Quick Answer

The five-year outlook through 2030 still totals roughly 12 GWdc of commercial additions. Wood Mackenzie reports about 160 GW of committed large-load interconnection requests in the US pipeline, equivalent to about 22% of the country's 2024 peak demand. Post-ITC equilibrium Source: SEIA / Wood Mackenzie US Solar Market Insight Q4 2025 and Q1 2026 commercial segment forecasts.

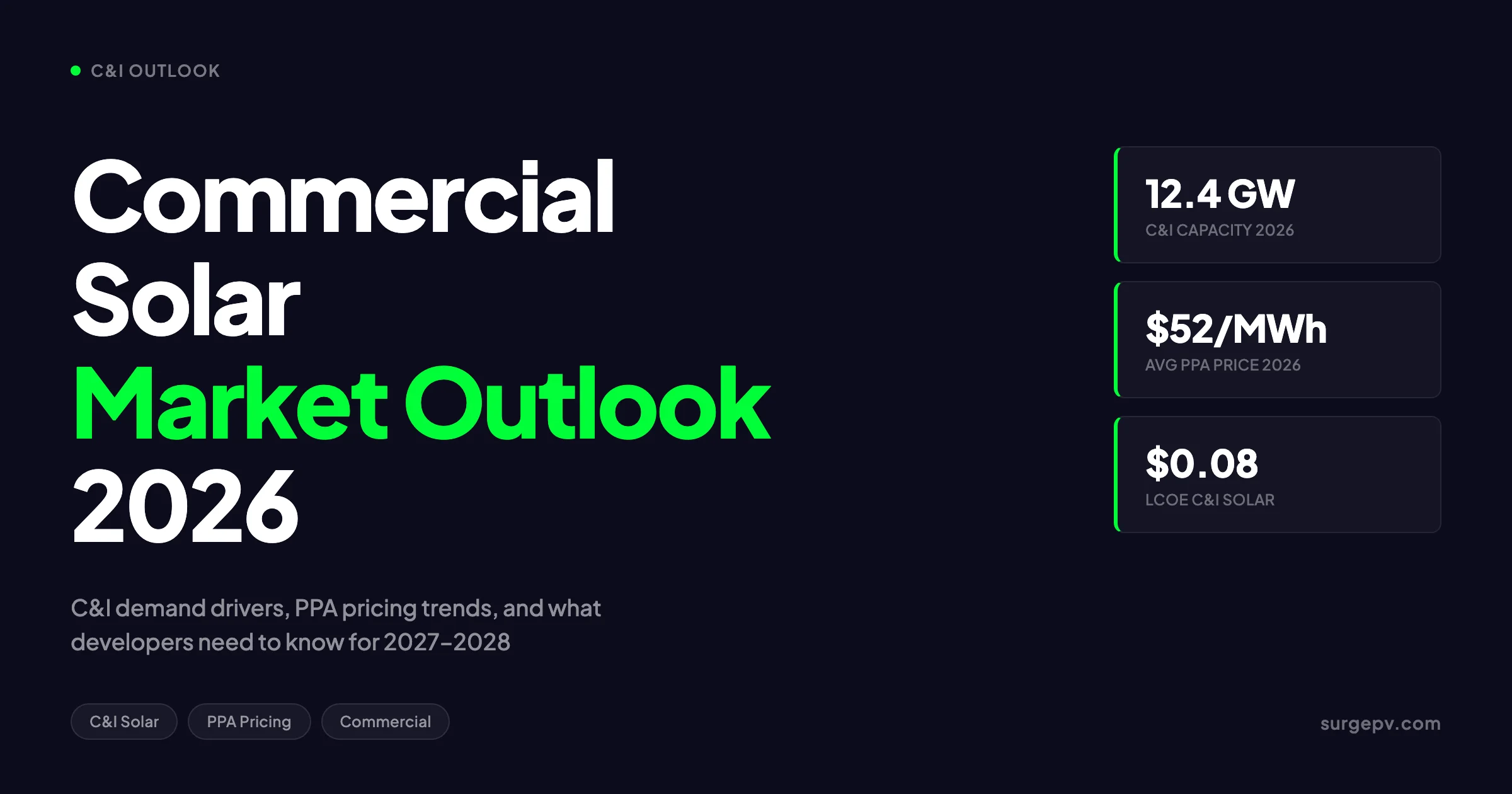

The commercial solar market is no longer driven by sustainability commitments. It is driven by power scarcity. AI data center load alone added roughly 160 GW of large-load interconnection requests to the US queue — about 22% of 2024 peak demand, per Wood Mackenzie — and corporate buyers signed 55.9 GW of clean energy PPAs globally in 2025 per BloombergNEF. Yet the commercial and industrial (C&I) onsite segment enters 2026 with a 4% downgrade to its five-year outlook, EPC labor shortages, and a 10% year-on-year jump in system pricing. For Global-specific compliance details, see Global net-metering-by-country.

The five-year outlook through 2030 still totals roughly 12 GWdc of commercial additions. Wood Mackenzie reports about 160 GW of committed large-load interconnection requests in the US pipeline, equivalent to about 22% of the country’s 2024 peak demand.

This guide covers the full commercial solar market outlook 2026 for installers, developers, and corporate buyers: capacity forecasts from SEIA and Wood Mackenzie, regional PPA pricing from LevelTen Energy, hyperscaler procurement strategy, the tax equity transition after direct pay, interconnection bottlenecks, and what to do in 2026 to land the projects that will close in 2027 and 2028. For the broader solar software context, see our related guides on solar shadow analysis software and commercial solar financing.

