Quick Answer

European solar incentives in 2026 include Germany's EEG feed-in tariff (8.11 ct/kWh, 20 years) and 0% VAT, Italy's Ecobonus (50% tax deduction) and GSE net metering, France's EDF OA feed-in tariff (up to 23.49 ct/kWh), and Spain's IDAE grants (15–40% of costs). The UK maintains 0% VAT on residential solar through 2027.

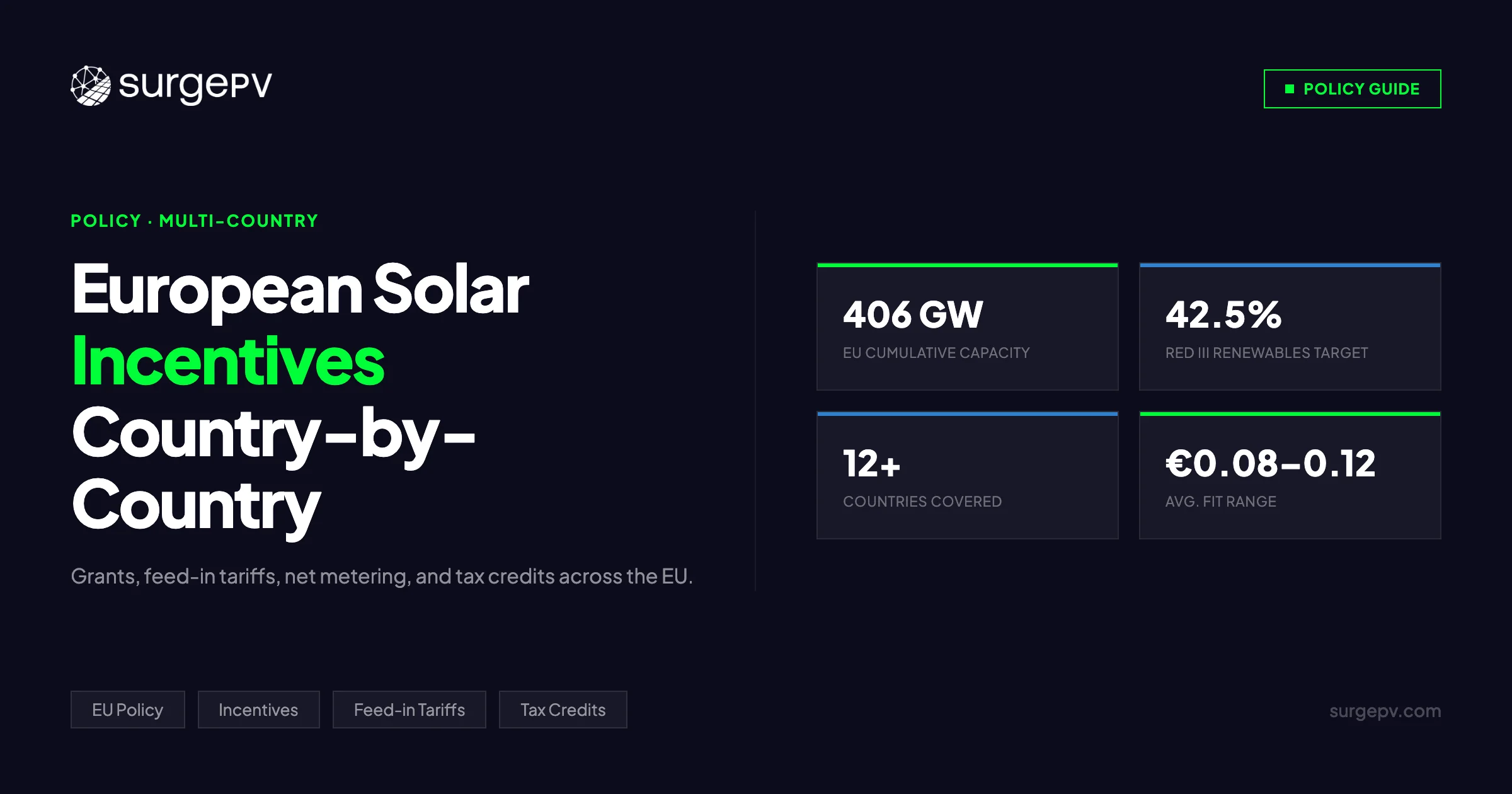

Europe is in the middle of a solar financing transition — and the direction is clear. The REPowerEU plan committed €210 billion to energy independence, with solar at the centre of that strategy. RED III raised the binding renewable energy target to 42.5% by 2030. The EU Solar Strategy originally targeted 600 GW; the Net Zero Industry Act pushed the headline to 750 GW. As of end-2025, the EU’s cumulative solar fleet stood at 406 GW — roughly 54% of the way there with four years to go. For Europe-specific compliance details, see Europe solar compliance.

European solar incentives in 2026 include Germany’s EEG feed-in tariff (8.11 ct/kWh, 20 years) and 0% VAT, Italy’s Ecobonus (50% tax deduction) and GSE net metering, France’s EDF OA feed-in tariff (up to 23.49 ct/kWh), and Spain’s IDAE grants (15–40% of costs). The UK maintains 0% VAT on residential solar through 2027. Also see: solar panel ROI in Italy. Also see: Germany solar subsidies. Also see: France solar feed-in tariffs. Also see: Spain net metering.

At the same time, the incentive environment is changing faster than many installers realise. Germany’s Solar Peak Act suspends feed-in tariff payments during negative grid price periods. France has removed the 100–500 kW commercial rooftop segment from its OA feed-in tariff entirely. Italy’s Superbonus has been cut from 110% to 50%. The Netherlands voted to end residential net metering on January 1, 2027. Italy’s Scambio sul Posto closed to new registrations in September 2025.

For solar installers, EPCs, and project developers working across European markets, navigating these changes correctly is the difference between a proposal that closes and one that falls apart in due diligence. The financial case for solar in Europe in 2026 increasingly rests on self-consumption savings, storage pairing, and correctly stacking available incentives — not on the headline feed-in tariff rate alone.

This guide covers eight EU markets — Germany, France, Spain, Italy, the Netherlands, Austria, Belgium, and Poland — plus a UK section and EU-wide programs. For each market, you will find current rates, eligibility rules, key deadlines, and the incentive combinations that yield the strongest financial returns. A worked stacking example at the end shows how to model the full picture for a real project. Read more about Agricultural Solar Case Study. For UK-specific information, see Battery Solar System Design UK. For United Kingdom-specific compliance details, see United Kingdom comparisons/mcs-vs-non-mcs.

European solar incentives in 2026 span four types: feed-in tariffs (Germany EEG, France OA), capital grants (Spain IDAE, Austria EAG), tax deductions (Italy Ecobonus 50%, Germany 0% VAT), and market premiums (Netherlands SDE++). The strongest financial cases stack two or three layers. Germany offers the deepest stack: EEG tariffs at 8.11 ct/kWh, KfW loans, battery grants up to €3,200, and zero VAT. France leads on small-system rates at up to 23.49 ct/kWh for under 3 kWp. Solar design software helps model stacked incentives per country. See our guide on Commercial Rooftop Solar Case Study Italy for more.

TL;DR — European Solar Incentives 2026

EU cumulative solar: 406 GW at end-2025. RED III mandates 42.5% renewable share by 2030. Germany: EEG FiT €0.0786–€0.1247/kWh (up to 10 kW), KfW 270 loans, KfW 442 battery grant up to €3,200, 0% VAT on hardware. France: OA FiT up to €0.2349/kWh (Q1 2026, under 3 kWp full injection), Prime à l’Autoconsommation up to ~€1,900/kWp over 5 years, 10% TVA on eligible systems. Spain: compensación simplificada at hourly PVPC spot price, IBI up to 50%, ICIO up to 95%, regional IRPF 20–60%. Italy: Superbonus 50–65%, Ritiro Dedicato via GSE (Scambio sul Posto closed Sept 2025), CER communities up to €110/MWh. Netherlands: SDE++ €8B budget 2026, saldering ends Jan 2027. UK: Smart Export Guarantee (SEG), MCS certification, ECO4 for low-income households. Poland: net billing at spot price, Mój Prąd grants, 8% VAT on systems under 50 kW. EU-wide: REPowerEU, ETS revenues funding national programs, RED III permitting caps.

