Quick Answer

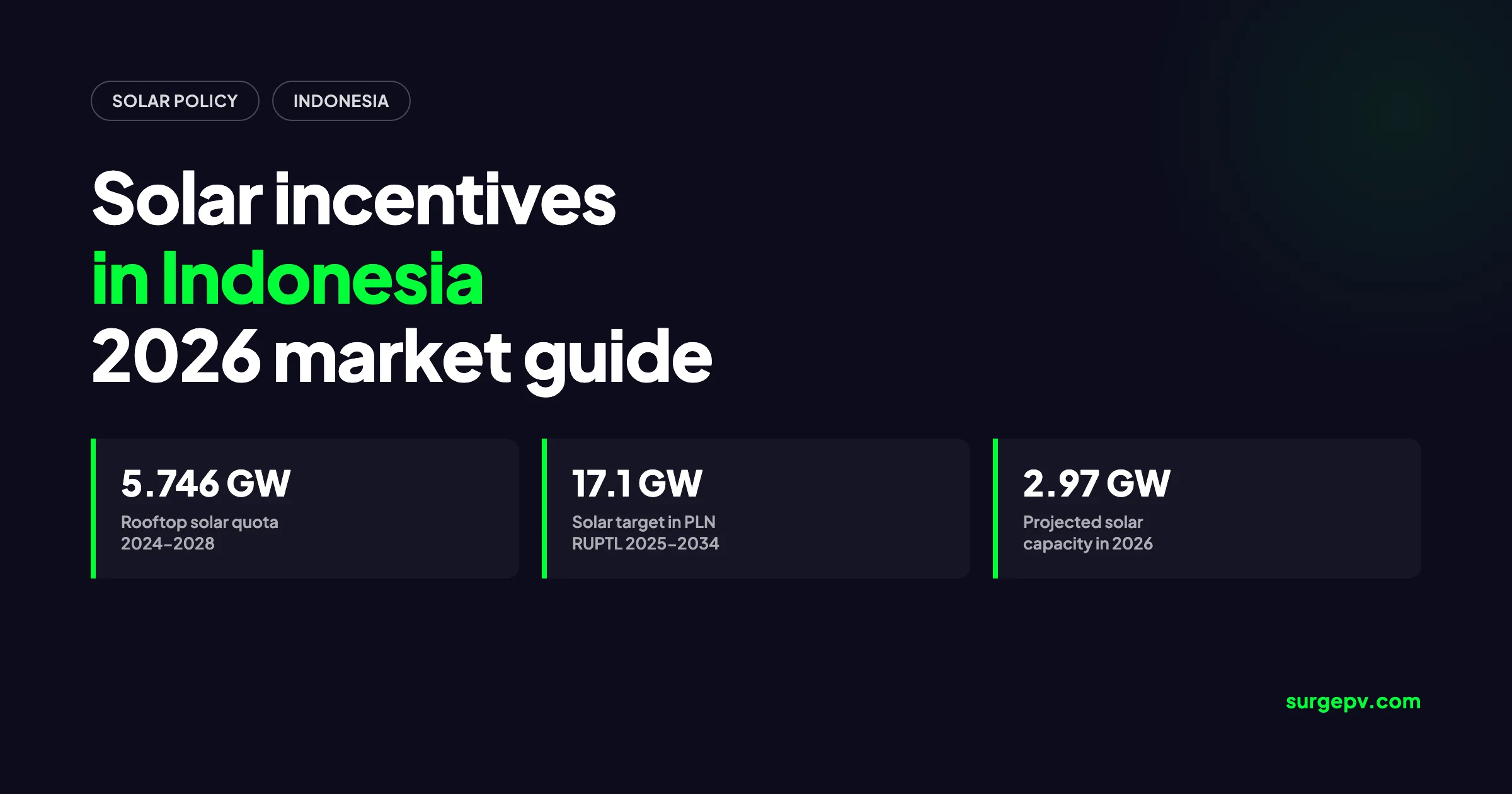

Indonesia's 2026 solar incentives are a policy stack rather than a direct subsidy: a 5.746 GW rooftop quota under MEMR Regulation 2/2024, the 17.1 GW solar target in PLN's RUPTL 2025-2034, tax holidays and import duty relief for qualifying projects, TKDN local-content rules, and JETP-backed financing. Net metering for new rooftop systems has ended, so projects must be sized for self-consumption.

