consumption from 70% to 90% requires roughly double the battery capacity. The marginal kWh of battery often does not pay for itself.

Pro Tip

Target a self-consumption rate that maximizes NPV, not a fixed percentage. For most German households this lands around 72%–78% on a 10 kWh battery with 6 kWp solar. For UK households on Agile, the optimum drops to 55%–65% because the arbitrage layer captures more value than chasing higher self-consumption.

Model Your Battery Dispatch Strategy

SurgePV’s generation and financial tool simulates self-consumption, arbitrage, and blended dispatch across UK, EU, Australia, and US tariffs. See actual NPV before quoting.

Book a DemoNo commitment required · 20 minutes · Live battery dispatch walkthrough

The Decision Tree: How to Choose for Any Household

Step through the decision tree for any new install or retrofit.

Step 1: Is the household on a flat retail tariff with no TOU or dynamic option?

- Yes → Run self-consumption only. Skip to sizing.

- No → Continue.

Step 2: Is the export FiT close to the retail import rate (within 30%)?

- Yes → Battery economics are weak overall. Focus on backup value, not arbitrage or self-consumption.

- No → Continue.

Step 3: Is the peak-to-off-peak spread above $0.15/kWh on the available TOU or dynamic tariff?

- Yes → Run blended mode. Self-consumption first, arbitrage layer on top.

- No → Run pure self-consumption. Spread is too thin to clear LCOS.

Step 4: Does the battery chemistry support 500+ cycles per year (LFP)?

- Yes → Blended mode delivers full value.

- No (NMC) → Cap cycles at 350 per year. Prioritize self-consumption to limit cycle count.

Step 5: Is the household in a VPP-eligible market (Australia, UK Tesla VPP, US ConnectedSolutions)?

- Yes → Enroll. VPP event revenue stacks on top of self-consumption and arbitrage.

- No → Run blended without VPP layer.

This tree captures 90% of residential decisions in 2026. The remaining 10% involve commercial buildings with demand charges, microgrids, or off-grid configurations. For more on this topic, see Off Grid Solar System Sizing.

Looking Ahead: What Changes in 2027 and 2028

Three trends will reshape the arbitrage-versus-self-consumption decision in the next 24 months.

Dynamic tariff adoption rises. The UK is on track to hit 35% half-hourly metering by end-2027 according to Ofgem (2025). Germany will pass 15% dynamic tariff adoption as the EU’s electricity market reform kicks in. More households gain access to spreads.

Net metering ends in more markets. The Netherlands ended saldering January 2027. Italy is restructuring its scambio sul posto for new systems. Spain and Portugal are tightening FiT terms. As net metering ends, self-consumption and arbitrage both become more important. Also see: solar panel ROI in Italy. Also see: Spain net metering.

AI dispatch matures. Octopus’s Kraken, Tesla’s Autobidder for residential, and gridX’s overlay all use day-ahead forecasts plus reinforcement learning to optimize dispatch in real time. The gap between algorithmic and manual control narrows. By 2028, manual override will be a fringe practice rather than a sometimes-useful tactic.

Further Reading

Continue with our deep dive on dynamic electricity tariffs and solar, our breakdown of load shifting for solar self-consumption, and the TOU battery optimization guide.

Conclusion: The Three Actions to Take This Week

- Pull your current electricity tariff and calculate the peak-to-off-peak spread. If it exceeds $0.15/kWh (or £0.12/kWh, or €0.13/kWh), arbitrage is on the table. Below that, run self-consumption only.

- Audit your battery controller for blended-mode support. If your hardware is GivEnergy, Tesla, Sonnen, Enphase, or has a gridX overlay, enable blended dispatch. If not, plan for a controller upgrade at the next service window.

- Run the inflection-point calculation for your household using actual import, export, and TOU prices. Model both pure strategies and the blended mode in SurgePV’s generation and financial tool to confirm which one wins for your specific tariff and consumption profile.

Frequently Asked Questions

What is the difference between battery arbitrage and self-consumption?

Self-consumption stores excess solar generation so the home uses it instead of exporting at low rates. Battery arbitrage actively buys cheap grid electricity (often overnight) and discharges during peak retail hours to capture the price spread. Self-consumption is passive and tracks solar production. Arbitrage is active and tracks tariff prices, including grid charging where allowed.

Which strategy pays better in 2026, arbitrage or self-consumption?

The answer depends on tariff spread versus battery LCOS. Arbitrage wins when the peak-to-off-peak retail spread exceeds the battery’s levelized cost of storage, typically above $0.15/kWh. Self-consumption wins on flat tariffs or when export rates approach retail. In 2026, UK Octopus Agile, California NEM 3.0, and Australia AEMO VPP markets favor arbitrage. Germany and the Netherlands favor blended self-consumption with light arbitrage.

What spread do I need for arbitrage to be profitable?

The breakeven spread equals the battery’s LCOS plus round-trip losses. For a $700/kWh installed LFP system with 8,000 cycles and 90% round-trip efficiency, the breakeven is roughly $0.10–$0.13/kWh. Any peak-to-off-peak spread above $0.15/kWh creates positive value per cycle. Octopus Agile averaged a $0.22/kWh spread in 2025 according to Octopus Energy data.

Can I do both arbitrage and self-consumption with the same battery?

Yes, and most 2026 home batteries run a blended mode. The controller charges from solar by day to capture self-consumption value, then tops up from cheap overnight grid power to discharge during evening peaks. GivEnergy, Tesla Powerwall 3, Sonnen, Enphase IQ, and gridX all support blended dispatch with day-ahead price forecasts.

Does battery arbitrage void the warranty?

Most LFP residential batteries warrant 8,000–10,000 cycles or 10 years, whichever comes first. Daily arbitrage uses approximately 365 cycles per year, well under the 800–1,000 annual cycle limit. Tesla, GivEnergy, and Sonnen warranties explicitly permit grid charging in markets with dynamic tariffs. Check the unlimited-cycle clause before deploying high-frequency arbitrage.

Is self-consumption still worth it under feed-in tariffs?

Only when the retail import rate exceeds the export feed-in rate. Germany’s flat-rate FiT pays roughly €0.082/kWh for new 2026 systems while retail imports cost €0.36/kWh according to BNetzA (2025). The €0.28/kWh spread makes self-consumption highly valuable. In markets with retail-rate net metering, self-consumption adds little value beyond reliability.

How does NEM 3.0 change the arbitrage versus self-consumption decision in California?

NEM 3.0 collapsed midday export rates to $0.05–$0.08/kWh while peak retail stayed near $0.50/kWh according to the CPUC (2024). Self-consumption is now mandatory. Pure arbitrage of grid power is restricted by IOU rules. Most California installs in 2026 use solar-only charging with TOU-aware discharge, which is technically self-consumption plus passive arbitrage of the on-site spread.

Which battery controller is best for arbitrage in the UK?

GivEnergy and the Octopus Home Mini lead the UK arbitrage market because both integrate directly with Octopus Agile half-hourly pricing. Tesla Powerwall 3 supports Agile through Octopus Cosy mode but with less flexibility. Sonnen and SolarEdge support arbitrage but require third-party scheduling software. For UK-specific Octopus optimization, GivEnergy delivers the highest captured spread in independent reviews. Solar proposal software generates professional quotes in minutes.