In this guide:

- Latest solar incentive updates across major European markets, March 2026

- EU-wide framework: RED III, REPowerEU, Fit for 55, and how they shape national programs

- Germany: EEG feed-in tariffs, KfW loans and grants, Solarpaket I, VAT exemption, Solar Peak Act

- Italy: Superbonus 50–65%, Detrazione Fiscale, Ritiro Dedicato, CER energy communities

- France: Obligation d’Achat rates, Prime à l’Autoconsommation, TVA, Credit Impôt history

- Spain: RD 244/2019 autoconsumo, municipal tax incentives, IDAE programs

- Netherlands: SDE++ subsidy structure, saldering phase-out, residential transition

- UK: Smart Export Guarantee, MCS, ECO4, and the post-FiT environment

- Poland: Mój Prąd, net billing, OZE auctions, VAT reduction

- Austria, Belgium, and other EU markets

- REPowerEU and EU ETS funding flows to national solar programs

- How to stack incentives: full worked example with three country scenarios

Latest Updates: European Solar Incentives 2026

The table below captures the major changes to European solar incentive programs since January 2025. Installers and developers should treat this as the first checkpoint before building any project financial model.

| Country | Program | Change | Effective Date |

|---|---|---|---|

| Germany | EEG feed-in tariff | Solar Peak Act suspends FiT during negative grid price periods | February 2025 |

| Germany | EEG FiT rates | Degraded rates published for Aug 2025 – Jan 2026 (1% per 6-month cycle) | August 2025 |

| Germany | Solarpaket I | Simplified planning rules for rooftop PV; community energy provisions expanded | May 2024 |

| France | OA FiT scope | Systems 100–500 kW removed from OA framework; CRE tender only | Q4 2025 |

| France | OA tariff rates | CRE cuts Q4 2025 rates for 10–100 kW band by ~15% | Q4 2025 |

| Italy | Scambio sul Posto | Closed to new registrations (cut-off: September 26, 2025) | September 2025 |

| Italy | Superbonus | Deduction reduced to 50% for most residential works; 65% for major condominium retrofits | January 2025 |

| Italy | CER Decree | 2024 energy community decree fully operational; GSE incentive up to €110/MWh | January 2024 |

| Netherlands | Saldering | Parliament confirmed end date: January 1, 2027 | November 2024 |

| Netherlands | SDE++ | Plans announced to replace large-scale SDE++ with two-way CfDs from 2027 | October 2025 |

| Spain | IDAE innovative fund | New €202.5M call for innovative renewables and storage (window closed Feb 2026) | Jan–Feb 2026 |

| Spain | NextGen EU grants | Approved projects (RD 477/2021) must complete installation by June 30, 2026 | Deadline June 2026 |

| UK | SEG rates | Several major suppliers updated SEG rates; Octopus, E.ON revised upward | Q1 2026 |

| UK | ECO4 | Scheme extended; targeting 1 million homes through 2026 | Ongoing |

| Poland | Mój Prąd 6 | Round 6 concluded; round 7 call anticipated H1 2026 | 2025–2026 |

| Austria | EAG investment grant | New Q2 2026 call opens April 23, €40M budget | April 2026 |

| Austria | ”Made in Europe” bonus | 20% funding uplift for EU-manufactured PV components | 2025 onwards |

| EU-wide | RED III | Transposing into national law through 2025; 12-month permitting cap in acceleration areas | 2024–2025 |

Key Takeaway

The overarching trend across Europe in 2026 is a shift from guaranteed feed-in tariffs toward self-consumption, market premiums, and competitive tenders. Countries that led on generous FiTs — Germany, France, Italy — are all reducing them. The economic case for solar increasingly rests on self-consumption savings, storage pairing, and tax incentive stacking rather than grid export revenue alone. Installers who model this shift accurately in their proposals win more business; those who still lead with FiT rates face clients who have already read the headlines.

EU-Wide Framework: How REPowerEU and RED III Shape National Incentives

Before diving into country-specific programs, understanding the EU-level architecture that underpins them matters — especially for developers working across multiple markets or accessing EU funding streams directly.

RED III and the 42.5% Renewable Target

The Renewable Energy Directive III (RED III), agreed in late 2023 and transposing into national law through 2025, raises the EU-wide renewable energy target to 42.5% by 2030, with a stretch aspiration of 45%. For solar specifically, RED III introduces:

- 12-month permitting cap for new solar installations sited within designated Renewable Acceleration Areas (RAAs). Member states must designate RAAs and achieve the cap by mid-2026.

- Mandatory solar on new commercial and public buildings over 250 m² from 2026, and on new residential buildings from 2029.

- Simplified grid access requirements for smaller installations across all member states.

RED III does not set national feed-in tariff levels. But it forces every member state to maintain an incentive environment that keeps solar deployment on track. Countries that fall behind the trajectory risk EU infringement proceedings and loss of access to REPowerEU funding, which creates a structural floor under national solar support — even as individual programs are reformed or scaled back.

REPowerEU and the 750 GW Headline Target

REPowerEU, launched in May 2022, set an original solar target of 600 GW by 2030 to reduce dependency on Russian gas. The Net Zero Industry Act and subsequent policy statements pushed the effective headline to 750 GW. At 406 GW cumulative installed by end-2025, the EU is on track to miss both targets at current pace, which is the key driver behind continued national incentive support across member states.

The REPowerEU plan channelled funds through several mechanisms relevant to solar:

- National Recovery and Resilience Plans (NRRP): Each member state’s PNRR/recovery plan includes solar components. Italy committed €1.5 billion to agri-PV. Spain’s NextGen EU grants (RD 477/2021) totalled billions across the autonomous communities. Poland’s recovery plan includes Mój Prąd grant extensions.

- Innovation Fund: Funded from EU Emissions Trading System (ETS) revenues, the Innovation Fund has committed €38 billion to low-carbon technology deployment. Large-scale solar projects in Central and Eastern Europe have accessed this funding.

- Cohesion and ERDF funding: European Regional Development Fund programs continue to channel infrastructure investment toward solar in lower-income member states including Poland, Romania, Bulgaria, and Croatia.

How ETS Revenues Fund Solar Programs

Since 2021, revenues from the EU Emissions Trading System have partly funded the Innovation Fund and national climate investment programs. As carbon permit prices fluctuate — the ETS carbon price ranged from €45 to €75/tonne through 2025 — the quantum of funding flowing to solar support varies. Several member states, including Poland and the Czech Republic, have used ETS auction revenues to finance their domestic solar grant programs. This linkage means ETS price movements have indirect effects on the availability of solar grant funding across Central and Eastern Europe.

Four Types of National Solar Incentive

EU member states use four main mechanisms, often in combination:

- Feed-in tariffs (FiTs): A fixed, guaranteed price per kWh exported to the grid for a set term (typically 20 years). Once dominant across Europe, now declining in scope. Germany (EEG), France (OA), and Italy (historic Conto Energia) are the primary examples.

- Market premiums: A top-up above the wholesale electricity market price, rather than a guaranteed absolute rate. Germany’s Marktprämie for systems over 100 kW, Netherlands SDE++, and Austria’s OeMAG premium use this model. Increasingly the preferred mechanism as grid penetration rises.

- Direct grants and rebates: Capital subsidies covering a percentage of installation cost, paid upfront or over a short period. France’s Prime à l’Autoconsommation, Austria’s EAG Investitionszuschuss, Poland’s Mój Prąd, and Germany’s KfW 442 are examples.

- Tax incentives: VAT reductions on hardware and installation, income tax deductions on qualifying investment costs, or property tax credits. Italy’s Superbonus, Germany’s 0% VAT, Spain’s IBI/ICIO/IRPF municipal and regional discounts, and Poland’s 8% VAT reduction are the main instruments.

The highest-returning installations in 2026 stack multiple mechanisms from this list. A German residential project might combine EEG FiT + KfW 270 loan + KfW 442 battery grant + 0% VAT on hardware. An Italian project might combine Superbonus 50% deduction + Ritiro Dedicato grid payment + CER energy community incentive. The worked stacking example later in this guide shows how to model these combinations using solar design software with country-specific financial modelling.

Germany Solar Incentives 2026

Germany remains Europe’s largest solar market by cumulative installed capacity — approximately 100 GW at end-2025 — and operates one of the continent’s most structured incentive frameworks. Three parallel systems define the economics: the EEG feed-in tariff, KfW financing programs, and the VAT exemption. The Solarpaket I legislative reform package (May 2024) simplified planning rules and expanded community energy provisions. The Solar Peak Act (February 2025) introduced new complexity around negative grid price periods.

For a full breakdown of the German subsidy environment, see our guide to solar incentives subsidies Germany.

EEG Feed-in Tariff (Einspeisevergütung)

Germany’s Renewable Energy Sources Act (EEG) mandates that grid operators pay a fixed feed-in tariff to solar system owners for electricity exported to the grid. The tariff is guaranteed for 20 years from commissioning, and the rate is locked at the time of registration. Rates degrade at 1% every six months — automatically, on February 1 and August 1 each year.

For systems commissioned between August 2025 and January 2026, the EEG rates are:

| System Size | Export Model | FiT Rate |

|---|---|---|

| Up to 10 kW | Partial (surplus only) | €0.0786/kWh |

| Up to 10 kW | Full injection | €0.1247/kWh |

| 10–40 kW | Partial (surplus only) | €0.0680/kWh |

| 40–100 kW | Partial (surplus only) | €0.0556/kWh |

| 10–100 kW | Full injection | €0.1045/kWh |

For systems above 100 kW, the Marktprämie (market premium) model applies. These systems participate in direct marketing agreements (Direktvermarktung) and receive a top-up above the hourly wholesale price rather than a fixed guaranteed rate.

Solar Peak Act (February 2025): The Solar Peak Act suspends EEG feed-in tariff payments during periods when the electricity spot price in the EPEX day-ahead market is negative. This primarily affects mid-day summer generation when grid oversupply pushes prices below zero — a phenomenon that occurred on over 100 days in Germany during 2024. The practical impact:

- Residential systems with battery storage are largely protected, because stored energy avoids the negative-price window

- Small roof systems without storage lose income only during specific hours, which analysis suggests reduces annual FiT revenue by 2–8% depending on location and system orientation

- South-facing systems in Bavaria are most exposed due to coincidence of peak summer generation and grid oversupply peaks

- Installers should model the Solar Peak Act effect explicitly in financial proposals for new clients, particularly for unshaded south-facing rooftops in southern Germany Shadow analysis software identifies shading issues before installation.