Indonesia’s solar market is entering a new phase in 2026. The country is projected to grow from 2.15 GW of solar capacity in 2025 to 2.97 GW in 2026, according to Research and Markets (2026). The same forecast sees capacity reaching 14.91 GW by 2031. For installers, EPCs, and investors, the message is clear: Indonesia is scaling, but the rules have changed.

This guide is a market-focused incentive manual for 2026. It covers the regulatory framework, the real incentives that reduce project cost, how PLN now treats rooftop solar, and the mistakes that waste money. For the broader Southeast Asian picture, see our global solar market forecast for 2026. For payback comparisons across markets, see solar payback period by country.

If you are designing systems or writing proposals for Indonesian clients, use a solar design platform that models PLN tariffs, self-consumption ratios, and quota constraints. The right tool can cut hours from every project. Model payback automatically, then generate solar proposals in minutes. Check pricing or book a demo to see how SurgePV handles Indonesia.

Quick Answer

Indonesia’s 2026 solar incentives are a policy stack rather than a direct subsidy: a 5.746 GW rooftop quota under MEMR Regulation 2/2024, the 17.1 GW solar target in PLN’s RUPTL 2025-2034, tax holidays and import duty relief for qualifying projects, TKDN local-content rules, and JETP-backed financing. Net metering for new rooftop systems has ended, so projects must be sized for self-consumption.

In this guide:

- Latest 2026 status of every active Indonesian solar incentive

- Why MEMR Regulation 2/2024 ended net metering and what replaced it

- How the PLN rooftop solar quota works and where capacity is allocated

- Tax incentives, import relief, and TKDN local-content rules

- RUPTL 2025-2034 and the 17.1 GW solar target

- Corporate PPA and floating solar opportunities

- Regional differences: Java, Sumatra, Kalimantan, and beyond

- Common mistakes and how to avoid them

Latest Updates: Indonesia Solar Incentives 2026

The Indonesian solar policy environment shifted in 2024 and 2025. MEMR Regulation 2/2024 restructured rooftop solar, PLN published its 2025-2034 RUPTL, and module prices fell sharply enough to push solar below grid parity in high-irradiance provinces.

Indonesia Solar Incentive Status — June 2026

| Incentive | Type | Status | Key Terms |

|---|---|---|---|

| Rooftop solar quota | Capacity allocation | Active | 5.746 GW total for 2024-2028; 1,065 MW in 2026 |

| Net metering | Bill credit | Ended for new systems | Grandfathered for approved existing systems |

| Tax holiday | Corporate tax exemption | Active | 5-10 years for investments above IDR 156 billion |

| Import duty exemption | Customs relief | Active | For equipment not produced domestically |

| Accelerated depreciation | Tax accounting | Active | 8-year schedule vs standard 20 years |

| TKDN local content | Local-content requirement | Active | 40% ground-mounted, 60% rooftop typical |

| RUPTL solar target | Planning target | Active | 17.1 GW solar additions, 2025-2034 |

| JETP financing | International support | Active | USD 20 billion public and private commitment |

| Corporate RE-PPA | Contract route | Growing | Direct renewable energy PPAs authorized |

| Floating solar | Technology pathway | Emerging | Up to 20% of surface water areas under study |

Key Changes Since 2025

January 2024 — MEMR Regulation 2/2024: The Ministry of Energy and Mineral Resources replaced MEMR Regulation 26/2021 with a new rooftop solar framework. It abolished net metering and removed the 100% of connected-capacity cap. It also introduced a five-year quota, limited applications to January and July, and added deemed approval after 30 business days. Read the full analysis from ABNR Counsellors at Law (2024).

May 2025 — RUPTL 2025-2034 launched: PLN’s ten-year plan targets 69.5 GW of new capacity, with 42.6 GW from renewables and 10.3 GW from storage. Solar leads at 17.1 GW. Total investment is estimated at IDR 2,967 trillion, with roughly 73% from private developers and IPPs, according to Mondaq (2025).

