Quick Answer

Solar installer cash flow management requires milestone-based payments (30% deposit, 40% at installation, 30% at commissioning) and 30–60 day collection cycles. Working capital needs average 15–25% of annual revenue. Financing options: equipment supplier credit, invoice factoring, and construction loans.

A 40-crew solar installer in Phoenix called me in March 2025. The pipeline was full. The sales team had crushed Q1. The crews were booked through May. The CEO did not know how to make payroll on Friday.

Solar installer cash flow management requires milestone-based payments (30% deposit, 40% at installation, 30% at commissioning) and 30–60 day collection cycles. Working capital needs average 15–25% of annual revenue. Financing options: equipment supplier credit, invoice factoring, and construction loans. For more on this topic, see Solar Sales Commission Structure.

Solar installer cash flow management requires milestone-based payments (30% deposit, 40% at installation, 30% at commissioning) and 30–60 day collection cycles. Working capital needs average 15–25% of annual revenue. Financing options: equipment supplier credit, invoice factoring, and construction loans.

This is not unusual. Solar installers do not fail because they cannot sell. They fail because they cannot manage the gap between paying suppliers and getting paid by customers. The average residential solar project takes 90 to 120 days from contract to PTO. The installer pays for panels, inverters, and labor inside the first 30 days. The customer payment lands 60 to 90 days later. Multiply that gap across 50 active projects and the math becomes obvious.