Registration through the Marktstammdatenregister (MaStR) is mandatory before grid connection. Failure to register before commissioning affects FiT eligibility.

Solarpaket I: Simplified Planning and Community Energy

Germany’s Solarpaket I (Solar Package I) was enacted in May 2024 and introduced a range of administrative simplifications:

- Balcony power plants (plug-in PV up to 800W) are now fully exempt from network operator notification requirements and landlord permission requirements in most cases

- Agricultural and commercial rooftops benefit from streamlined permitting procedures under the new Photovoltaic-Beschleunigungsgesetz (PV Acceleration Act) provisions

- Community energy cooperatives have expanded access to the direct marketing premium, allowing smaller aggregated portfolios to participate in the Marktprämie framework

- Tenant electricity models (Mieterstrommodell) have been expanded to allow more building types to implement shared PV for rental housing

For installers working on multi-unit residential and mixed-use commercial projects, Solarpaket I represents meaningful administrative simplification that reduces project timelines.

KfW Financing Programs

KfW 270 — Renewable Energies Standard Loan: KfW’s flagship financing instrument for solar offers loans at subsidised interest rates for residential, commercial, and utility-scale solar PV installations. Key parameters:

- Loan amounts up to €150 million per project

- Repayment terms up to 30 years, with options for repayment-free initial periods

- Fixed interest rate set at commitment — significantly below commercial market rates through the program

- Applied for through the borrower’s own bank (Hausbank), not directly through KfW

- Compatible with KfW 442 and regional Länder grants (for different cost components)

KfW 442 — Solarstrom für Elektroautos: This grant supports residential solar systems paired with battery storage and EV wallboxes. Key parameters: See Adding Battery Storage Services for detailed guidance.

- Grants of up to €3,200 for battery + wallbox combinations meeting minimum specifications

- Minimum battery capacity: 5 kWh

- Applications submitted online through the KfW portal before commissioning begins

- Budget rounds close quickly — Q2 and Q4 application windows typically exhaust within weeks of opening

- Cannot be combined with KfW 270 for the same cost components (but the loan can cover panels while the grant covers storage and wallbox)

Pro Tip

German installers who build proposals using solar design software with integrated EEG FiT rate tables, KfW loan amortisation, and KfW 442 grant values win client sign-off faster than those who present tariff rates in isolation. The client decision point is the monthly net cash flow after loan repayment — not the kWh rate. A proposal showing exactly what the household pays per month net of loan repayment and FiT income removes the most common residential objection.

VAT Exemption on Solar Hardware

Since January 1, 2023, Germany permanently exempts solar PV modules, inverters, batteries, and mounting systems from VAT (Umsatzsteuer) when sold for systems on or near private dwellings up to 30 kWp, and for systems on public and charitable buildings of any size. Key terms:

- The exemption covers both the sale of hardware and its installation (labor is also VAT-exempt for qualifying projects)

- No application is needed — the exemption applies automatically to qualifying transactions

- Installers do not charge VAT; they declare the zero rate on their invoices

- The 19% saving on hardware costs reduces a typical €15,000–€20,000 residential installation cost by €2,850–€3,800

This remains one of the cleanest and most accessible incentives in Europe, requiring no application, no certification, and no annual renewal.

Germany Summary

| Incentive | Type | Amount / Rate | Duration |

|---|---|---|---|

| EEG Einspeisevergütung (up to 10 kW, partial) | Feed-in tariff | €0.0786/kWh | 20 years |

| EEG Einspeisevergütung (up to 10 kW, full inj.) | Feed-in tariff | €0.1247/kWh | 20 years |

| KfW 270 Renewable Loan | Subsidised loan | Up to €150M, subsidised rate | Up to 30 years |

| KfW 442 Battery/EV Grant | Capital grant | Up to €3,200 | One-time |

| VAT exemption on hardware | Tax exemption | 0% VAT (systems up to 30 kWp) | Permanent |

| Länder state grants | Regional grants | Varies by Bundesland | Varies |

| Marktprämie (over 100 kW) | Market premium | Above wholesale price | Contract term |

Italy Solar Incentives 2026

Italy’s incentive picture in 2026 reflects an active transition away from the decade-long Superbonus era. The Superbonus — once 110%, the most generous residential energy subsidy in Europe — has been cut to 50–65%. Scambio sul Posto (net metering) closed to new registrations in September 2025. Yet Italy’s solar market remains strong: irradiance of 1,200–1,600 kWh/m² in the north and 1,500–1,900 kWh/m² in the south, retail electricity prices above €0.28/kWh for residential customers, and the growing CER (Comunità Energetiche Rinnovabili) energy community framework sustain a compelling investment case.

For a full country analysis including regional payback periods and cost tables, see our dedicated guide to Italy solar panel ROI.

Detrazione Fiscale 50% (Ecobonus)

The Detrazione Fiscale 50% is Italy’s primary active tax deduction for residential solar in 2026. It allows homeowners to deduct 50% of qualifying solar installation costs from their personal income tax (IRPEF), spread over 10 equal annual installments. Key parameters:

- Eligible works: Supply and installation of solar PV systems on residential buildings; roof-mounted and integrated systems qualify

- Spending cap: €96,000 per property unit for all combined energy improvement works

- Claimable via: ENEA online portal submission within 90 days of completion of works; installation by a certified professional required

- Transferability: The deduction must be claimed by the taxpayer personally (the 2022–2023 “cessione del credito” credit transfer mechanism has been largely withdrawn for new works)

- Documentation: Energy performance certificate (APE) before and after installation required for the full 50% rate

For properties where the 50% deduction cannot be fully absorbed (insufficient IRPEF liability over 10 years), net present value of the deduction falls — typically to an effective 40–45% at a 4% discount rate. This is an important consideration for lower-income households or properties held by legal entities.

Key Takeaway

The most time-sensitive action for new Italian solar installations in 2026 is registering with GSE promptly after commissioning — for Ritiro Dedicato and, where applicable, CER energy community enrollment. Retroactive GSE registration is permitted but delays the compensation period. For properties in southern Italy, also check regional grant availability; Puglia and Sicilia have active programs that close when annual budgets are exhausted.

Superbonus — Status for 2025–2026

Italy’s Superbonus is a higher-rate tax deduction mechanism that allows homeowners to deduct a larger percentage of qualifying energy improvement costs, where the qualifying conditions are met.

| Intervention Type | Deduction Rate | Deduction Period |

|---|---|---|

| Major retrofit (condominiums) | 65% (subject to spending caps) | 10 years |

| Major retrofit (detached houses, income-tested) | 65% | 10 years |

| Standard residential energy works | 50% | 10 years |

| Solar PV as “following intervention” | 50% (within overall energy retrofit) | 10 years |

Critical conditions for the Superbonus in 2026:

- Solar PV qualifies only as a “following intervention” (intervento trainato) alongside a “leading intervention” (intervento trainante) such as external insulation (cappotto termico) or replacement of a heating system with a heat pump

- Standalone solar-only installations do not qualify for the Superbonus — they qualify only for the standard 50% Detrazione Fiscale

- Homeowners who accessed the Superbonus cannot simultaneously register for Scambio sul Posto (which is closed anyway); they must use Ritiro Dedicato for grid export

- Spending caps apply: €48,000 deductible investment cap for PV within a broader retrofit

For a full analysis of Italy’s Superbonus solar mechanics, eligibility rules, and application process, see our dedicated post on Italy Superbonus solar.

Ritiro Dedicato (Dedicated Withdrawal) via GSE

With Scambio sul Posto closed for new registrations since September 26, 2025, new solar installations in Italy export electricity under the Ritiro Dedicato (RID) mechanism. Under RID, the GSE (Gestore dei Servizi Energetici) acts as the mandatory offtaker for surplus solar generation:

- Hourly zonal pricing: The GSE pays the actual hourly zonal electricity price for each period of export. The average zonal price in Q3 2025 was approximately €0.110/kWh, but prices vary significantly by hour, zone (Nord, Centro-Nord, Centro-Sud, Sud, Sicilia, Sardegna), and season

- ARERA guaranteed minimum price: As an alternative floor, ARERA (Italy’s energy regulator) sets annual minimum prices. For 2025, the guaranteed minimum was €0.1176/kWh for systems up to 100 kW — providing downside protection during periods of low market prices

- Contract duration: For systems installed under the Superbonus, RID conventions run for 5 years with renewal. For standard installations, annual renewal applies

- Registration: Online via the GSE portal for systems up to 20 kW; in-person application for larger installations

The economic comparison between RID and the legacy Scambio sul Posto matters for legacy system owners considering whether to upgrade. SsP provided a “virtual netting” credit that offset grid consumption at the retail rate (approximately €0.28–€0.30/kWh), which is considerably more favourable than the zonal wholesale price under RID. This gap — approximately €0.17–0.19/kWh in 2025 terms — is the central argument for maximising self-consumption on new Italian installations rather than over-sizing for export.