TL;DR — Commercial Solar Market Outlook 2026

US C&I solar to dip slightly in 2026 then grow 12% annually through 2030 per Wood Mackenzie. Global corporate PPAs at 55.9 GW in 2025 (BloombergNEF), down 10% but still the second-highest year on record. North America solar PPAs at $64.49/MWh (up 13% YoY); Europe at €55.05/MWh (down 13% YoY) per LevelTen Q1 2026. AI data centers drive 49% of global corporate clean energy deals. OBBBA sets a July 4, 2026 construction-start deadline to preserve 48E and 45Y tax credits. Texas hosts 40% of new US utility-scale solar and 25% of the data center pipeline.

In this guide:

- C&I solar snapshot 2026 — capacity, pricing, and the headline data points

- Demand drivers: AI data centers, onsite generation, corporate ESG, and reshoring

- PPA pricing trajectory by region through 2028

- Behind-the-meter versus offsite — when each makes sense

- What most commercial solar reports miss (the contrarian take)

- Financing models after the tax equity disruption

- Interconnection queue bottlenecks and grid constraints

- 2027 and 2028 outlook for C&I solar

- Practical implications for developers and installers

C&I Solar Snapshot 2026: Capacity and Pricing

Commercial and industrial solar in the United States installed approximately 2.0 GWdc in 2025 according to SEIA and Wood Mackenzie. The 2026 forecast sits around 1.8–2.1 GWdc — a soft year as California NEM 2.0 projects wind down and developers digest the One Big Beautiful Bill Act (OBBBA) tax credit changes. The five-year outlook through 2030 still totals roughly 12 GWdc of commercial additions.

Globally, the picture is bigger and more bullish. Wood Mackenzie reports about 160 GW of committed large-load interconnection requests in the US pipeline, equivalent to about 22% of the country’s 2024 peak demand. The US Energy Information Administration expects 43.4 GW of new utility-scale solar to come online in 2026 — a 60% jump over 2025 and the largest single-year addition in history.

US Commercial Solar Capacity Trajectory

| Year | C&I Installed (GWdc) | Annual Growth | Notes |

|---|---|---|---|

| 2023 | 1.8 | +5% | Pre-IRA momentum stabilizing |

| 2024 | 2.1 | +17% | California NEM 2.0 surge + IRA pull |

| 2025 (actual) | 2.0 | −5% | Tariff pressure begins |

| 2026 (forecast) | 1.8–2.1 | flat to −10% | California contraction; labor constraints |

| 2027 (forecast) | 2.2 | +10–15% | Recovery; Midwest/Southeast pickup |

| 2028 (forecast) | 2.5 | +13% | Hyperscaler onsite demand peaks |

| 2030 (target) | 3.0+ | +12% avg | Post-ITC equilibrium |

Source: SEIA / Wood Mackenzie US Solar Market Insight Q4 2025 and Q1 2026 commercial segment forecasts.

Commercial Solar PPA Pricing — Q1 2026

| Region | Market | Q1 2026 Solar PPA | YoY Change | Driver |

|---|---|---|---|---|

| North America (blended) | LevelTen index | $64.49/MWh | +13% | Hyperscaler demand, FEOC compliance |

| CAISO (California) | LevelTen | ~$75/MWh | +18% | Negative pricing risk, queue cost |

| ERCOT (Texas) | LevelTen | ~$58/MWh | +9% | Land availability, data center load |

| MISO (Midwest) | LevelTen | ~$62/MWh | +11% | Emerging market premium |

| Europe (P25 average) | LevelTen | €55.05/MWh (~$64.83) | −13% | Weak industrial demand, hybrid shift |

| UK | LevelTen | ~£52/MWh | −10% | Capacity Market interaction |

| Germany | LevelTen | ~€58/MWh | −12% | Negative pricing dominance |

| Spain | LevelTen | ~€38/MWh | −15% | Solar saturation, cannibalization |

Source: LevelTen Energy Q1 2026 PPA Price Index, North America and Europe editions.

Two markets, two stories. North American solar PPAs are now $7/MWh cheaper than blended PPAs and almost $15/MWh cheaper than wind — yet still 13% more expensive than a year ago. European solar PPAs have declined for five straight quarters as developers shift toward hybrid solar-plus-storage and wind-heavy portfolios.

Key Takeaway — Where the Money Is in 2026

For developers, the value pivot is from megawatt-hours to dispatchable megawatts. Standalone solar PPAs are losing value to negative pricing in Europe and queue cost in North America. Hybrid solar-plus-storage, 24/7 CFE structures, and behind-the-meter projects at data center sites command premiums of 15–30% over flat solar PPAs. The same 1 MW of solar is worth $52/MWh as a standalone European PPA and over $75/MWh as a 24/7 CFE block in CAISO.

The 2026 fundamentals: rising US PPA prices, falling European PPA prices, a 4% downgrade to commercial solar but an 11% upgrade to utility-scale, all wrapped around a hyperscaler buying spree that pulled 49% of global corporate clean energy procurement into four companies. This is not a market in trouble. It is a market re-pricing risk and re-routing capital.

Demand Drivers 2026: AI Data Centers, Onsite Generation, Corporate ESG

Five forces drive commercial solar demand into 2026. They do not contribute equally — AI data center load alone matters more than the other four combined.

Driver 1: AI Data Centers (The Dominant Force)

AI data centers are expected to triple their share of US electricity consumption from 4.4% in 2023 to 12% by 2028. A single AI task can consume up to 1,000 times more electricity than a traditional web search. Data centers drove half of all US electricity demand growth in 2024.

The numbers behind hyperscaler procurement:

- Microsoft crossed 40 GW of contracted clean power and signed an 8-year, 12 GW solar deal with Qcells. Its 2024 agreement with Brookfield Asset Management aims to develop 10.5 GW of new renewable capacity globally between 2026 and 2030.

- Google signed two 15-year PPAs with TotalEnergies in February 2026 for 1 GW of Texas solar — the 805 MW Wichita and 195 MW Mustang Creek projects. Google’s 24/7 CFE program achieves 90% hourly matching at five data centers.