Quick Answer: Solar Installer Cash Flow Management

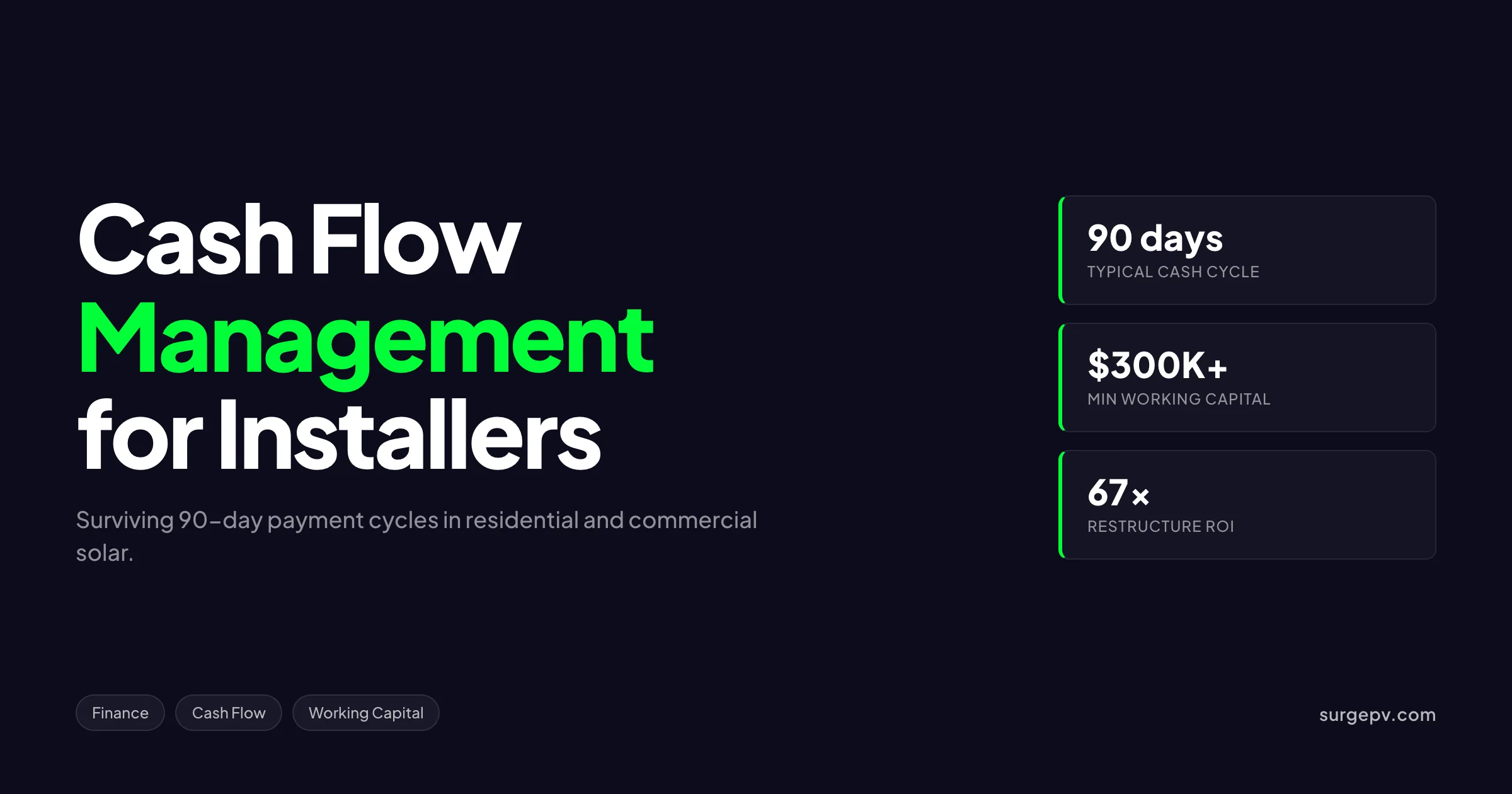

Solar installer cash flow management balances supplier payables (30-day terms) against customer receivables (60-90 day cycles). Successful installers solve the gap with dealer-financed loans that pay at install, customer deposits at signing, and 90 days of working capital reserves. Get this wrong and even a profitable installer goes bankrupt during a growth spurt.

In this guide:

- Why solar cash cycles look different from any other trade

- The real numbers behind a 90-day payment cycle

- Financing options that close the gap (dealer fees, milestone billing, factoring)

- How to structure customer payment terms to protect cash

- Working capital benchmarks for installers at every size

- The tax and incentive timing that catches installers off-guard

- What most installers get wrong about cash flow

- Eight common questions about solar installer cash management

Why Solar Cash Cycles Are Worse Than Other Trades

A roofing contractor gets paid when the job is done. A plumber gets paid before they leave. A solar installer gets paid weeks after the equipment is installed, often after a utility inspection that the installer does not control.

Solar payment cycles depend on three external parties. The customer needs financing approved. The Authority Having Jurisdiction (AHJ) — your local building department — must pass the final inspection. The utility must issue Permission To Operate (PTO). Each step adds 7 to 30 days of delay. None of them care about your payroll schedule.

The Standard Solar Installer Cash Cycle

Here is a typical residential project cash timeline:

| Day | Event | Cash Impact |

|---|---|---|

| 0 | Contract signed | Deposit received (if collected) |

| 14 | Engineering complete | Pay design fees |

| 21 | Panels ordered | Distributor invoice issued (net 30) |

| 35 | Materials delivered | Inverter, racking arrive |

| 42 | Install day | Pay crew labor + remaining suppliers |

| 60 | Inspection pass | No cash event |

| 90 | PTO granted | Final customer payment due |

| 105 | Customer pays | Cash received |

A $20,000 residential system costs an installer roughly $13,000 to deliver. Of that, $8,000 goes to materials within 30 days. $3,500 goes to labor inside 42 days. The installer carries that $13,000 outlay for 90 to 105 days before the customer payment closes the loop.

Now scale that to 10 active projects per month. The installer is carrying $130,000 of outflows against $0 in matching receivables for the first 30 days of each project. After three months at steady state, the installer carries $390,000 in working capital just to keep the lights on.

Key Takeaway

A solar installer running 10 residential systems per month at $20,000 average price needs $300,000 to $450,000 in working capital. Less than that and a single PTO delay can trigger a payroll crisis.

Commercial Solar Makes the Problem Worse

Residential cash cycles are 60 to 90 days. Commercial cycles run 120 to 180 days. The system is bigger, so the supplier invoices are larger. Procurement timelines are longer. The customer is a property owner who pays on net 60 or net 90 terms, not a homeowner with financing in place at signing.

A 500 kW commercial rooftop project costs an installer $700,000 to $850,000 to deliver. The customer pays 30% at contract, 30% at material delivery, 30% at substantial completion, and 10% at PTO. Each milestone is a separate invoice that takes 30 to 45 days to clear. Many commercial customers contest the final 10% retainage for 60 to 90 days, citing punch-list items that may or may not exist.

This is why most solar installers stay residential until they have at least $1 million in working capital. The commercial business model requires balance-sheet strength that small installers do not have.

The Real Numbers Behind a 90-Day Cash Cycle

Most installers track revenue. Few track cash. The two are not the same.