CER — Comunità Energetiche Rinnovabili (Energy Communities)

Italy’s CER (Renewable Energy Community) framework, activated by the January 2024 implementing decree, is the most significant new solar mechanism introduced in this decade. Under the CER decree:

- Groups of residential consumers, businesses, municipalities, and public bodies within the same medium-voltage grid substation area can form a CER

- Shared virtual self-consumption is incentivised at up to €110/MWh (€0.11/kWh) for 20 years, administered by GSE

- An additional “TARI” (waste collection tax) reduction applies in some municipalities for CER participants

- CERs in southern Italy and islands qualify for an additional incentive of up to €130/MWh in some bands

- The total budget committed to CER incentives is €2.2 billion over the program life

For installers, CERs open a new project type: aggregating apartment buildings, small municipalities, and mixed-use commercial-residential blocks into shared solar configurations. The 20-year incentive and the involvement of municipalities as anchor participants in many CER structures provides project financing certainty that single-building residential installations cannot match.

Italy Incentive Status — March 2026

| Program | Status | Notes |

|---|---|---|

| Detrazione Fiscale 50% (Ecobonus) | Active | 10-year income tax deduction; ENEA registration required |

| Superbonus 65% (major condominium retrofit) | Active with conditions | Bundled with leading interventions; spending caps apply |

| Superbonus 50% (standard residential) | Active with conditions | Solar as following intervention only |

| Scambio sul Posto | Closed to new registrations | Existing holders continue until contract expiry |

| Ritiro Dedicato (RID) | Active | GSE administered; ~€0.11/kWh zonal average or ARERA minimum |

| CER energy communities | Active | 2024 Decree operational; up to €110–€130/MWh for 20 years |

| PNRR Agri-PV Grants | Active | €1.5B committed; new rounds processing in 2026 |

| Regional grants (Puglia, Sicilia, Lombardy) | Active (varies) | Budget-limited; verify current status before advising clients |

France Solar Incentives 2026

France’s solar incentive system centres on the Obligation d’Achat (OA) feed-in tariff administered by EDF, the Prime à l’Autoconsommation self-consumption bonus, and reduced TVA. A significant structural shift is underway: the OA tariff for surplus self-consumption (approximately €0.04–€0.065/kWh for small systems) now sits well below the retail electricity cost (€0.2146/kWh as of early 2026), which means the financial case for French residential solar is now primarily built on self-consumption savings and the Prime bonus, not on grid export revenue. Full-injection tariffs for very small systems remain competitive, but the overall market is shifting toward self-consumption models.

For a complete analysis of the French feed-in tariff structure, application process, and historical rate evolution, see our guide to France feed-in tariffs.

Obligation d’Achat (EDF OA) Feed-in Tariff

The EDF OA program requires EDF to purchase solar electricity from eligible installations at CRE-regulated tariffs for 20 years. Rates are reviewed and published quarterly by the Commission de Régulation de l’Énergie (CRE). Q1 2026 rates:

| System Size | Injection Model | Q1 2026 Rate |

|---|---|---|

| Up to 3 kWp | Full injection (vente totale) | €0.2349/kWh |

| 3–9 kWp | Full injection | €0.1996/kWh |

| 9–100 kWp | Full injection | €0.1362/kWh |

| Up to 9 kWp | Surplus (autoconsommation avec vente de surplus) | ~€0.04–€0.065/kWh |

| 100–500 kWp | Removed from OA framework | CRE competitive tender only |

Key Q4 2025 change: Systems between 100 kW and 500 kW were removed from the OA feed-in tariff framework in Q4 2025 and must now participate in CRE competitive tenders (appels d’offres) to access any supported tariff. This was a significant market change for commercial rooftop installers targeting the mid-size commercial segment.

Application process: Install using a QualiPV-certified installer; submit grid connection request (demande de raccordement) through Enedis; accept the Enedis connection offer within 3 months; submit the OA contract request to EDF OA within 18 months of the Enedis offer. The tariff rate is locked at contract signing. Do not commission the system before submitting the OA application — late submissions permanently forfeit eligibility at the prevailing rate and must reapply at the then-current (lower) rate.

Prime à l’Autoconsommation

The Prime à l’Autoconsommation is a capital grant paid over five annual installments to owners of solar self-consumption installations. Current rates for 2025–2026:

| System Size | Annual Bonus (Year 1) | Total Over 5 Years |

|---|---|---|

| Up to 3 kWp | ~€380/kWp/year | ~€1,900/kWp |

| 3–9 kWp | ~€280/kWp/year | ~€1,400/kWp |

| 9–36 kWp | ~€190/kWp/year | ~€950/kWp |

| 36–100 kWp | ~€100/kWp/year | ~€500/kWp |

The Prime can be combined with the surplus OA tariff (autoconsommation avec vente de surplus), but cannot be combined with vente totale (full injection OA). It cannot be combined with MaPrimeRénov’ grants for the same installation. For a 3 kWp system, the Prime represents approximately €5,700 in total payments over 5 years — a meaningful reduction in effective payback period that moves French small-system economics into the 5–7 year range even with the lower surplus export tariff.

TVA (VAT) Reduction

Solar installations on existing residential buildings in France benefit from reduced TVA:

- 10% TVA: Systems under 3 kWp installed by a RGE/QualiPV-certified professional on buildings over 2 years old

- 20% TVA: All other installations (new-build, systems over 3 kWp)

The 10% TVA applies to both equipment and installation labor. On a typical 3 kWp installation costing €6,000–€8,000, the TVA reduction saves €600–€800 compared to the standard 20% rate.

Crédit d’Impôt: Historical Context

France previously operated a Crédit d’Impôt pour la Transition Énergétique (CITE) that covered a range of home energy improvements including solar thermal. PV systems were removed from CITE eligibility in 2014 and replaced by the current OA + Prime framework. MaPrimeRénov’, which replaced CITE from 2020, covers thermal renovation (heat pumps, insulation, windows) and solar thermal collectors, but does not cover PV panels directly — a point of regular confusion for clients who have seen “solar” mentioned in MaPrimeRénov’ communications. Clarifying this distinction for clients who arrive expecting a MaPrimeRénov’ grant for their PV installation is a routine installer task.

France Summary

| Incentive | Type | Amount / Rate | Duration |

|---|---|---|---|

| EDF OA vente totale (up to 3 kWp) | Feed-in tariff | €0.2349/kWh (Q1 2026) | 20 years |

| EDF OA full injection (3–9 kWp) | Feed-in tariff | €0.1996/kWh (Q1 2026) | 20 years |

| EDF OA full injection (9–100 kWp) | Feed-in tariff | €0.1362/kWh (Q1 2026) | 20 years |

| Prime à l’Autoconsommation (up to 3 kWp) | Capital grant | ~€1,900/kWp over 5 years | 5-year payout |

| TVA reduction | Tax incentive | 10% (vs 20%) on eligible systems | Per installation |

| CRE tender premium (over 100 kWp) | Market premium | ~5–7 ct/kWh above wholesale | 20 years |

Spain Solar Incentives 2026

Spain combines Europe’s best solar resource with a self-consumption framework that, when correctly structured, delivers some of the fastest payback periods on the continent. Peak sun hours of 1,700–2,100 annually across most of the peninsula, retail electricity prices above €0.25/kWh, and the bedrock Real Decreto 244/2019 autoconsumo legislation form the foundation. Municipal tax incentives — IBI and ICIO — add meaningful upfront and ongoing savings that are underused by installers unfamiliar with the local municipal level.

For a full technical guide to RD 244/2019 rules, measurement requirements, and collective self-consumption configurations, see our post on Spain net metering benefits.

Real Decreto 244/2019 — Compensación Simplificada

RD 244/2019 allows residential and commercial solar owners to offset their grid electricity consumption against solar generation on a monthly billing cycle (compensación simplificada — Spain’s net metering equivalent). Key terms:

- Surplus credit value: Exported solar electricity is valued at the actual hourly wholesale spot price (PVPC) and credited against that month’s electricity bill

- Credit ceiling: Monthly surplus credits cannot exceed the total electricity bill for that period — no cash payment to the solar owner, and credits do not roll over to future months

- Collective self-consumption: Multiple consumers within 500 metres (with a draft regulation under discussion proposing extension to 5 km for systems up to 5 MW) can share generation from a single installation; reparto coeficientes (sharing coefficients) must be registered

- Registration: All grid-connected PV installations must be registered with the autonomous community energy authority (consejería de industria or equivalent)

The economic impact of compensación simplificada depends heavily on the household load profile. Households with high daytime consumption (work-from-home, electric heating or cooling, EV charging) achieve 60–70% self-consumption rates in southern Spain. Households with low daytime occupancy achieve 35–45%. Accurately modelling the consumption profile — not just the irradiance — is the key differentiator in Spanish solar proposals. Solar proposal software that incorporates hourly consumption profiling alongside generation simulation produces materially more accurate payback figures than tools that use average annual self-consumption assumptions.

IDAE Grants and National Programs

NextGen EU direct grants (RD 477/2021): These grants, funded by the EU Recovery and Resilience Facility, covered 15–40% of residential and commercial solar installation costs depending on system size and applicant profile. The application window has closed, but approved projects have until June 30, 2026 to complete installation. For installers with clients who have approved applications still unexecuted, this June 2026 deadline is the most time-critical item in the Spanish market.