- Amazon acquired a $650 million data center campus in Pennsylvania powered by an adjacent nuclear plant, and added rooftop solar with battery storage at multiple AWS facilities.

- Meta signed roughly 11 GW of clean energy contracts in 2025, including new behind-the-meter solar at Texas and Oklahoma data centers.

Texas hosts about 40% of new US utility-scale solar coming online this year and more than 25% of the country’s data center pipeline. ERCOT interconnection rights, transmission headroom, and developable land are now the most contested commodities in the C&I market.

“Procurement is moving from financial hedges to physical delivery, from grid-tied contracts to behind-the-meter energy parks, and from annual REC matching to 24/7 carbon-free hourly matching.” — pv magazine USA, March 2026, summarizing the shift in hyperscaler PPA strategy. Also see: Us Residential Solar Market Trends 2026.

The implication for commercial solar developers without hyperscale customers: every gigawatt the hyperscalers procure crowds out generic offsite capacity in the queue. The same projects that would have signed at $48/MWh in 2023 now sign at $58–$72/MWh in 2026 because a Microsoft or Meta bid set the floor.

Driver 2: Onsite Generation and Behind-the-Meter Economics

Retail electricity prices rose 5.2% year-on-year in 2025 across US commercial customers according to EIA data, with several states (Massachusetts, California, Hawaii) seeing double-digit increases. The retail-to-wholesale spread has widened from roughly $80/MWh in 2020 to $120/MWh in 2026. That spread is the entire commercial solar onsite value proposition.

Behind-the-meter rooftop and carport solar offsets retail rates of $0.10–$0.18/kWh. Onsite generation also avoids the demand charges that make up 30–60% of commercial bills. A typical 500 kW rooftop system at a Northeastern US distribution center now produces $0.13–$0.16/kWh of value — well above the $0.064/kWh standalone offsite PPA rate. For more on this topic, see Commercial Solar Carport Design Guide.

Walmart, Target, Prologis, and Amazon together added more than 800 MW of behind-the-meter rooftop solar in 2025 according to SEIA estimates, with another 1.1–1.4 GW projected for 2026.

Driver 3: Corporate ESG and 24/7 CFE Commitments

ESG is now segmented. The first wave of corporate solar (2015–2020) was driven by RE100 commitments — 100% renewable energy on an annual matching basis. The second wave (2021–2024) added scope 3 emissions and Science-Based Targets. The third wave, opening in 2025–2026, is 24/7 carbon-free energy.

Google, Microsoft, and Meta have all committed to 24/7 CFE by 2030. Schneider Electric, AT&T, and Iron Mountain are following. 24/7 CFE PPAs price 15–30% above standalone solar because they require a portfolio of solar, wind, storage, and firm clean power — and they cannot be met cheaply at any time-zone latitude.

Driver 4: Manufacturing Reshoring

The CHIPS Act and IRA Section 45X production tax credits triggered a manufacturing reshoring wave. Battery gigafactories (LG, Panasonic, Samsung SDI), chip plants (TSMC, Intel, Micron), and EV plants (Stellantis, Hyundai, Rivian) all need 24/7 baseload power and increasingly demand clean energy procurement as part of their site selection criteria.

A typical 1 GWh-per-year battery factory consumes 800–1,200 GWh of electricity annually. Pairing onsite solar with PPA-procured clean energy is now standard for new builds in Texas, Georgia, and Tennessee.

Driver 5: Logistics, Retail, and Telecom

Walmart targets 100% renewable energy by 2035. Amazon AWS is 100% renewable on annual matching as of 2023 and now pushing toward 24/7 CFE. AT&T announced a 1.5 GW renewable target including roughly 600 MW of solar tied to tower portfolios and edge compute sites.

Prologis, the largest logistics REIT in the world, committed to 1 GW of onsite solar across its global warehouse portfolio by 2025 — and now plans 2 GW by 2030. Multi-tenant industrial parks are emerging as the next major C&I segment, particularly when paired with multi-tenant commercial solar design.

For commercial sales teams chasing these accounts, solar proposal software with built-in irradiance modeling, demand-charge analysis, and lifecycle financial reporting shortens the buying committee cycle — particularly important for the commercial solar sales cycle that typically runs 4–9 months.

PPA Pricing: Where Rates Are Heading 2026 to 2028

PPA pricing in 2026 splits into three regimes: rising in tight North American markets, falling in saturated European markets, and stable to rising in emerging Asian markets. The drivers are different in each.

North America PPA Pricing 2026 to 2028

North American solar PPAs averaged $64.49/MWh in Q1 2026 per LevelTen, up from $57/MWh in Q1 2025. The forecast through 2028 is for continued upward pressure with possible relief in 2027 as utility-scale capacity catches up.

| Year | NA Solar PPA Average | CAISO | ERCOT | MISO | PJM |

|---|---|---|---|---|---|

| 2024 | $57/MWh | $66 | $52 | $54 | $60 |

| 2025 | $61/MWh | $70 | $54 | $58 | $64 |

| 2026 (Q1) | $64.49/MWh | $75 | $58 | $62 | $68 |

| 2027 (forecast) | $66–$72/MWh | $78–$85 | $60–$68 | $65–$72 | $70–$78 |

| 2028 (forecast) | $63–$70/MWh | $75–$82 | $58–$65 | $63–$70 | $68–$75 |

Source: LevelTen Energy Q1 2026 PPA Price Index plus author projections based on SEIA/Wood Mackenzie pipeline data and BloombergNEF capacity forecasts.

The 2026–2027 spike is driven by three converging forces:

- OBBBA construction deadlines: The July 4, 2026 start-of-construction deadline pulls demand forward.

- FEOC compliance: Material assistance requirements limit Chinese-sourced equipment, raising input costs.