January 2026 — Proposed 400 MW rooftop quota boost: The Ministry of Energy and Mineral Resources proposed adding 400 MW to the 2026 rooftop allocation. If PLN endorses the plan, the annual quota would rise to around 1.4 GW, as reported by Solar Quarter (2026).

Key Takeaway

2026 is the first full year of the post-net-metering era. The most reliable value comes from self-consumption, tax holidays, and corporate PPAs. Quota availability is now the gatekeeper for new rooftop projects.

Why Indonesia’s Solar Market Matters in 2026

Indonesia is the largest economy in Southeast Asia and one of the most solar-rich countries on earth. The technical potential is enormous, but deployment has lagged behind Vietnam, Thailand, and the Philippines. That is now changing.

Market Size and Targets

Cumulative solar capacity is expected to reach 2.97 GW in 2026, up from 2.15 GW in 2025. The forecast comes from Research and Markets (2026). The same source expects 14.91 GW by 2031. Module average selling prices fell nearly 50% during 2024, shipping costs normalized, and EPC bids routinely met PLN’s ceiling tariff of IDR 1,200 per kWh. Some bids reportedly went as low as IDR 1,050 per kWh.

The RUPTL target of 17.1 GW of solar additions between 2025 and 2034 makes solar the largest renewable technology in the plan. That is more than hydro at 11.7 GW and wind at 7.2 GW, according to Lexology (2025).

Resource Quality

Indonesia’s solar technical potential is estimated at 207 GW to 3,600 GW depending on the study. The best resources are in eastern Indonesia, parts of Sumatra, and southern Java. Capacity factors for fixed-tilt PV typically range from 14% to 18% nationally, with some sites exceeding 20%. That is lower than the Middle East or northern Chile. Combined with high PLN tariffs and falling module costs, it is still enough to make solar competitive.

The JETP Factor

Indonesia’s Just Energy Transition Partnership mobilizes USD 20 billion in public and private financing to accelerate power-sector decarbonization. JETP supports grid investment, early coal retirement studies, and renewable project development. It does not replace PLN procurement, but it lowers the cost of capital and improves bankability for large solar and storage projects.

For solar professionals, the practical opportunity is to show both generation and bill avoidance at the customer’s actual tariff tier. That requires hourly load modeling and accurate shading analysis, both of which are built into modern solar design software.

MEMR Regulation 2/2024: The End of Net Metering

MEMR Regulation 2/2024 is the most important policy change for Indonesian rooftop solar. It replaced the previous net-metering framework with a quota-based, self-consumption-driven model.

What Changed

| Aspect | Before (MEMR 26/2021) | Now (MEMR 2/2024) |

|---|---|---|

| Export credit | Exported kWh offset imported kWh | No credit; export is uncompensated |

| Capacity limit | Up to 100% of connected capacity | No fixed cap; limited by quota |

| Metering | Export-import kWh meter paid by customer | Advanced meter paid by IUPTLU holder |

| Industrial capacity charge | Applied monthly | Abolished for new systems |

| Application timing | No fixed window | January and July only |

| Approval timeline | 5 business days | 30 business days with deemed approval |

The Quota Mechanism

IUPTLU holders, primarily PLN, must submit five-year rooftop solar quotas to the Director General of Electricity. PLN’s first quota covers 2024-2028 and totals 5,746 MW. The annual breakdown is 901 MW in 2024, 1,004 MW in 2025, 1,065 MW in 2026, 1,183 MW in 2027, and 1,593 MW in 2028. These figures come from Ashurst (2024).

2026 Quota by Region

| Region | 2026 Quota (MW) |

|---|---|

| Java-Madura-Bali | 910.0 |

| Sumatra | 60.0 |

| South, Southeast, and East Kalimantan | 58.7 |

| West Kalimantan | 16.4 |

| Southern Sulawesi region | 12.0 |

| North Kalimantan | 1.9 |

| West Nusa Tenggara | 1.5 |

| Maluku and North Maluku | 1.2 |

| Papua and West Papua | 1.3 |

| East Nusa Tenggara | 0.9 |

| North Sulawesi and Gorontalo | 0.6 |

| Total | 1,065 |

Application and Allocation

Prospective customers apply through the PLN Mobile app during January and July windows. Quotas are allocated on a first-come-first-served basis. If a cluster’s quota is exhausted, the customer is placed on a waiting list for the next period. After approval, the system must reach commercial operation within six months or the quota is revoked.