IDAE Innovative Renewables Program (Q1 2026): A new call opened January 14, 2026 and closed February 19, 2026, with €202.5 million for innovative renewable energy projects including advanced solar-storage combinations, hybrid solar-heat pump systems, and smart grid integration. IDAE runs additional grant calls throughout the year; installers and developers should monitor the IDAE self-consumption office for new programs in H2 2026. Read Advanced Solar PV Design Software for a complete walkthrough.

Regional / Autonomous Community Programs: Spain’s 17 autonomous communities each operate parallel subsidy programs. Andalucía’s INEA and INCEA programs (FEDER 2021–2027 funded) were expected Q1–Q2 2026 with capital grants for residential and commercial solar and storage. Cataluña, Madrid, Castilla y León, and the Comunitat Valenciana all have active or expected programs. Amounts and conditions vary significantly — a 20% capital grant in one region may not exist across the border in the next.

Municipal Tax Incentives: IBI, ICIO, IRPF

Three tax-based incentives operate through 2026 and are frequently underused because they require direct engagement with municipal tax authorities:

IBI reduction (property tax): Municipalities can offer up to a 50% reduction in Impuesto sobre Bienes Inmuebles (annual property tax) for properties with solar installations, for up to 5 years. Major cities — Madrid, Barcelona, Seville, Valencia, Zaragoza — typically have formal IBI solar programs. The application is filed separately with the municipal tax office (Oficina de Atención al Contribuyente or equivalent) after installation. On a typical residential property with an annual IBI bill of €400–€800, a 50% discount for 5 years represents €1,000–€2,000 in cumulative savings.

ICIO discount (construction permit tax): The Impuesto sobre Construcciones, Instalaciones y Obras can be discounted by up to 95% for solar installation permits. This is applied at the permit application stage and is one of the most accessible savings, as many municipalities apply it automatically to qualifying permits. On permit costs of €300–€600 for a residential installation, the saving is €285–€570.

IRPF deductions (regional income tax): Most autonomous communities maintain solar IRPF (personal income tax) deductions of 20–60% on installation costs, claimable over one to four years. Specific rates: Andalucía 15%, Madrid up to 20%, Castilla y León up to 15%, Cataluña up to 10%, Aragón up to 20%. These are filed in the annual renta personal income tax return (declaración de la renta) using the appropriate regional deduction codes. Installers who provide clients with the precise deduction amount and code applicable to their region build trust and remove a common post-sale administration barrier.

Pro Tip

Spanish solar proposals that incorporate the compensación simplificada credit alongside IRPF, IBI, and ICIO tax impacts in a single financial model close more decisively than those presenting only the self-consumption savings. Use a generation and financial tool that models monthly self-consumption, hourly PVPC credit values, and the cash flow impact of tax benefits — this produces the complete picture clients need to make a decision. A 10-page proposal that shows year-by-year net benefit including all tax layers is more persuasive than a headline payback number alone.

Spain Summary

| Incentive | Type | Amount / Rate | Duration |

|---|---|---|---|

| Compensación simplificada (RD 244/2019) | Net metering credit | Hourly PVPC spot price, monthly settlement | Ongoing |

| IDAE innovative fund (2026) | Capital grant | Part of €202.5M pool | Program-specific |

| Regional programs (Andalucía, Madrid, etc.) | Capital grant | 15–40% of installation cost | Program-specific |

| IRPF deduction | Regional income tax | 10–20% on installation cost (varies by region) | 1–4 years |

| IBI reduction | Property tax discount | Up to 50% of annual IBI | Up to 5 years |

| ICIO discount | Construction permit tax | Up to 95% discount | At permit stage |

Netherlands Solar Incentives 2026

The Dutch solar market is in one of the most clearly defined policy transitions in Europe: the residential saldering (net metering) scheme that has underpinned household solar economics since the 1990s ends on January 1, 2027. At the same time, the SDE++ large-scale operating subsidy continues for 2026 with an €8 billion budget before its own planned transition to Contracts for Difference from 2027. For Dutch installers, 2026 is a clear sell window for residential: clients who install before year-end secure approximately one final year under saldering before the scheme ends.

SDE++ — Large-Scale Solar Operating Subsidy

The SDE++ (Stimulering Duurzame Energieproductie en Klimaattransitie) provides an operating subsidy for commercial and utility-scale renewable energy production including solar PV. It functions as a sliding-scale market premium:

- The subsidy covers the difference between a fixed base energy price (representing the long-run cost of production) and the actual market electricity price for each production period

- Duration: up to 15 years from commissioning

- 2026 budget: €8 billion

- Application window: specific rounds published by RVO (Rijksdienst voor Ondernemend Nederland)

- Eligible systems: commercial rooftop, ground-mount, and floating solar above residential thresholds

CfD transition from 2027: The Dutch government announced in October 2025 that from 2027 it plans to replace the SDE++ large-scale solar component with two-way Contracts for Difference (CfDs). Under CfDs, subsidy flows in both directions: the government pays when market prices fall below the strike price, and the developer repays when market prices exceed the strike price. This mirrors EU electricity market reform recommendations and affects project financing structures — lenders and equity investors evaluate CfD revenue profiles differently from one-way operating subsidy structures. For projects with commissioning dates in 2027 or beyond, the CfD framework should be incorporated into financial modelling from the outset.

Saldering (Net Metering) — Phase-Out Timeline

The Dutch saldering scheme allows residential solar owners to fully offset their annual electricity consumption against solar generation at a 1:1 exchange ratio. Excess summer production nets against winter consumption within the calendar year at the retail electricity price — the most favourable net metering structure in Europe.

Parliament confirmed in November 2024 that saldering ends on January 1, 2027. After that date:

- Energy suppliers will set their own compensation rate for residential excess solar export

- The government will require compensation to be “reasonable” but will not set a regulatory floor

- The annual 1:1 netting benefit is lost; summer export will be compensated at supplier-determined rates expected to be well below the retail electricity price (likely in the €0.04–€0.08/kWh range based on current voluntary supplier rates)

Implications for Dutch residential solar installers:

- Systems installed and commissioned before January 1, 2027 benefit from saldering for approximately one final year

- The financial case for residential solar after January 2027 shifts entirely to maximising self-consumption, through accurately sized systems and battery storage pairing

- Systems with battery storage installed in 2025–2026 are better positioned for the post-saldering environment than export-optimised oversized systems

- Proposals for 2026 clients should model both the remaining saldering period and the post-2027 self-consumption scenario to show the full 25-year financial picture

Key Takeaway

Dutch installers have a clear sell window in 2026. Residential clients who install before January 1, 2027 secure approximately one final year under full saldering before the scheme ends. Pairing the 2026 installation with battery storage maximises both the remaining saldering benefit and the post-2027 self-consumption economics. Using solar design software that models both the saldering and post-saldering cash flows across a full 25-year period helps clients understand what they are buying — not just the short-term benefit.

Netherlands Summary

| Incentive | Type | Amount / Rate | Duration |

|---|---|---|---|

| SDE++ (commercial/utility) | Operating subsidy / market premium | Gap between base price and market price | Up to 15 years |

| Saldering (residential net metering) | 1:1 annual netting at retail price | Full retail electricity price offset | Until January 1, 2027 |

| Post-2027 residential compensation | Supplier-set tariff | ~€0.04–€0.08/kWh (estimated, no regulatory floor) | From 2027 |

| CfD (large-scale, from 2027) | Two-way Contract for Difference | Strike price TBD by auction | Contract term |

United Kingdom Solar Incentives 2026

The UK solar incentive environment sits outside the EU framework post-Brexit, but remains directly relevant for European solar businesses with UK operations or clients. The UK’s approach has moved firmly toward market-based mechanisms and targeted support for low-income households, having ended the large-scale Feed-in Tariff in 2019.

Smart Export Guarantee (SEG)

The Smart Export Guarantee (SEG), introduced in January 2020, requires all licensed electricity suppliers with over 150,000 customers to offer a tariff for solar electricity exported to the grid. Key terms:

- Rate: Set by individual suppliers — the government mandates only that the rate must be above zero, not a specific amount. 2025–2026 rates from major suppliers: Octopus Energy Outgoing (5.0p/kWh flat rate), E.ON Next Export (5.5p/kWh), OVO Energy (4.0p/kWh), British Gas Solar Export (7.5p/kWh — higher but with conditions)

- Eligibility: MCS-certified solar PV systems of any size up to 5 MW; a smart meter must be installed

- Duration: Ongoing — no fixed term, but suppliers review rates periodically

- No registration fee: Application made directly to the energy supplier after commissioning and MCS registration

SEG rates are materially lower than the historic Feed-in Tariff (which provided 41.3p/kWh for early schemes). The economic case for UK residential solar is now almost entirely built on self-consumption savings, with SEG providing supplementary income on exported surplus. At UK retail electricity prices of approximately 24–28p/kWh (Q1 2026, after the Energy Price Cap), self-consumption avoidance savings significantly exceed SEG export income.