- Hyperscaler procurement: 49% of global corporate clean energy deals (BloombergNEF 2025 data) sit with four buyers willing to pay above market.

The 2028 relief comes from the next wave of utility-scale supply hitting the market plus possible normalization of trade tariffs.

Europe PPA Pricing 2026 to 2028

European solar PPAs are in a different cycle. Q1 2026 hit €55.05/MWh — the fifth consecutive quarterly decline. The trajectory is shaped by demand weakness, negative pricing risk, and oversupply in Spain and Germany.

| Market | Q1 2026 | 2027 Forecast | 2028 Forecast |

|---|---|---|---|

| Spain | €38/MWh | €35–€42/MWh | €40–€48/MWh |

| Germany | €58/MWh | €52–€60/MWh | €55–€62/MWh |

| France | €62/MWh | €58–€65/MWh | €60–€68/MWh |

| UK | €58/MWh | €55–€62/MWh | €60–€68/MWh |

| Italy | €68/MWh | €62–€70/MWh | €65–€72/MWh |

| Netherlands | €54/MWh | €50–€58/MWh | €55–€62/MWh |

| Poland | €72/MWh | €68–€75/MWh | €70–€78/MWh |

Source: LevelTen Energy Q1 2026 PPA Price Index Europe plus BloombergNEF 1H 2026 Corporate Energy Market Outlook.

The European story is hybrid: standalone solar PPAs are losing value, but solar-plus-storage and solar-plus-wind hybrid PPAs are commanding premiums. Spain and Germany are the most exposed to cannibalization. UK and Italy hold up better because of capacity market interaction and lower solar penetration. For the latest details on UK, see Battery Solar System Design UK.

For installers operating in Italy specifically, the European solar incentives framework remains a significant value layer that PPA pricing alone does not capture.

Asia-Pacific PPA Pricing

APAC corporate PPA volume fell to 6.9 GW in 2025 from 10.7 GW in 2024 according to BloombergNEF, driven by slowdowns in India and South Korea. Solar PPA prices in India remain in the $35–$48/MWh range for utility-scale; Australia at AUD $55–$75/MWh; Japan at ¥9,500–¥12,000/MWh ($65–$82/MWh). The Asian market premium has compressed as Chinese module oversupply continues to dampen prices. Also see: Best Solar Design Software India. For India-specific information, see 5kW Solar Panel Price in India. For Australia-specific compliance details, see Australia comparisons/lgc-vs-stc.

Project Size Trends: Behind-the-Meter vs Offsite

The bifurcation between onsite (behind-the-meter) and offsite (utility-scale PPA) commercial solar is now structural. Each serves different customer needs and runs on different economics.

Behind-the-Meter Commercial Solar

Typical project size: 200 kW to 5 MW. Customer types: warehouses, distribution centers, office parks, manufacturing, retail. Economics: offsets retail rate ($0.10–$0.18/kWh US, €0.18–€0.30/kWh Europe) and avoids demand charges.

| BTM Segment | Typical Size | 2026 Installed Cost | Payback (with ITC) | Payback (post-ITC) |

|---|---|---|---|---|

| Small commercial (office, retail) | 50–250 kW | $1.80–$2.20/W | 6–8 years | 8–10 years |

| Mid-commercial (distribution center) | 250 kW–1 MW | $1.50–$1.90/W | 5–7 years | 7–9 years |

| Large commercial (manufacturing) | 1–5 MW | $1.30–$1.70/W | 4–6 years | 6–8 years |

| Carport (mixed retail/employee) | 500 kW–3 MW | $2.20–$2.80/W | 7–9 years | 9–11 years |

| Industrial rooftop with storage | 1–5 MW + 1–4 MWh | $2.10–$2.60/W | 5–7 years | 7–9 years |

Source: SEIA/Wood Mackenzie Q4 2025 installed cost data, EIA commercial retail rate data, author calculations on 30% ITC plus accelerated depreciation.

BTM economics improve as retail rates rise. The 2025 US commercial retail rate average was $0.137/kWh — up from $0.108/kWh in 2020, a 27% increase. Conservative forecasts have rates reaching $0.155–$0.170/kWh by 2030. This rate inflation, more than any policy support, will sustain BTM commercial solar after the ITC sunsets.

Offsite Commercial PPAs

Typical project size: 5 MW to 500 MW. Customer types: hyperscalers, large corporates, utilities reselling clean attributes. Economics: replaces wholesale electricity at $40–$80/MWh, claims RECs for sustainability reporting.

| Offsite PPA Type | Typical Size | 2026 Price Range | Tenor | Key Buyers |

|---|---|---|---|---|

| Physical PPA (sleeved) | 50–500 MW | $55–$75/MWh | 10–15 yr | Hyperscalers, large industrials |

| Virtual PPA (financial swap) | 20–300 MW | $50–$70/MWh | 10–15 yr | Tech, retail, banks |

| Green tariff (utility) | 5–100 MW | $60–$80/MWh | 5–10 yr | Mid-market corporates |

| Aggregated PPA | 5–50 MW (per buyer) | $58–$72/MWh | 7–12 yr | Multi-corporate consortia |

| 24/7 CFE block | 50–500 MW portfolio | $75–$110/MWh | 10–20 yr | Hyperscalers (Google, Microsoft) |

Source: LevelTen Energy 2026 PPA market data, BloombergNEF corporate energy outlook, and disclosed deals from Microsoft, Google, Amazon, Meta filings.

When BTM Beats Offsite

BTM makes sense when retail-to-wholesale spread exceeds installed cost amortization. With US commercial retail at $0.137/kWh and wholesale solar PPAs at $0.064/kWh, the spread is $0.073/kWh — enough to pay back a $1.70/W behind-the-meter system in 6–8 years.