Tax, Customs, and Fiscal Incentives

Indonesia does not offer a direct upfront rebate for residential solar buyers. The real value lies in corporate tax holidays, customs relief, and accelerated depreciation.

Tax Holidays

Renewable energy projects with investment above IDR 156 billion can qualify for a corporate income tax holiday of 5 to 10 years. The exact duration depends on location and project type, with frontier regions typically receiving longer holidays. This is one of the strongest incentives for utility-scale and large C&I developers.

Import Duty Exemptions

Equipment that is not produced domestically can qualify for import duty exemption. Solar modules, inverters, and tracking systems often fall into this category because domestic manufacturing capacity remains limited. Combined with falling module prices, this materially lowers landed costs.

Accelerated Depreciation

Solar assets can be depreciated over eight years instead of the standard 20-year schedule. For a project in the 22% corporate tax bracket, this front-loads tax shields and improves early-year cash flow.

Local Incentives and Mandates

Jakarta Governor Regulation 38/2024 obliges new commercial buildings larger than 500 square meters to install rooftop solar. Similar mandates are being mirrored in West Java and Bali. These are not subsidies in the traditional sense, but they create guaranteed demand and can include permitting fast-tracks.

TKDN Local-Content Rules

TKDN, or Tingkat Komponen Dalam Negeri, measures the share of local value in a project. It is a requirement, not an incentive, but compliance unlocks access to PLN tenders and government procurement.

Typical Thresholds

- Ground-mounted solar power plants: minimum 40% TKDN

- Rooftop solar projects: minimum 60% TKDN

These thresholds can vary by tender and may rise over time as domestic manufacturing grows. Projects that exceed the minimum can receive price preferences in competitive bidding.

Practical Impact

Indonesia’s solar manufacturing base is still developing. Module prices for locally produced panels can be 27% to 88% higher than imported equivalents. This is based on research cited by Halimatussadiah et al. (2023). That means TKDN compliance can raise project costs unless the developer structures labor, assembly, logistics, and supporting services to count toward local content.

For EPCs, the message is to confirm TKDN treatment before procurement. Do not assume that using a local installer alone satisfies the threshold.

RUPTL 2025-2034 and the 17.1 GW Solar Target

PLN’s RUPTL is the master plan for Indonesian power development. The 2025-2034 edition is the most renewable-heavy version to date.

Capacity Targets

| Technology | 2025-2034 Target (GW) |

|---|---|

| Solar | 17.1 |

| Hydro | 11.7 |

| Wind | 7.2 |

| Geothermal | 5.2 |

| Bioenergy | 0.9 |

| Nuclear | 0.5 |

| Battery storage | 4.3 |

| Pumped-storage hydro | 6.0 |

| Gas | 10.3 |

| Coal | 6.3 |

The plan calls for 69.5 GW of new capacity by 2034, of which 42.6 GW is renewable energy and 10.3 GW is storage. Total investment is estimated at IDR 2,967 trillion, roughly USD 182 billion.

Implementation Reality

PLN has historically underperformed against renewable targets. In the first half of 2025, only 1.6 GW of capacity reached commercial operation. The planned volume from the previous RUPTL was 10 GW. This gap is noted by IESR (2025). Developers should treat RUPTL targets as directional demand signals, not guaranteed procurement volumes.

Corporate PPAs, Floating Solar, and C&I Routes

Large energy buyers in Indonesia are bypassing the quota and tariff framework. They use direct contracts and alternative procurement routes instead.

Corporate Renewable PPAs

Direct power purchase agreements between renewable generators and large buyers are authorized under recent regulations. These contracts are especially popular with RE100 manufacturers in Java and Batam that need Scope 2 emissions reductions and long-term price certainty. A corporate PPA does not rely on net metering or PLN’s retail tariff, so it suits buyers with large, stable daytime loads.