MCS Certification and Its Role

MCS (Microgeneration Certification Scheme) certification is the mandatory quality standard for UK residential and small commercial solar installations accessing SEG and other support mechanisms. MCS certification covers:

- Installer accreditation: Installers must hold MCS certification for PV systems to install eligible systems

- Product approval: PV panels and inverters must be on the MCS product list

- Installation certificate: Each completed installation generates an MCS installation certificate, which is required for SEG applications, warranty claims, and Building Regulations compliance

For UK installers, MCS certification is a prerequisite for operating in the residential market. The certification body operates a public database of MCS-certified installers, which many consumers use as their primary selection criterion. Non-MCS installations are legally installed but exclude clients from SEG, some mortgage products (lenders increasingly ask for MCS certificates), and future incentive programs.

ECO4 (Energy Company Obligation)

ECO4 is the current phase of the Energy Company Obligation scheme, requiring large energy suppliers to fund energy efficiency improvements in low-income, fuel-poor, and vulnerable households. Solar PV is an eligible ECO4 measure when installed as part of a broader home energy upgrade package:

- Who qualifies: Households receiving qualifying benefits (Universal Credit, Housing Benefit, Child Tax Credit, others) or referred through the Great British Insulation Scheme

- What is funded: The full cost of solar PV installation, when combined with insulation, heat pumps, or other primary energy efficiency measures

- Target: 1 million homes through the scheme period (extended to 2026)

- Installer access: Installers must be TrustMark and MCS certified to participate in ECO4

For solar installers focused on the social housing and low-income residential market, ECO4 provides a funded pipeline of installations where the customer pays nothing. The challenge is navigating the supply chain — most ECO4 work is channelled through managing agents and larger contractors rather than directly to installers.

UK Summary

| Incentive | Type | Amount / Rate | Duration |

|---|---|---|---|

| Smart Export Guarantee (SEG) | Export tariff | 4.0–7.5p/kWh (supplier-dependent, 2026) | Ongoing |

| ECO4 | Full cost grant (low-income) | Full installation cost, qualifying households | Until 2026 |

| VAT zero rate (residential PV) | Tax relief | 0% VAT on residential PV installation (reinstated 2022) | Ongoing |

Note: UK residential solar PV installation has been zero-rated for VAT since April 2022, reducing a typical installation cost by approximately £1,000–£2,000.

Poland Solar Incentives 2026

Poland has undergone significant policy evolution for residential solar since April 2022, when it replaced net metering with a net billing system for all new installations. The transition reduced financial returns for small solar owners but has been partially offset by the Mój Prąd grant program and a favourable reduced VAT rate. Poland’s utility-scale solar market continues to expand through annual OZE auctions.

Mój Prąd (My Electricity) Grant Program

Mój Prąd is Poland’s principal residential solar grant program, supporting installations of 2–10 kWp. The program has run through multiple rounds, with round 6 concluding in 2025 and round 7 anticipated in H1 2026. Key parameters from recent rounds:

- Base PV grant: PLN 6,000–7,000 (approximately €1,400–€1,650) for systems of 2–10 kWp

- Battery storage bonus: Additional PLN 16,000 (approximately €3,750) for qualifying battery storage systems

- Heat pump bonus: Additional PLN 5,000–7,000 for qualifying heat pump installation alongside solar

- EMS (energy management system) bonus: PLN 3,000 for smart energy management systems

- Maximum total grant: Up to PLN 31,000 (approximately €7,250) for PV + battery + heat pump + EMS combination

Under net billing with Mój Prąd support, small PV installations of 4–5 kWp achieve internal rates of return of 19–25% according to national energy agency modelling — making Poland one of the stronger residential solar markets in Central and Eastern Europe despite the net billing transition. The grant applies per property per applicant and cannot be combined with certain regional subsidy programs; check compatibility before advising clients.

Net Billing System

Residential prosumers in Poland registered after April 1, 2022 sell surplus electricity to the grid at the actual hourly spot price (monthly settlement) and purchase grid electricity at the full retail tariff. The monthly netting deficit — buying at retail, selling at wholesale — is the primary source of payback extension compared to the legacy net metering system.

Installations registered before April 1, 2022 continue under the legacy net metering system for 15 years from their registration date. For installers with legacy clients considering system expansions or inverter replacements, maintaining net metering eligibility — or the risk of losing it — requires careful technical and regulatory advice.

Virtual prosumer (from July 2024): Poland allows virtual prosumers — tenants, apartment residents, and consumers who cannot install their own rooftop solar — to purchase a share in a nearby solar farm’s capacity and settle consumption under the net billing framework as if it were their own rooftop system. This mirrors the Italian CER model and the Spanish collective self-consumption framework, and opens a new project type for developers: community solar farms serving registered virtual prosumers.

OZE Auctions (Utility-Scale)

Poland’s annual OZE (Odnawialne Źródła Energii) auctions provide 15-year price support contracts for utility-scale renewable energy. The Energy Regulatory Office (URE) conducts auction rounds with differentiated baskets by technology and system size. Polish utility-scale solar has grown rapidly, with auction-backed projects driving several hundred megawatts of new capacity per year. For developers with the capacity to navigate the regulatory process, OZE auctions provide long-term revenue certainty that commercial solar in Western Europe cannot match at equivalent scale.

VAT Reduction

Poland applies a reduced 8% VAT rate (from the standard 23%) on solar power systems under 50 kW for residential and agricultural applications, and on installation services for these systems. This 15-percentage-point reduction represents a meaningful cost saving on a typical residential installation: on a PLN 35,000 system (approximately €8,200), the VAT saving relative to the standard rate is PLN 5,250 (approximately €1,230).

Poland Summary

| Incentive | Type | Amount / Rate | Duration |

|---|---|---|---|

| Mój Prąd grant (PV only) | Capital grant | PLN 6,000–7,000 (~€1,400–€1,650) | Per-installation |

| Mój Prąd grant (PV + battery + heat pump + EMS) | Capital grant | Up to PLN 31,000 (~€7,250) | Per-installation |

| Net billing | Grid export payment | Hourly spot price, monthly settlement | Ongoing |

| OZE auction support (utility-scale) | 15-year price contract | Auction-set strike price | 15 years |

| VAT reduction | Tax reduction | 8% (vs 23%) on systems under 50 kW | Ongoing |

Other EU Markets: Austria and Belgium

Austria

Austria operates one of Europe’s most systematic grant programs for rooftop solar through the EAG (Erneuerbaren-Ausbau-Gesetz — Renewable Energy Expansion Act) investment subsidy framework, administered by OeMAG.

EAG Investitionszuschuss (Investment Grant): Covers 20–30% of total system costs for eligible PV installations. The Q2 2026 call opens April 23, 2026, with a budget of €40 million. Earlier 2025 rounds had budgets of €60–€135 million and were oversubscribed; grants are awarded on a first-come, first-served basis within the application window.

“Made in Europe” bonus: Austria introduced a 20% funding uplift for PV systems and storage using European-manufactured components. OeMAG maintains a published White List of qualifying products. The uplift raises the effective grant from 20–30% to 24–36% of qualifying costs for projects using EU-manufactured panels and inverters — a meaningful advantage for installers who have supplier relationships with European manufacturers (notably those from Germany, France, and Austria itself).

Market premium (OeMAG): For larger installations above the grant thresholds, OeMAG operates a feed-in premium auction providing a market premium above the spot price for a fixed period.

VAT: Austria applies a 0% VAT rate on solar systems for private households, in line with the EU VAT directive that has permitted member states to reduce VAT on solar PV hardware to zero since April 2022.

Regional programs: Austrian Bundesländer — particularly Niederösterreich, Steiermark, and Tirol — operate parallel grant programs that can in many cases be stacked with the federal EAG grant.

Belgium

Belgium’s solar incentive structure is decentralised across three regions: Flanders, Wallonia, and Brussels-Capital.

Flanders: The prosumer tariff (prosumententarief) applies to residential solar owners — a grid usage fee assessed on estimated self-consumption. Net metering for Flemish residential solar was replaced by a digital meter system (digitale meter), with separate injection and offtake measurement. Compensation for surplus injection is set by energy suppliers; typical 2026 injection compensation rates range from €0.04–€0.08/kWh. Flemish residential solar economics are primarily driven by self-consumption savings. Also see: Us Residential Solar Market Trends 2026.

Wallonia: Wallonia operates a certificate system (Certificats Verts) where qualifying solar installations earn certificates based on CO₂ savings. Certificates can be sold to obligated grid operators. The Walloon Energy Fund also provides direct grants for residential solar.

Brussels-Capital: The Brussels region offers grants under the RENOLUTION renovation support program, applicable to solar installations in combination with other energy renovations.

Federal VAT: A temporary VAT reduction to 6% (from 21%) on solar PV for residential buildings applies in Belgium; verify the current status and duration with a local installer as this measure has been subject to change.

EU-Wide Programs: REPowerEU ETS Funding and Innovation Fund

Beyond national programs, several EU-level funding mechanisms are directly accessible or indirectly relevant to solar developers across Europe.

Innovation Fund

The EU Innovation Fund, financed from EU ETS auction revenues, provides grants for large-scale innovative clean energy projects. As of 2025–2026, the Innovation Fund has disbursed €38 billion in committed funding. Solar projects — particularly large-scale utility solar, floating solar, and integrated solar-storage systems in lower-income member states — have received Innovation Fund grants covering up to 60% of eligible project costs. The fund operates through open calls managed by the European Climate, Infrastructure and Environment Executive Agency (CINEA). Project minimum size thresholds mean the Innovation Fund is relevant primarily to utility-scale developers rather than residential installers.