Offsite makes sense when scale exceeds onsite roof area, when 100% renewable matching is a corporate goal, or when the buyer wants RECs without site complexity. A Microsoft data center with 200 MW load cannot meet that demand from rooftop solar — it needs offsite PPA scale.

For developers serving warehouse and distribution clients, commercial battery storage sizing is now part of the standard scope, particularly in California (NEM 3.0), Massachusetts, and New York where time-of-use rates make storage essential. For more on this topic, see Adding Battery Storage Services.

What Most Commercial Solar Reports Miss

Industry reports tend to repeat three narratives that are increasingly out of date. Here is what I see from the deal floor that does not match the published outlook.

Misconception 1: “Tariffs Will Crush Commercial Solar in 2026”

The tariff impact is real — 10% year-on-year price increase per Wood Mackenzie — but it is asymmetric across project sizes. Large utility-scale and hyperscaler BTM projects with safe-harbored modules are barely affected because they procured 2023–2024 inventory and locked in long-term supply contracts with Korean and Vietnamese manufacturers.

The pain falls on mid-market C&I projects (200 kW to 2 MW) that buy at spot. These buyers face the full tariff hit and rarely have the procurement power to negotiate around it. The headline forecast averages across both, masking a clean segmentation: the top of the market is fine, the middle is squeezed.

Misconception 2: “Behind-the-Meter Solar Needs the ITC”

It does not. The 30% commercial ITC matters, but with retail rates rising 4–6% annually and module prices falling 18% over the last two years per BloombergNEF, BTM commercial payback was already in the 6–8 year range before the ITC. Post-ITC payback drifts to 8–10 years — still better than most CFO hurdle rates for energy capex.

The customers most worried about ITC sunset are the ones with the worst economics anyway: small commercial rooftops in low-rate states. They should not have been buying solar on tax credit math in the first place.

Misconception 3: “Storage Solves Everything”

Solar-plus-storage is the consensus answer to every C&I problem in 2026. It is not. Storage doubles project cost, increases EPC complexity, and adds dispatch optimization risk. For a typical 1 MW commercial rooftop in a flat-rate region, adding 1 MWh of storage extends payback by 2–4 years.

Storage shines in three specific cases: NEM 3.0 California (where export compensation is minimal), demand charge management at high-load facilities, and microgrid resilience for mission-critical operations. Outside those cases, “we’ll add storage” is often a sales reflex that destroys the value proposition.

Tradeoff: Hyperscaler Premium vs Mid-Market Squeeze

The unspoken tradeoff in 2026 commercial solar: developers can chase hyperscaler scale (high MW, complex 24/7 CFE terms, multi-year negotiations) or mid-market velocity (smaller projects, faster close cycles, traditional PPA terms). Few firms execute well on both.

Hyperscaler deals can carry $5–$15 million in development costs over 18–36 months. A mid-market 2 MW BTM project closes in 4–6 months at a fraction of that overhead. The wrong choice between the two is the single biggest strategic error I see in commercial solar developer business plans.

Pro Tip — Pick a Lane

The 2026 commercial solar market punishes generalists. Developers should pick BTM or offsite, hyperscaler or mid-market, US or Europe. Trying to serve all four quadrants leads to thin pipelines and unfocused proposals. Boards we serve typically realize this 12–18 months too late, after burning capital chasing the wrong segment.

Model C&I Solar Economics Across Markets

SurgePV’s commercial solar design and proposal stack handles utility-rate analysis, demand charge modeling, ITC and depreciation calculations, and PPA versus self-financed comparisons in a single workspace. Built for installers and developers who run BTM and offsite portfolios side by side.

Book a DemoNo commitment required · 20 minutes · Walkthrough with your live commercial pipeline

For France-specific information, see Agricultural Solar Case Study.

Financing Models: Tax Equity After Direct Pay

The financing layer underneath commercial solar shifted more than the technology layer over the last three years. Tax equity used to be the only path to monetize the federal ITC. Now it is one of four, and OBBBA is rewriting the rules.

Tax Equity Today

Tax equity — the structure where a bank or insurance company takes the ITC and accelerated depreciation in exchange for cash equity — financed approximately $20 billion per year of US renewables historically. In 2026, that volume sits around $18–$22 billion but with reshaped terms: shorter flip horizons, tighter FEOC compliance covenants, and higher developer guarantees.

The main tax equity providers in commercial solar 2026 are JPMorgan, Bank of America, Wells Fargo, US Bank, MUFG, and several insurance companies. Yields on tax equity investments now sit at 8.5–11% after-tax — up from 6.5–8% in 2022. That increase reflects perceived policy risk under OBBBA.

Direct Pay (The Tax-Exempt Pathway)

Direct pay, enacted in the Inflation Reduction Act and preserved (with modifications) under OBBBA, allows tax-exempt entities to receive the ITC as a cash payment from the IRS:

- Municipalities and county governments

- Public schools, universities, hospitals (501(c)(3))

- Rural electric cooperatives

- Tribal governments and Alaska Native Corporations

- Tennessee Valley Authority and other federal power authorities

Direct pay eliminates the tax equity middle layer entirely. A municipal warehouse PV project that historically would have lost 25–35% of ITC value to tax equity friction now keeps the full 30% credit. The catch under OBBBA: FEOC and material assistance compliance must be documented, and audit risk is non-trivial.

Transferability

Section 6418 of the IRA allows project owners to sell the ITC to an unrelated buyer for cash. Transferability is now a major financing alternative — particularly for mid-sized developers who lack tax appetite and want to avoid tax equity complexity. Typical 2026 transfer prices: $0.91–$0.96 per dollar of ITC for low-risk projects, $0.85–$0.92 for higher-risk projects.

Transferability volume hit roughly $25 billion in 2025 according to several major brokers, and is on track for $30–$40 billion in 2026. It is now the largest single financing channel for mid-market commercial solar.