Revenue recognition for solar follows the percentage-of-completion method under ASC 606. You recognize revenue as the job progresses. Cash hits the bank when the customer pays. The gap between revenue and cash is where installers go broke.

Cash Conversion Cycle (CCC)

The cash conversion cycle is the single best metric for solar installer financial health. CCC measures how many days your cash is locked up between supplier payment and customer collection.

Formula: CCC = DSO + DIO − DPO

- DSO (Days Sales Outstanding) = average days to collect customer payment

- DIO (Days Inventory Outstanding) = average days inventory sits before installation

- DPO (Days Payable Outstanding) = average days you take to pay suppliers

For a healthy solar installer:

| Metric | Healthy | At Risk | Crisis |

|---|---|---|---|

| DSO | Under 45 days | 45-75 days | Over 75 days |

| DIO | Under 21 days | 21-45 days | Over 45 days |

| DPO | 30-45 days | Under 25 days | Under 15 days |

| CCC | Under 30 days | 30-75 days | Over 75 days |

If your CCC is 90 days, you need to fund 90 days of operating expense before you ever see a dollar of profit. For a $5 million annual revenue installer with 15% margins, that is roughly $1 million in working capital just to operate. Most installers at this size have $200,000 to $400,000 in working capital. The shortfall comes from credit lines, owner contributions, or delayed payroll.

The Hidden Costs of Slow Collection

A delayed receivable does not just hurt cash. It compounds across operations:

- Late supplier payment damages your distributor relationship and pricing

- Late payroll triggers crew turnover, which costs $5,000 to $15,000 per replacement

- Late tax payments add 5 to 10% penalty plus interest

- Late insurance premium triggers policy lapse, blocking new permits

- Credit line drawdowns to cover shortfalls compound at 8 to 12% annual interest

A $50,000 late receivable can easily generate $5,000 to $10,000 in cascading costs across these areas. Multiplied across a year, the financial penalty for poor collection often exceeds the gross margin on the underlying project.

Financing Options That Close the Cash Gap

Solar installers have four primary tools to close the gap between paying suppliers and getting paid. Each has a cost. Picking the wrong tool costs more than picking the right one.

Dealer Fee Financing (Mosaic, GoodLeap, Sunlight)

Third-party consumer lenders pay the installer 70 to 95% of system price at install. The customer signs a 15 to 25 year loan with the lender. The installer pays a dealer fee of 12 to 25% of system price, which functions as a payment processing cost.

Pros: Installer paid in 3 to 7 days post-install. No collection risk. Easy customer sales pitch.

Pros: Installer paid in 3 to 7 days post-install. No collection risk. Easy customer sales pitch.

Cons: Dealer fees eat 12 to 25% of revenue. At 7.5% prime in 2026, dealer fees on 25-year loans increased to 15 to 25% according to PV Magazine USA’s Q1 2025 dealer fee survey. The fee scales with rate, so a higher Fed Funds rate directly cuts installer margin. Also see: Us Residential Solar Market Trends 2026. For United States-specific compliance details, see United States arizona/phoenix. For United States-specific compliance details, see United States california/los-angeles.

Best for: Installers under $20 million revenue who need fast cash and cannot self-finance.

Customer Cash with Deposit Structure

A cash customer pays the full system price out of pocket. Installers who take cash deals should always require a deposit at contract signing.

A 30% deposit on a $20,000 cash system delivers $6,000 to cover panel and inverter procurement. The installer carries $7,000 (the remaining hard cost) for 60 to 90 days before final payment.

Pros: No dealer fees. Higher per-deal margin.

Cons: Longer cash cycle than financed deals. Collection risk on final payment. State laws cap residential deposits in some markets — California limits deposits to $1,000 or 10% of contract value, whichever is less, under the Solar Energy System Disclosure rules.

Best for: High-margin commercial deals or installers with strong working capital.

Milestone Billing (Commercial Projects)

Commercial customers pay in tranches tied to project milestones. A typical structure:

| Milestone | Payment | Days from Start |

|---|---|---|

| Contract signing | 30% | 0 |

| Material delivery | 30% | 60 |

| Substantial completion | 30% | 120 |

| PTO / commissioning | 10% | 180 |

Milestone billing aligns customer payments with installer outflows. The 30% deposit covers material procurement. The completion payment covers labor.

Pros: Reduces working capital need. Spreads collection risk across the project.