Cohesion Fund and ERDF

European Structural Funds — the European Regional Development Fund (ERDF) and the Cohesion Fund — remain the primary EU-level mechanism for solar infrastructure investment in Central and Eastern Europe. Countries including Poland, Romania, Hungary, Bulgaria, Croatia, and Slovakia receive substantial ERDF allocations that include solar components. These funds flow through national and regional operational programs, supplementing domestic budgets for grant programs such as Mój Prąd (Poland) and equivalent programs in other recipient states.

NER300 and Historical Programs

NER300, an earlier EU mechanism funded from carbon permit revenues, supported large-scale renewable energy projects from 2012–2020. Its successor programs — the Innovation Fund and the Modernisation Fund (for Central and Eastern European states) — continue the model. The Modernisation Fund specifically supports energy system modernisation in 10 lower-income EU member states and has channelled funding toward solar capacity additions in Romania, Poland, Czech Republic, Slovakia, Hungary, and Bulgaria.

Model European Incentive Stacks for Any Country

SurgePV’s generation and financial tools support country-specific incentive modelling — EEG FiT rates, OA tariffs, SDE++ premiums, Superbonus deductions, and tax benefits — so your proposals reflect current policy accurately.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

Free Tool

Try our solar incentive finder to check which grants, tax credits, and feed-in tariffs apply to your project location.

Further Reading

For a deeper look at how EU-wide directives shape national programs, explore our EU solar policy guide.

How to Stack Incentives: Three Worked Examples

Understanding individual incentive programs is necessary but not sufficient. The financial case that wins client sign-off requires calculating the combined effect of all applicable mechanisms on a specific project. The following three examples show how to build that analysis for Germany, France, and Spain — the markets where incentive stacking has the most moving parts. The same methodology applies across all European markets using solar design software with country-specific financial modelling capability.

Worked Example 1: Germany — 12 kWp Residential, Bavaria

Project: 12 kWp rooftop PV, 10 kWh LFP battery, EV wallbox. Munich, Bavaria. Family of four, 7,200 kWh annual consumption.

Step 1 — Identify applicable incentives:

- EEG feed-in tariff (partial export, 10–40 kW band): €0.0680/kWh on surplus

- KfW 270 loan: 25-year term at subsidised fixed rate (approximately 3.5% in early 2026)

- KfW 442 grant: Up to €3,200 for battery + wallbox

- VAT exemption: 0% on panels, inverter, battery, mounting (system is 12 kWp, under 30 kWp threshold)

- Bavarian BayernFonds: Check current call — varies by year, typically 10–15% capital grant

Step 2 — Model self-consumption and export split:

Using a generation and financial tool with Munich irradiance data (approximately 950 kWh/kWp annual specific yield) and the household load profile:

- Annual generation: 11,400 kWh (12 kWp × 950 kWh/kWp)

- Self-consumption with 10 kWh battery: approximately 8,100 kWh (71%)

- Grid export: approximately 3,300 kWh

- Self-consumption without battery for reference: approximately 5,700 kWh (50%) — the battery adds 2,400 kWh of additional self-consumption

Step 3 — Calculate annual financial benefit:

| Component | Calculation | Annual Value |

|---|---|---|

| EEG FiT income on export | 3,300 kWh × €0.0680/kWh | €224 |

| Grid electricity savings | 8,100 kWh × €0.32/kWh (Munich retail tariff) | €2,592 |

| KfW 442 grant (annualised over system life) | €3,200 ÷ 20 years | €160 |

| VAT saving on hardware (annualised) | 19% × ~€18,000 hardware cost ÷ 20 years | €171 |

| Total annual benefit | ~€3,147 |

Step 4 — Net against financing cost: KfW 270 loan of €25,000 (full system cost after KfW 442 grant applied to battery/wallbox components) at 3.5% over 25 years = approximately €1,250/year repayment. Net annual benefit after financing: ~€1,897. Payback including KfW 442 grant: approximately 7–8 years. Total net benefit over 20-year FiT period: approximately €22,000–€28,000 after repaying the loan.

Solar Peak Act impact: Modelling suggests approximately 85–200 hours of annual negative price periods in Munich, affecting approximately 3–6% of annual export volume. For this system with battery storage, estimated annual FiT reduction due to Solar Peak Act: €8–€14. Immaterial for the financial case, but should be disclosed in client proposals.

Worked Example 2: France — 6 kWp Residential, Toulouse

Project: 6 kWp rooftop PV, surplus autoconsommation model. Toulouse, Occitanie. Annual generation estimated at 7,200 kWh (1,200 kWh/kWp for south-west France).

Incentives applicable:

- Prime à l’Autoconsommation (6 kWp, 3–9 kWp band): €280/kWp/year × 5 years = €1,400/kWp total → €8,400 over 5 years for 6 kWp

- EDF OA surplus tariff: surplus export at approximately €0.065/kWh (3–9 kWp band)

- TVA: 20% applies (system is 6 kWp — 10% TVA threshold is 3 kWp only)

- Self-consumption savings at French retail electricity price: approximately €0.2146/kWh (Q1 2026 TRV tariff)

Annual benefit calculation:

| Component | Calculation | Annual Value |

|---|---|---|

| Self-consumption savings (est. 55% of generation) | 3,960 kWh × €0.2146/kWh | €850 |

| OA surplus income on export | 3,240 kWh × €0.065/kWh | €211 |

| Prime à l’Autoconsommation (years 1–5) | €8,400 ÷ 5 years | €1,680/year |

| Annual benefit (first 5 years) | ~€2,741 | |

| Annual benefit (years 6–20, no Prime) | ~€1,061 |

Total installed cost: approximately €12,000 (6 kWp professional installation, 20% TVA). Simple payback including Prime bonus: approximately 5–6 years. Payback on ongoing benefits alone (years 6+): 10–11 years from installation, but the full 20-year NPV is strongly positive due to the front-loaded Prime payments. For French clients, presenting the first-5-year cash flow and total 20-year return together — not just the payback headline — improves close rates.

Worked Example 3: Spain — 8 kWp Residential, Seville

Project: 8 kWp rooftop PV, no battery. Seville, Andalucía. Annual generation: 12,000 kWh (1,500 kWh/kWp for southern Spain).

Incentives applicable:

- Compensación simplificada at PVPC spot price (~€0.12/kWh annual average, 2025)

- IRPF deduction: 15% on installation costs (Andalucía regional rate)

- IBI reduction: Seville municipality 50% for 5 years (verify current program status)

- ICIO discount: 95% at permit stage

Annual benefit calculation:

| Component | Calculation | Annual Value |

|---|---|---|

| Self-consumption savings (est. 60% of generation) | 7,200 kWh × €0.25/kWh (Seville retail tariff) | €1,800 |

| Compensación simplificada on surplus | 4,800 kWh × €0.12/kWh (PVPC average) | €576 |

| IBI saving (50% of €400/year annual IBI) | Annualised over 5-year benefit period | €200 |

| IRPF deduction (15% × €10,000 cost, over 4 years) | €1,500 ÷ 4 years | €375 |

| Annual benefit (first 5 years) | ~€2,951 | |

| Annual benefit (years 6–20) | ~€2,376 |

ICIO discount at permit stage reduces upfront cost by approximately €475 (95% × €500 permit fee). Net installed cost: approximately €10,000 − €475 ICIO + IRPF PV of €1,500 deduction ≈ effective €8,025 at close. Simple payback: approximately 2.7–3.5 years — among the fastest in Europe for residential solar, driven by the combination of high irradiance, high self-consumption at 60%, retail electricity price above €0.25/kWh, and municipal tax incentives.

Incentive Comparison: Europe at a Glance

The table below summarises the current incentive environment for a typical 8–12 kWp residential rooftop installation across the eight markets covered in this guide.

| Country | Best Export Rate | Key Grant/Deduction | Tax Benefit | Approx. Payback |

|---|---|---|---|---|

| Germany | €0.0786–€0.1247/kWh (EEG, up to 10 kW) | KfW 442: up to €3,200 | 0% VAT on hardware | 7–9 years |

| France | €0.1996–€0.2349/kWh (OA full injection, up to 9 kWp) | Prime: up to ~€1,900/kWp | 10% TVA (up to 3 kWp) | 5–8 years |

| Spain | PVPC spot ~€0.10–€0.14/kWh | IDAE/regional grants 15–40% | IBI 50%, ICIO 95%, IRPF 10–20% | 3–7 years |

| Italy | ~€0.11/kWh RID (zonal average) | Superbonus 50–65% tax deduction | 50–65% income tax deduction | 5–10 years |

| Netherlands | Saldering 1:1 retail rate (until Jan 2027) | SDE++ for commercial only | None for residential | 6–9 years (pre-2027) |

| UK | 4.0–7.5p/kWh SEG | ECO4 (low-income households) | 0% VAT on residential PV | 8–12 years |

| Austria | OeMAG premium auction | EAG grant 20–30% (+ 20% EU bonus) | 0% VAT on residential PV | 7–10 years |

| Belgium | €0.04–€0.08/kWh (supplier-set) | Regional grants (varies) | 6% VAT (temporary) | 8–12 years |

| Poland | Hourly spot price, net billing | Mój Prąd up to PLN 31,000 | 8% VAT on systems under 50 kW | 6–9 years |

Payback estimates assume average local solar irradiance, typical household consumption profiles, and retail electricity prices as of early 2026. Individual results vary significantly based on system design, shading, consumption patterns, and incentive rates at time of application.