Sponsor Equity and Project Debt

The traditional project finance stack — sponsor equity (10–25%), term debt (60–75%), tax equity (15–25%) — still works but the term debt component has expanded. Solar-as-a-service lenders like Sunwealth, Generate Capital, and Greenbacker now offer all-in financing at 7.5–9.5% IRR to LPs for commercial projects above 1 MW.

| Financing Structure | Project Size | All-in Yield to Owner | Best Fit |

|---|---|---|---|

| Tax equity partnership | 5 MW+ | 6.5–8.5% | Large utility-scale, hyperscaler PPA |

| ITC transferability | 1–10 MW | 7.5–9.5% | Mid-market commercial |

| Direct pay | All sizes | 8–10% | Tax-exempt entities (cities, schools, co-ops) |

| Sponsor + project debt | 500 kW–5 MW | 8–11% | Independent commercial owners |

| Solar-as-a-service / PPA | 200 kW–10 MW | 9–13% | Off-balance-sheet C&I customers |

| Cash purchase | Any | 11–18% IRR | Self-funded corporates |

Source: Author analysis of 2026 commercial solar financing market, Cohnreznick tax equity data, Norton Rose Fulbright transferability tracker, and disclosed deal terms from major sponsor companies.

For commercial sales teams structuring deals, modeling all five financing paths against a single project is now table stakes. The right structure can move project IRR by 200–400 basis points — often the difference between go and no-go for the corporate buyer.

Interconnection Queue and Grid Constraints

Interconnection is the single biggest bottleneck in commercial solar 2026 — bigger than tariffs, labor, or capital cost. Wood Mackenzie counts about 160 GW of committed large-load interconnection requests in the US pipeline. The Lawrence Berkeley National Laboratory tracks roughly 2,300 GW of total generation in interconnection queues nationwide, with average wait times of 4–5 years for utility-scale solar.

Queue Wait Times by Region 2026

| ISO/RTO | Avg Wait Time (Solar) | Withdrawal Rate | Active Solar in Queue (GW) |

|---|---|---|---|

| MISO | 5+ years | 75% | ~400 GW |

| ERCOT | 2–3 years | 55% | ~180 GW |

| PJM | 4–5 years | 70% | ~250 GW |

| CAISO | 4–6 years | 65% | ~190 GW |

| SPP | 4–5 years | 72% | ~140 GW |

| ISO-NE | 5–7 years | 80% | ~60 GW |

| NYISO | 6+ years | 78% | ~80 GW |

Source: Lawrence Berkeley National Laboratory Queue Report 2025, ISO-specific quarterly queue updates, and FERC Order 2023 implementation tracking.

ERCOT is the relative bright spot — competitive interconnection, large land availability, and aggressive transmission build-outs. Texas hosts about 40% of new US utility-scale solar coming online this year. CAISO, MISO, and PJM all have queues so deep that 60–80% of submitted projects withdraw before reaching commercial operation.

For C&I onsite (behind-the-meter) projects, interconnection is typically faster — most distribution utility queues run 6–18 months. But export-limited or larger BTM projects (above 2 MW) trigger transmission-level studies and can stall for years. Engineers serving these clients should review solar interconnection application guide and export limitation solar design commercial before quoting timelines.

FERC Order 2023 Impact

FERC Order 2023, fully implemented through 2024–2026, reformed the US interconnection queue from a serial first-come-first-served process to a cluster-based study approach. The intent: process more projects faster, reject undeveloped speculation early. Early results show 15–25% throughput improvement in MISO and SPP queues. CAISO and PJM are still working through transitional backlogs.

The practical implication for commercial developers: 2024 and 2025 queue entries get cluster-study results in 2026. Projects that did not get into the queue by mid-2025 are unlikely to come online before 2029.

Behind-the-Meter Advantage in 2026

Behind-the-meter projects bypass the worst queue dynamics. A 500 kW rooftop on a distribution center can typically interconnect within 4–8 months in most US states. A 2 MW utility-scale project in MISO takes 4–6 years. That timing difference is the entire argument for prioritizing BTM in 2026 — even if PPA economics on offsite would be marginally better.

2027 to 2028 Outlook for C&I Solar

The 2027–2028 window will define the post-ITC commercial solar market. Three scenarios bracket the range of plausible outcomes.

Scenario A: Soft Landing (35% Probability)

OBBBA stays in place. The July 4, 2026 construction deadline pulls demand forward. 2027 sees a moderate dip in new utility-scale starts but commercial recovery as Wood Mackenzie projects (12% annual C&I growth). PPA prices stabilize at $60–$70/MWh. Hyperscaler procurement continues at 30–40 GW per year globally. Tax equity volume contracts but transferability and direct pay fill the gap. Module prices fall another 12–18%.

This is the consensus forecast. It assumes regulatory continuity and steady AI data center load growth.

Scenario B: Policy Whiplash (40% Probability)

A new administration or legislative action modifies OBBBA — either expanding ITC eligibility or further tightening FEOC and material assistance rules. Developers stall projects pending clarity. PPA prices spike to $75–$90/MWh in tight markets. Hyperscaler procurement continues but shifts more aggressively to non-tax-credit structures (utility green tariffs, behind-the-meter, direct ownership).

This scenario produces the highest near-term price volatility but does not change the long-term growth trajectory. The fundamentals — retail rate inflation, AI load, grid scarcity — drive demand regardless of federal policy.

Scenario C: Demand Shock (25% Probability)

AI data center load exceeds even the bullish projections. Wood Mackenzie’s 160 GW pipeline materializes faster than expected. PPA prices climb to $80–$100/MWh in CAISO, ERCOT, and PJM. Commercial onsite solar booms as data center operators pursue every available megawatt. Solar-plus-storage becomes table stakes. Texas and Arizona land prices triple for utility-scale-suitable parcels.