Cons: Each milestone is a separate invoice, often with separate retainage. Commercial customers contest milestones to delay payment. The 10% final retainage frequently sits in dispute for 90+ days.

Best for: Commercial and C&I installers above $5 million revenue.

Invoice Factoring

A factoring company advances 70 to 90% of an invoice within 24 to 48 hours. The factor collects from the customer directly and remits the remainder minus fees.

Typical fees: 2 to 5% per month of the invoice amount. For solar receivables with 60-day terms, this annualizes to 12 to 30% effective cost.

Pros: Immediate cash. No new debt on the balance sheet (when structured as true sale).

Cons: Expensive. Customer sees factor on the bill, which can damage the relationship. Factor takes credit risk seriously and may reject high-risk customers.

Best for: Short-term emergencies, not long-term funding.

Customer Payment Structure: The Single Biggest Lever

Most installers underprice the cash flow value of strong payment terms. A contract that requires 30% at signing, 60% at install, and 10% at PTO is dramatically better than a contract that says “due upon completion” — even if the headline price is identical.

Residential Best-Practice Payment Structure

| Stage | Cash Customer | Financed Customer |

|---|---|---|

| Contract signing | 10-30% deposit (per state law) | 0% (lender funds) |

| Material delivery | 0% | 0% |

| Install complete | 60-80% | Lender pays 70-95% |

| PTO | 10-20% balance | Lender pays remaining 5-30% |

For cash deals, the install-complete payment is critical. Do not wait for PTO. PTO can take 30 to 60 days post-install and is outside the installer’s control. Bill 80% at install with a clear contract clause that final 10-20% is due at PTO or 30 days post-install, whichever comes first.

Commercial Payment Structure

Commercial customers expect milestone billing. Negotiate explicitly:

- 30% mobilization fee at NTP (Notice To Proceed)

- 30% upon delivery of major equipment to site

- 30% at mechanical completion (system installed but not commissioned)

- 10% at substantial completion (PTO + 30 days for punch list)

The 30% mobilization fee is critical. It funds engineering, permitting, and initial material orders. Without it, the installer carries hundreds of thousands in expense before any cash arrives.

Pro Tip

Build retainage limits into every commercial contract. Cap the customer’s right to withhold final payment at 5% of contract value, not 10%, and require dispute resolution within 30 days of substantial completion. This single clause has saved my installer clients millions in disputed receivables.

Working Capital Benchmarks by Installer Size

Working capital needs scale with project volume, not just revenue. A high-volume residential installer needs more working capital than a commercial installer with the same revenue because residential projects close faster.

| Annual Revenue | Project Volume | Minimum Working Capital | Credit Line Recommended |

|---|---|---|---|

| Under $1M | 1-3 systems/month | $50K-$100K | $50K |

| $1M-$5M | 5-20 systems/month | $250K-$750K | $250K |

| $5M-$20M | 20-80 systems/month | $750K-$2.5M | $1M |

| $20M-$100M | 80-400 systems/month | $2.5M-$10M | $5M |

| Above $100M | 400+ systems/month | $10M+ | $25M+ |

The credit line column matters more than the cash column. Most growing installers do not have $2 million sitting in cash. They have $500,000 in cash and a $1 million credit line. The credit line covers seasonal swings and growth spurts. Without it, a single delayed quarter can trigger insolvency.

How to Build a Banking Relationship Early

Solar installers struggle to get credit lines because banks see the industry as volatile. The path to a strong credit facility:

- Open business accounts at a regional bank, not a national bank. Regional banks have relationship lending models. National banks scorecard everything.

- Build 12 months of clean financial statements before applying. Banks want to see consistent revenue, positive cash flow, and clear separation between owner and business funds.

- Provide three years of personal tax returns from all owners. Banks treat solar installers as personal-guarantee businesses regardless of LLC status.

- Maintain a debt service coverage ratio (DSCR) above 1.25. This means net operating income covers debt payments by 25% or more.

- Use a CPA who specializes in solar. Standard accountants miss inventory accounting, percentage-of-completion revenue recognition, and federal tax credit timing. These mistakes spook lenders.

A typical installer with $5 million revenue can secure a $750,000 to $1.5 million credit line after 24 months of consistent operations. Below 24 months, expect to use SBA-backed loans or alternative lenders like Sage or Pipe.