Floating Solar

RUPTL 2025-2034 identifies floating solar as a way to reduce land-use constraints. The plan contemplates using up to 20% of surface water areas for floating PV, subject to government approval. Reservoirs attached to hydroelectric dams are the most promising early sites because they already have grid infrastructure.

Utility-Scale Auctions

Large utility-scale projects typically sell to PLN through competitive auctions or bilateral negotiations. Ceiling tariffs have fallen to IDR 1,200 per kWh and below, making solar competitive with new coal and gas in high-irradiance areas.

For C&I installers, the design priorities differ from residential work. Load profiling, demand-charge analysis, and shadow analysis matter more than simple bill offset.

Regional Differences

Indonesia is an archipelago of more than 17,000 islands, so solar economics vary sharply by region.

Java-Madura-Bali

Java holds the largest load centers, the best grid infrastructure, and the largest quota allocation. Industrial demand from Jakarta, Surabaya, and Batam drives most corporate PPA activity. Retail tariffs are high enough to make rooftop solar attractive for factories, malls, and data centers.

Sumatra

Sumatra has strong solar resources and growing industrial demand, particularly around Medan and the Riau Islands. The 2026 quota is only 60 MW, so competition for capacity can be tight.

Kalimantan

East and South Kalimantan are emerging as solar and battery manufacturing hubs due to nickel processing investments. Grid infrastructure is weaker than Java, but demand growth is rapid. The Nusantara capital city project in East Kalimantan is also expected to drive clean-energy procurement.

Eastern Indonesia

Regions such as Papua, Maluku, and Nusa Tenggara have the best solar resources but the weakest grids. Many projects here are off-grid or hybrid solar-plus-diesel systems rather than grid-tied rooftop installations.

Common Mistakes and Misconceptions

Even experienced developers lose money in Indonesia by misunderstanding how the new framework works.

Designing for Export

The single most expensive mistake is sizing a rooftop system to maximize generation rather than self-consumption. Under MEMR 2/2024, exported energy is not credited. A kilowatt consumed on site is worth the full retail tariff; a kilowatt exported is worth zero.

Ignoring the Quota Window

Applications open only in January and July. Missing a window can delay a project by months, especially in clusters where quota is exhausted quickly. Check PLN Mobile regularly and prepare documents in advance.

Underestimating TKDN

Ordering imported modules and inverters without a TKDN plan can disqualify a project from tenders or delay COD certification. Map local content early and get certification from the Ministry of Industry.

Overlooking Grid Reliability

Some regions have weak grids with limited absorption capacity. A project that is technically permitted may still face curtailment or interconnection delays. Always review the local grid study before finalizing design.

Assuming National Tariffs Apply Everywhere

PLN tariffs vary by customer class and region. Model the customer’s actual tariff, not a Jakarta average. The same 500 kW system can have very different payback in Batam versus Papua.

Conclusion

Indonesia’s solar incentive framework in 2026 is a stack built from rooftop quotas, RUPTL targets, tax holidays, import relief, and JETP financing. The biggest change is the end of net metering for new rooftop systems. That shifts the entire design philosophy from maximizing generation to maximizing self-consumption.

For solar professionals, the competitive edge is no longer just installation price. It is the ability to model the right system size for a customer’s daytime load, confirm quota availability, navigate TKDN rules, and present a bankable proposal. Tools like Clara AI and SurgePV’s generation and financial tool can automate that workflow for Indonesian projects.

Three actions to take now:

- Size for self-consumption first — exported rooftop energy is not compensated under MEMR 2/2024.

- Check quota before quoting — confirm available capacity in the customer’s PLN cluster during the January or July window.

- Map TKDN early — local-content compliance can make or break project economics and tender eligibility.

For regional comparisons, see our solar payback period by country guide. For installers scaling in Southeast Asia, our guide for solar installers covers proposal automation and compliance workflows.

Frequently Asked Questions

What solar incentives are available in Indonesia in 2026?