This scenario is bullish for solar developers with locked-in pipeline but bearish for new market entrants. Land, EPC capacity, and module supply all become severe constraints.

Combined Outlook

| Metric | 2026 | 2027 | 2028 |

|---|---|---|---|

| US C&I solar additions | 1.8–2.1 GWdc | 2.2 GWdc | 2.5 GWdc |

| US utility solar additions | 43 GW | 38–42 GW | 35–40 GW |

| NA solar PPA average | $64.49/MWh | $66–$72/MWh | $63–$70/MWh |

| EU solar PPA average | €55/MWh | €52–€58/MWh | €55–€62/MWh |

| Global corporate PPA volume | 60–70 GW | 55–75 GW | 60–80 GW |

| Hyperscaler share of global corporate PPA | ~50% | 50–55% | 50–55% |

| Module ASP (utility) | $0.11–$0.13/W | $0.10–$0.12/W | $0.09–$0.11/W |

| C&I rooftop installed cost | $1.50–$1.90/W | $1.45–$1.85/W | $1.40–$1.80/W |

Source: Author synthesis of SEIA/Wood Mackenzie, BloombergNEF, LevelTen Energy, EIA, and Lawrence Berkeley National Laboratory data plus base/scenario weighting.

Practical Implications for Developers and Installers

The 2026 commercial solar market rewards specialization, scale partnerships, and disciplined project selection. Generic C&I development strategies that worked in 2021–2023 do not scale into 2026.

For C&I Developers

- Pick your segment by Q2 2026. BTM mid-market, BTM enterprise, offsite mid-scale, offsite hyperscale. Pick one and build the team around it.

- Build interconnection capacity in-house. The single biggest constraint on revenue is queue position, not sales pipeline. A senior interconnection engineer is now more valuable than two senior origination leads.

- Develop financing optionality. Run tax equity, transferability, and direct pay quotes on every deal. Right-structuring adds 200–400 bps of project IRR.

- Texas, Arizona, and select MISO markets first. ERCOT interconnection, transmission headroom, and developable land are the most contested commodities. Get there or skip utility-scale.

For Commercial Installers

- Focus on BTM projects 250 kW to 5 MW. This is the sweet spot where retail rate inflation drives economics and interconnection is manageable.

- Sell on demand charge reduction, not only kWh offset. Demand charges drive 30–60% of commercial bills. Solar-plus-storage targeting demand charge reduction is the strongest 2026 BTM pitch.

- Pre-qualify financing partners early. Solar-as-a-service providers (Sunwealth, Generate, Greenbacker) and ITC transfer brokers (Crux, Reunion, Atheva) want to see project pipeline. Build relationships now.

- Invest in design and proposal tools. Mid-market commercial customers compare 2–4 proposals. The proposal that includes accurate retail rate modeling, demand charge analysis, and clear financing options wins disproportionately. Tools like solar design software and commercial solar design software shorten close cycles.

For Corporate Buyers

- Distinguish 100% annual matching from 24/7 CFE. The latter is 3–10x harder and 15–30% more expensive. Set the right target.

- Behind-the-meter first, offsite second. BTM solar offsets retail rate; offsite PPA offsets wholesale. Capture the retail-wholesale spread before pursuing scale.

- Lock multi-year supplier pipelines. The hyperscalers locked in 5–10 year supplier pipelines in 2023–2024. Mid-tier corporate buyers should sign 2026–2027 RFPs for 2028–2030 delivery to secure pricing.

- Don’t over-pay for greenfield development. Operating solar assets trade at meaningful discounts to development-stage projects. Acquiring brownfield C&I solar can be 25–40% cheaper than commissioning new builds in 2026.

Case Example: California Distribution Center Operator

A West Coast logistics operator with 14 distribution centers across California, Arizona, and Nevada needed to hedge against PG&E and SCE rate increases averaging 8% annually. The internal team modeled three options:

| Option | Project Scope | Capex | Annual Savings (Year 1) | 25-Year NPV | Payback |

|---|---|---|---|---|---|

| Option A: Full BTM rooftop + carport across all 14 sites | 42 MW total | $73M | $9.2M | $148M | 7.5 yr |

| Option B: BTM at top 6 sites + 30 MW offsite PPA | 18 MW BTM + 30 MW offsite | $32M (BTM) + PPA fees | $5.8M | $94M | 6.5 yr (BTM portion) |

| Option C: 60 MW offsite virtual PPA only | None onsite | $0 capex + PPA fees | $3.1M | $52M | n/a |

The board chose Option B. The BTM portion captured the retail-wholesale spread at the highest-cost sites (LA, Riverside) while the offsite PPA hedged the remaining 70% of consumption with no capex. The deal closed in Q1 2026 with Crux ITC transferability on the BTM portion and a 15-year offsite PPA with a Texas developer at $62/MWh. Total expected savings: $145–$160M over 25 years.

This is the new commercial solar shape: hybrid, financed across multiple structures, designed around interconnection reality rather than pure economic optimum.

For developers building these proposals at scale, the generation financial tool shortens the multi-scenario modeling cycle that wins these accounts.

Conclusion

The 2026 commercial solar market is harder than 2024, more interesting than 2023, and structurally healthier than the headlines suggest. Forecasts cut by 4% mask a market that is repricing risk rather than retreating. AI data center load alone justifies the next decade of build-out. Retail rate inflation supports BTM economics regardless of federal policy.

The clearest signals from the deal floor: hyperscalers will keep paying premiums for physical, dispatchable, 24/7 clean power. Mid-market BTM solar will keep penetrating because retail rate inflation outpaces installed cost reduction. Standalone solar PPAs will keep losing value to negative pricing in Europe and to hybrid structures everywhere else.