Tax and Incentive Timing: The Trap That Catches Installers

The federal Investment Tax Credit (ITC) and state incentives create cash flow traps that catch even experienced installers off-guard. Two specific issues recur:

The Section 25D Reality for Homeowners in 2026

The residential 30% ITC under Section 25D expired December 31, 2025. Homeowners installing systems in 2026 do not receive the 30% federal tax credit. This dramatically changes the installer cash conversation.

Before 2026: Installer markets the tax credit as part of the total system value. Customer self-funds the credit portion through tax savings. Cash flow neutral for installer.

After 2025: No federal tax credit for homeowners. Installers must drop sticker price or move customers to financed deals where the system is owned by a third party (TPO) that can claim Section 48 ITC.

The TPO transition matters for cash flow because it shifts the receivable from homeowner to third-party financier. TPO providers like Sunrun and Sunnova pay installers within 30 days of install, which is much faster than chasing homeowner payments post-PTO.

Section 48 ITC for Commercial Solar

Commercial solar projects still qualify for the 30% Section 48 ITC through 2032 under the Inflation Reduction Act. But the credit timing creates working capital pressure: the customer files for the credit on their next tax return, which can be 12 to 18 months after the system is installed.

Some commercial customers structure their payment to the installer based on after-credit cost. This means the installer carries the 30% credit value as a receivable until the customer’s tax filing cycle completes. For a $1 million commercial project, this is a $300,000 working capital drag.

The fix: Always price commercial deals before the ITC, not after. Force the customer to fund the full pre-credit amount through milestone payments. They monetize the credit on their own balance sheet.

State Incentive Timing

State incentives create separate cash traps:

- California SGIP (battery storage): Reservation request, install, then incentive payout. 90 to 180 days post-install.

- New York NY-Sun: Block-based incentive paid to installer on behalf of customer. 60 to 90 days post-install.

- Massachusetts SMART: 10-year monthly incentive stream to system owner. Zero upfront cash to installer.

Installers who roll state incentives into their installed price assume the receivable risk for collection. This is a hidden working capital drag that few installers model correctly.

What Most Solar Installers Get Wrong About Cash Flow

After working with hundreds of solar installers, the same five mistakes appear repeatedly.

Mistake 1: Confusing Revenue Growth with Cash Growth

A growing installer needs MORE working capital, not less. Each new project requires upfront material and labor outlay before customer payment lands. Doubling project volume doubles the working capital requirement at minimum.

I have watched installers raise $5 million in revenue from $2 million the prior year and run out of cash by month four. The growth itself consumed all available working capital. Net income looked great. The bank account did not.

Mistake 2: Treating Dealer Fees as a “Marketing Cost”

Dealer fees are 12 to 25% of revenue. That is not marketing. That is a structural margin cut. Installers who do not model dealer fees in their gross margin calculations think they are running at 30% gross margin when they are actually running at 8 to 15%.

Track dealer fees as a contra-revenue item, not a marketing expense. Net revenue (after dealer fees) is what funds operations.

Mistake 3: Letting AR Age Without a Collection Process

The day a customer payment is one day late, the installer should have a standard collection process. Most installers wait 30, 60, or 90 days before calling the customer. By then, the customer has moved cash to other priorities.

A simple 5-day, 15-day, 30-day, 45-day escalation cadence collects 80% of slow receivables. Day 5: friendly email. Day 15: phone call. Day 30: certified letter. Day 45: lien filing.

Mistake 4: Underestimating Inspection Delays

The installer does not control inspection schedules. AHJs can take 2 to 8 weeks for final inspection in busy markets. Utility PTO can take another 2 to 6 weeks. The installer who plans on 30-day post-install collection often waits 90+ days.

Build inspection lag into every cash flow forecast. Assume 60 days post-install for residential PTO and 120 days for commercial.

Mistake 5: Mixing Personal and Business Cash

Owner-operators frequently dip into personal cash to cover business shortfalls, then dip into business cash for personal expenses. This breaks corporate veil protection and confuses banks during credit review.

Keep separate accounts. Pay yourself a clear salary. Track every owner draw separately. The discipline pays off when applying for credit and tax filings.

What Most Guides Miss

Generic cash flow advice tells you to “collect faster, pay slower.” For solar installers, this is wrong. Collecting faster is mostly outside your control (PTO timing). Paying slower damages supplier relationships that are critical in a supply-constrained market. The real lever is structuring contracts so customer cash and supplier cash align — not generic working capital optimization.