Indonesia’s 2026 solar incentives include the 5.746 GW rooftop solar quota under MEMR Regulation 2/2024, PLN’s 17.1 GW solar target in RUPTL 2025-2034, tax holidays of 5-10 years for qualifying investments, import duty exemptions for equipment not produced domestically, accelerated depreciation, TKDN local-content preferences, and JETP-backed financing. New rooftop systems no longer receive net metering, so incentives now reward self-consumption and corporate power purchase agreements.

Does Indonesia have net metering for rooftop solar in 2026?

No. MEMR Regulation 2/2024 abolished net metering for new rooftop solar systems connected to PLN or other IUPTLU holders. Exported energy is no longer credited against the customer’s electricity bill. Existing systems approved before the regulation may keep net metering for a transitional period, generally up to 10 years from approval. New projects must be sized for daytime self-consumption.

What is the PLN rooftop solar quota for 2026?

The national rooftop solar quota set under DGE Decree 279.K/TL.03/DJL.2/2024 allocates 1,065 MW for 2026 as part of a 5.746 GW total for 2024-2028. Java-Madura-Bali receives the largest share with 910 MW in 2026, followed by Sumatra with 60 MW and Kalimantan with 76.4 MW across its subsystems. The Ministry has also proposed an additional 400 MW boost for 2026, which would raise the total to roughly 1.4 GW if approved.

How do I apply for rooftop solar quota in Indonesia?

Applications are submitted through the PLN Mobile app during bi-annual windows in January and July. Customers must create an ID, enter the requested capacity, upload administrative and technical documents, and wait for PLN’s decision. PLN has 30 business days to evaluate; silence is treated as deemed approval. Once approved, the system must obtain its operational worthiness certificate within six months or the quota is revoked.

What are TKDN requirements for solar projects in Indonesia?

TKDN, or Tingkat Komponen Dalam Negeri, is Indonesia’s local-content requirement. Solar projects typically need at least 40% domestic content for ground-mounted plants and 60% for rooftop systems. Government and PLN-linked tenders may impose higher thresholds or give price preferences to bidders that exceed them. Imported modules, inverters, and tracking systems may qualify for exemptions when no competitive domestic alternative exists.

What tax incentives exist for solar projects in Indonesia?

Qualifying renewable energy investments can receive a 5-10 year corporate income tax holiday for projects above IDR 156 billion, import duty exemptions for equipment not produced domestically, and accelerated depreciation over eight years instead of the standard 20-year schedule. These incentives are administered through the Ministry of Finance and Indonesia’s investment authority, BKPM.

What is RUPTL 2025-2034 and what does it mean for solar?

RUPTL is PLN’s ten-year electricity supply business plan. The 2025-2034 edition targets 69.5 GW of new capacity, of which 42.6 GW is renewable energy and 10.3 GW is storage. Solar leads the renewable mix with 17.1 GW, followed by hydro, wind, and geothermal. The plan signals strong policy demand for utility-scale, rooftop, and floating solar, although execution and grid investment remain major hurdles.

Can residential customers still benefit from rooftop solar after MEMR 2/2024?

Yes, but the value proposition changed. Without net metering, residential savings come almost entirely from offsetting daytime PLN consumption. Homes with high daytime loads, such as air conditioning or electric water heating, still see meaningful savings. Households with mostly night-time consumption will find payback longer unless they add batteries, which raises the upfront cost.

What are the main mistakes when sizing solar systems in Indonesia?

The most common mistake is oversizing for export. Because MEMR 2/2024 ended net metering, surplus energy sent to PLN is not compensated. Systems should be sized to match daytime self-consumption. Other mistakes include ignoring the bi-annual quota window, underestimating TKDN compliance timelines, using non-SNI-compliant mounting, and applying for capacity without confirming local grid quota availability.

What is the typical solar payback period in Indonesia?

Well-designed commercial and industrial rooftop systems in Indonesia typically pay back in 6 to 10 years, depending on the local PLN tariff, self-consumption ratio, irradiance, and TKDN compliance costs. Systems in Java and Batam with high daytime loads and strong corporate PPA structures can pay back faster, while residential projects with low daytime usage may take longer.