Three actions for 2026:

- Lock interconnection positions in ERCOT, MISO, and PJM by Q3 2026 if you are pursuing utility-scale — the 2027–2028 queue is effectively closed.

- Pre-qualify ITC transferability and direct pay financing partners on every BTM project above 500 kW — the structure adds 200–400 bps of IRR.

- Specialize by Q2 2026 between BTM mid-market and offsite hyperscale — generalist developers will lose to specialists in both halves of the market.

For deeper reading on closing C&I deals, see our guides on closing commercial solar deals with procurement committees and consultative selling for solar. For the global context, our European solar incentives breakdown covers the EU side of the 2026 PPA divergence.

Frequently Asked Questions

What is the commercial solar market outlook for 2026?

The 2026 commercial solar market outlook is mixed near-term, strong medium-term. Wood Mackenzie cut its five-year C&I forecast by 4% on tariff pressure and EPC labor shortages, with 2026 commercial volumes expected to dip on the back of the California NEM 2.0 wind-down. From 2027 to 2030, SEIA and Wood Mackenzie project 12% average annual growth in commercial solar, driven by AI data center load, retail rate inflation, and emerging Midwest and Southeast markets. Corporate PPA volumes globally hit 55.9 GW in 2025 per BloombergNEF, with solar still the dominant technology.

How much are commercial solar PPA prices in 2026?

Solar PPA prices in 2026 diverged sharply by region. LevelTen Energy’s Q1 2026 index put North American solar PPAs at $64.49/MWh, up 4.6% quarter-on-quarter and 13% year-on-year. European solar PPAs fell to €55.05/MWh (~$64.83/MWh), down 13% year-on-year and the fifth consecutive quarterly decline. Hyperscaler demand, ERCOT bottlenecks, and FEOC compliance under OBBBA pushed US prices higher, while weak European industrial demand and negative pricing risk pulled rates down.

How are AI data centers affecting commercial solar in 2026?

AI data centers are the single biggest driver reshaping commercial and corporate solar in 2026. Wood Mackenzie counts about 160 GW of committed large-load interconnection requests in the US pipeline, roughly 22% of 2024 peak demand. Hyperscalers (Microsoft, Amazon, Google, Meta) signed 49% of all global corporate clean energy deals in 2025 per BloombergNEF. Microsoft has crossed 40 GW of contracted clean power. Procurement is shifting from financial RECs to physical delivery, 24/7 hourly matching, and behind-the-meter energy parks co-located with data centers.

What is the difference between behind-the-meter and offsite commercial solar?

Behind-the-meter (BTM) commercial solar sits on the customer’s side of the utility meter and offsets retail electricity rates directly — typical for rooftop and onsite carport projects at warehouses, distribution centers, and office parks. Offsite commercial solar is a separate generation asset, often utility-scale, contracted through a physical or virtual power purchase agreement. BTM saves at retail rates ($0.10–$0.18/kWh in the US); offsite PPAs lock in wholesale-linked pricing ($40–$80/MWh). Hyperscalers increasingly use both — BTM for resilience, offsite PPAs for sustainability scale.

Will commercial solar grow without the federal ITC after 2027?

Yes, but the trajectory changes. Under OBBBA, Section 48E and 45Y commercial tax credits end after 2027 unless projects start construction by July 4, 2026 (then they get four years to come online). New FEOC and material assistance rules apply. Wood Mackenzie still projects 12% annual C&I growth from 2027 to 2030, on the assumption that retail rate inflation, AI data center demand, and falling module costs offset the credit loss. Sites with strong self-consumption economics and behind-the-meter exposure will keep penetrating even without incentives.

What is a 24/7 carbon-free energy PPA?

A 24/7 carbon-free energy (CFE) PPA matches clean electricity to a buyer’s consumption on an hourly basis, every hour of every day, rather than just on annual net volume. Google pioneered the framework — its 24/7 CFE program now achieves 90% hourly matching at five data centers. Standard annual REC-matched PPAs may show 100% renewable on paper while drawing from gas at night. 24/7 CFE typically requires a portfolio of solar, wind, storage, and firm clean power, and prices 15–30% above standalone solar PPAs. It is becoming the new gold standard for hyperscaler procurement.

What are tax equity and direct pay in commercial solar?

Tax equity is the financing structure where an investor with US federal tax appetite (historically banks and insurance companies) takes the Investment Tax Credit and depreciation benefits in exchange for cash. It has financed roughly $20 billion per year of US renewables. Direct pay, enacted in the Inflation Reduction Act, lets tax-exempt entities (municipalities, schools, cooperatives, tribes) receive the ITC as a cash payment from the IRS without needing a tax equity partner. OBBBA preserves direct pay for certain entity types through the 2027 ITC sunset but tightens FEOC compliance, which is now reshaping deal structures.

Which industries are driving commercial solar demand in 2026?

Five industries dominate 2026 C&I solar demand. First, hyperscale data centers (Microsoft, Amazon, Google, Meta) account for 49% of global corporate PPA volume per BloombergNEF. Second, retail and logistics — Walmart, Amazon, Target, and Prologis — driving rooftop megawatts on distribution networks. Third, manufacturing reshoring, especially battery and chip plants tied to onshoring incentives. Fourth, food and beverage (Anheuser-Busch, PepsiCo, Mars) chasing ESG targets. Fifth, telecom — AT&T and Verizon contracting solar to power tower portfolios and edge compute sites.

Sources:

- SEIA / Wood Mackenzie US Solar Market Insight Q4 2025 and Q1 2026

- LevelTen Energy Q1 2026 PPA Price Index — North America and Europe

- BloombergNEF 1H 2026 Corporate Energy Market Outlook

- US Energy Information Administration Electricity Data Browser

- Lawrence Berkeley National Laboratory — Interconnection Queue Report 2025