Pro Tip

The calculations above assume no shading correction. In dense urban environments — a Munich townhouse with adjacent buildings to the south, or a Seville rooftop with chimney obstructions — actual yield can fall 10–25% below the unobstructed figure. Always run a shading simulation before presenting financial projections. A solar proposal software tool that incorporates accurate shading analysis alongside incentive stacking produces proposals that hold up to client scrutiny — and survive competitive bids from installers who present inflated numbers.

Key Deadlines and Action Items for 2026

For solar professionals working across European markets, the following dates and actions are the highest-priority items before year-end:

Netherlands — December 31, 2026: Final opportunity for residential clients to commission under saldering. Systems installed before this date secure approximately one final year of 1:1 netting. After January 1, 2027, compensation rates are supplier-determined with no regulatory floor.

Spain — June 30, 2026: Completion deadline for projects with approved NextGen EU grants under RD 477/2021. Approved applicants who have not yet installed face grant forfeiture if systems are not commissioned by this date.

Italy — Ongoing: GSE registration for Ritiro Dedicato should be completed promptly after commissioning. The CER application window for energy communities is open; municipalities and building associations considering CER formation should begin the GSE registration process now, as administrative timelines can run 3–6 months.

Austria — April 23, 2026: Q2 2026 EAG investment grant call opens. Applications are first-come, first-served and the €40M budget will exhaust quickly. Installers with Austrian projects in pipeline should prepare applications in advance.

Germany — Ongoing: Marktstammdatenregister (MaStR) registration must be completed before grid connection. For projects targeting the KfW 442 grant, applications must be submitted before commissioning begins — not after. KfW 442 budget rounds fill within weeks of opening.

France — Per commissioning date: OA feed-in tariff rate is locked at the CRE rate applicable at the time of OA contract submission — not at the time of commissioning. Rates degrade quarterly. Installers who delay OA application after grid connection lock in a lower rate.

Poland — H1 2026 (anticipated): Mój Prąd round 7 is expected in H1 2026. Applications under earlier rounds established the template; round 7 eligibility and amounts may be refined. Monitor the NFOŚiGW (National Fund for Environmental Protection and Water Management) portal for the opening date.

Frequently Asked Questions

What solar incentives are available in Europe in 2026?

European solar incentives in 2026 span four main types: feed-in tariffs (Germany EEG, France OA), market premiums (Netherlands SDE++, Germany Marktprämie), direct capital grants (Austria EAG, Poland Mój Prąd, France Prime à l’Autoconsommation), and tax deductions or VAT reductions (Italy Superbonus 50%, Germany 0% VAT, Spain IBI/ICIO discounts). Most markets now combine multiple mechanisms — the strongest financial cases stack two or three layers simultaneously. The EU-wide RED III framework requires all member states to maintain incentive environments compatible with the 42.5% renewable target by 2030, which provides a structural floor under national programs. See individual country sections above for current rates and eligibility rules.

Which European country has the best solar incentives?

Germany offers the deepest incentive stack in 2026: EEG feed-in tariffs guaranteed for 20 years, KfW 270 low-interest loans up to €150 million per project, KfW 442 grants for battery storage and EV charging (up to €3,200), and a permanent 0% VAT exemption on solar hardware for systems up to 30 kWp. France offers the highest pure feed-in tariff rates for small systems — up to €0.2349/kWh for systems under 3 kWp under full injection as of Q1 2026. Italy’s Superbonus, now at 50–65%, is the highest residential tax deduction rate in Europe. Spain delivers the fastest payback in sun-rich southern regions, where high irradiance, high self-consumption rates, and IBI/ICIO municipal tax incentives push residential payback below four years in cities like Seville and Málaga.

Is Germany’s solar feed-in tariff still active in 2026?

Yes. Germany’s EEG feed-in tariff remains active for newly commissioned systems and is guaranteed for 20 years at the rate applicable at commissioning. For systems up to 10 kW commissioned between August 2025 and January 2026, the partial export rate is €0.0786/kWh and the full injection rate is €0.1247/kWh. Rates degrade at 1% every six months. The Solar Peak Act of February 2025 suspends FiT payments during negative grid price periods, but the practical impact is small for systems with battery storage and amounts to 2–8% of annual FiT revenue for export-optimised unshielded systems. Registration via Marktstammdatenregister (MaStR) is mandatory before grid connection.

What are France’s current solar grant and tariff rates?

France’s main solar incentives in 2026 are the Obligation d’Achat (OA) feed-in tariff (up to €0.2349/kWh for systems under 3 kWp under full injection, Q1 2026 CRE rates), the Prime à l’Autoconsommation (up to approximately €1,900/kWp total over 5 years for systems under 3 kWp), and reduced TVA of 10% on installations under 3 kWp on existing residential buildings. Systems over 100 kWp must enter the CRE competitive tender process. MaPrimeRénov’ covers thermal renovations and heating systems, not PV directly — a common client misconception. See our dedicated France feed-in tariffs guide for the full OA application process and rate history.

How does Spain’s autoconsumo net metering work?

Spain’s autoconsumo framework under Real Decreto 244/2019 allows solar owners to offset their monthly grid electricity bill against solar generation (compensación simplificada). Surplus credits are valued at the hourly wholesale spot price (PVPC) and applied against that month’s bill; credits cannot exceed the bill value and do not roll over. Tax incentives include IBI property tax reductions (up to 50%) at municipal level, ICIO construction permit tax discounts (up to 95%), and regional IRPF income tax deductions (10–20% depending on the autonomous community). For the full technical detail, see our post on Spain net metering benefits.

Is Italy’s Superbonus still available for solar in 2026?

Italy’s Superbonus has been reduced from 110% to 50–65% depending on intervention type. In 2026, standalone solar PV installations qualify only for the standard Detrazione Fiscale 50%, not the Superbonus. Solar PV installed as a “following intervention” alongside a qualifying “leading intervention” (external insulation or heat pump replacement) qualifies for 50–65% under the Superbonus framework. Scambio sul Posto (net metering) closed to new registrations in September 2025; new installations use Ritiro Dedicato (RID) via GSE. For the full picture see our guide to Italy Superbonus solar and the Italy solar panel ROI analysis.

Is Dutch net metering (saldering) ending?

Yes. The Dutch parliament confirmed in November 2024 that the saldering (net metering) scheme ends on January 1, 2027. Systems commissioned before that date benefit from saldering for approximately one final year. After January 1, 2027, energy suppliers set their own compensation rates for residential surplus export without a regulatory floor — rates are expected in the €0.04–€0.08/kWh range. The SDE++ large-scale operating subsidy continues for 2026 with an €8 billion budget, before transitioning to two-way Contracts for Difference from 2027.

What is Poland’s Mój Prąd program and how much is the grant?

Mój Prąd is Poland’s primary residential solar grant program for systems of 2–10 kWp. Recent rounds have provided PLN 6,000–7,000 (approximately €1,400–€1,650) for PV only, with additional grants of PLN 16,000 for battery storage, PLN 5,000–7,000 for heat pumps, and PLN 3,000 for energy management systems — up to PLN 31,000 (approximately €7,250) in total for a full combination package. Round 7 is anticipated in H1 2026. Poland also applies a reduced 8% VAT rate (from standard 23%) on solar systems under 50 kW and their installation.

How does the EU’s REPowerEU plan affect solar incentives?

REPowerEU, launched in May 2022, set a 600 GW solar target by 2030 and channelled €210 billion in investment across Europe to reduce energy dependency. Its direct effects on solar incentives operate through national Recovery and Resilience Plans (PNRR), which each member state submitted to the European Commission. Italy’s PNRR committed €1.5 billion to agri-PV; Spain’s NextGen EU grants funded billions in residential and commercial solar via RD 477/2021; Poland’s recovery plan extended the Mój Prąd grant program. RED III, enacted as part of the broader Fit for 55 package, mandates the 42.5% renewable energy target by 2030 and 12-month permitting caps in designated acceleration areas, creating a structural incentive for member states to maintain solar support programs.

Which European solar incentive programs have the best ROI for commercial installers?

For commercial installers, the strongest 2026 programs are: Germany’s Marktprämie (market premium) for systems over 100 kW through direct marketing agreements, with 20-year revenue certainty and no Solar Peak Act suspension risk for properly structured aggregated portfolios; Netherlands SDE++ for large commercial and utility-scale solar (€8 billion 2026 budget, up to 15-year term); Italy’s CER energy community incentive (up to €110/MWh for 20 years) for municipality and apartment-building aggregations; and Austria’s EAG Investitionszuschuss for mid-scale commercial rooftop with the Made in Europe bonus uplift. The UK’s SEG is too low-rate for commercial-scale economics; Belgium’s regional programs are too fragmented and volume-limited for large commercial projects.