The Commercial Cash Flow Stack: Tools and Software

Most installers manage cash flow in QuickBooks plus spreadsheets. That works up to about $5 million revenue. Above that, dedicated tools become necessary.

Accounting Software

| Tool | Best For | Monthly Cost |

|---|---|---|

| QuickBooks Online | Installers under $5M | $90-$200 |

| Sage Intacct | Installers $5M-$50M | $500-$2,000 |

| NetSuite | Installers above $50M | $2,000-$10,000 |

Solar-specific accounting requires job costing, percentage-of-completion revenue, and inventory tracking. Generic QuickBooks setups miss two of these three. Use a solar-specialized CPA to configure the chart of accounts correctly. See Solar Racking Design Guide for detailed guidance.

Cash Flow Forecasting

Cash flow forecasting tools beyond accounting include:

- Float — 13-week rolling cash forecast, $89/month

- Pulse — Solar-friendly cash flow tool, $59/month

- Spotlight Reporting — Project-level cash analysis, $159/month

A 13-week rolling forecast is the minimum for any installer above $2 million revenue. Update it weekly. Compare actual to forecast. The variance pattern teaches you about your business faster than any other metric.

Project Cash Tracking

Solar-specific project management tools that track cash:

- Scoop Solar — Field operations + cash milestones

- HelioQuote — Sales + payment tracking

- OpenSolar — Free design + basic project tracking

- Sighten — Enterprise pricing, full PMO

Pair the generation and financial tool inside solar design software with these project tools to model cash impact at the sales stage, not just post-sale.

A 90-Day Cash Flow Recovery Plan

If your installer business is cash-stressed right now, here is a 90-day recovery plan that has worked for my CFO clients.

Days 1-7: Stop the Bleeding

- Freeze new spending. No equipment purchases, no software signups, no hires.

- Pull AR aging report. Every receivable over 30 days gets a call within 48 hours.

- Pull AP aging report. Negotiate 30-day extensions with top 5 suppliers.

- Cut owner draws to minimum. Pay yourself what the business can sustain, not what you want.

- Review every recurring subscription. Cancel anything not directly producing revenue.

Days 8-30: Restructure Operations

- Renegotiate customer contracts. Move cash deals to financed where possible.

- Add deposit requirements to every new contract — 10% minimum residential, 30% commercial.

- Tighten credit terms. Net 30 max, no exceptions. Lien filing standard at day 45.

- Audit dealer fee partners. Switch high-fee partners (over 18%) to lower-fee competitors.

- Establish 13-week cash forecast. Update weekly. Share with owners every Friday.

Days 31-60: Build the Cushion

- Apply for credit line increase at your primary bank. Show 60 days of improved metrics.

- Renegotiate supplier terms. Push net 30 to net 45 with your top 3 distributors.

- Slow growth. Pause hiring and marketing spend until working capital is rebuilt.

- Quote 5-10% higher on new deals to rebuild margins.

- Sell or factor old receivables over 90 days.

Days 61-90: Lock In Improvements

- Hire fractional CFO if you do not have one. Cost: $3,000-$8,000/month.

- Implement project-level P&L tracking. Every job has a margin number.

- Set working capital target (90 days of operating expense). Build to it.

- Document cash policies. Deposit requirements, collection cadence, dealer fee thresholds.

- Build banking relationships even when you do not need money. The time to borrow is before you need to.

Model Project-Level Cash Flow Before You Sell

Use the SurgePV generation and financial tool to model project ROI for customers AND project cash flow for your own business — at the same time.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

For a direct comparison, see Arka 360 vs SurgePV.

Real-World Example: How a 30-Crew Installer Turned Cash Flow Around

A residential installer in Texas with 30 crews and $18 million annual revenue was burning $200,000 a month in working capital growth in 2024. The owner had drawn $400,000 from personal savings to cover payroll over six months.

The diagnostic revealed three issues:

- 65% of deals were cash, with average customer payment landing 87 days post-install

- Dealer fee partnerships averaged 21% (high end of market)

- Material credit was net 30, but supplier disputes caused 40% to be paid in 15 days

The 90-day fix:

- Required 20% deposit on all cash deals (state law allowed up to 20% in Texas)

- Switched dealer fee partner from a 21% provider to a 15% provider

- Negotiated net 45 terms with two largest distributors

- Implemented 5-day collection cadence on every receivable

Six months later:

- DSO dropped from 87 days to 41 days

- Effective dealer fee rate dropped from 21% to 15%

- Working capital requirement dropped from $4 million to $2.4 million

- The owner repaid the personal loan within 8 months

The improvement came from contract structure and dealer fee selection. No new financing required.

Frequently Asked Questions

What is the typical cash flow cycle for solar installers?

Residential solar installers face a 60 to 90 day cash flow cycle. Material is paid for at order. Labor is paid weekly. Final customer payment lands after PTO (Permission To Operate), which can take 30 to 60 days post-install. The cash gap between payable and receivable is where most installers fail.

How much working capital does a solar installer need?

A solar installer needs at least 90 days of operating expenses in working capital. For a company installing 10 systems per month at an average system cost of $20,000, that means $300,000 to $450,000 in available cash or credit. Below this threshold, one delayed PTO can trigger a payroll crisis.

What is the difference between dealer fees and milestone financing?

Dealer fees come from third-party financiers like Mosaic or GoodLeap. They pay the installer 70 to 95% of the system price at install, taking a 12 to 25% dealer fee. Milestone financing pays installers in stages: at contract signing, panel install, and PTO. Dealer fees cost more but settle cash quickly.

How do solar installers manage 90-day payment cycles?

Successful installers use three tactics: third-party loan partners that pay at install, customer deposits of 10 to 30% at contract signing, and progress billing for commercial projects. Combining these reduces the typical 90-day cycle to 15 to 30 days for most projects.

What is the biggest cash flow mistake solar installers make?

The biggest mistake is selling cash deals on net 60 payment terms while paying suppliers net 30. This creates a 30 to 90 day cash gap on every project. Installers should require 30% deposit on cash deals or push every cash customer to financed terms with dealer payouts.

What financial KPIs should solar installers track for cash flow?

Track Days Sales Outstanding (DSO), Days Payable Outstanding (DPO), and the cash conversion cycle (DSO minus DPO). A healthy solar installer keeps DSO under 45 days, DPO at 30 to 45 days, and a cash conversion cycle under 30 days. Anything higher signals a cash crisis ahead.

Can solar installers use invoice factoring?

Yes, but the cost is high. Factoring companies advance 70 to 90% of invoice value, taking 2 to 5% per month in fees. For solar installers with 60-day customer payment terms, factoring effectively costs 12 to 30% annualized. Use it only for short-term emergencies, not as a long-term funding source.

How do interest rates affect solar installer cash flow?

Higher interest rates raise both customer financing costs and installer working capital costs. At 7.5% prime in 2026, dealer fees on solar loans increased to 15 to 25% according to PV Magazine USA’s 2025 dealer fee survey. Lower take rates and longer sales cycles compound the cash flow pressure.

Three Steps to Take This Week

-

Pull your AR aging and AP aging side by side. If average AR days exceed average AP days, you have a structural cash problem. Fix the contract terms before fixing anything else.

-

Calculate your cash conversion cycle. Use the formula: DSO + DIO − DPO. If the number exceeds 60 days, you need more working capital than you have. Either raise capital, restructure terms, or slow growth.

-

Model your next 13 weeks of cash flow on a Friday afternoon. Show every project, every supplier payment, every payroll, every tax obligation. The first time you do this, you will find a week where cash goes negative. That is the week you must fix before it arrives. Run scenarios in solar design software to test pricing changes before they hit your books.

Related SurgePV Resources

Continue learning with these related guides for solar installers and EPCs:

- Project Profitability Tracking

- Solar Company Overhead Reduction

- Solar Business Succession Planning

- Solar Material Procurement Strategy

- Solar Installer Insurance Requirements

For more solar business and marketing content, explore the full SurgePV blog or browse the SurgePV glossary for definitions of solar industry terms.

Solar Software Tools to Support This Work

Effective solar installer operations depend on integrated software. SurgePV’s solar design platform helps installers handle the upstream work that feeds every decision in this guide:

- Solar design software for system layouts, panel placement, and BOM generation

- Shadow analysis for site-specific irradiance and obstruction modeling

- Generation and financial tool for production forecasts and project ROI

- Solar proposal software for branded, customer-facing proposals

- Clara AI for automated design assistance and Q&A

Browse the full SurgePV platform to see how installers across 50+ countries use the tools to design smarter, sell faster, and streamline every solar project.