Quick Answer

Kenya's solar regulations require EPRA licensing for systems over 1 MW, KPLC net metering approval for grid-connected systems, and NEMA environmental assessments for commercial projects. Rural electrification grants cover 30–50% of costs.

Most articles on Kenya solar regulations open with a celebration of geothermal leadership and 90% renewable grid share. That framing is fine for tourism brochures. It is misleading for anyone trying to actually build a system in 2026. Kenya’s solar sector is shaped less by its clean grid and more by three regulatory choices that almost nobody outside the industry understands.

Kenya’s solar regulations require EPRA licensing for systems over 1 MW, KPLC net metering approval for grid-connected systems, and NEMA environmental assessments for commercial projects. Rural electrification grants cover 30–50% of costs. Read Design Commercial Solar System 1MW for a complete walkthrough.

The first choice is the 1 MW cap on net metering. The second is the 15-kilometre buffer rule that keeps private mini-grids away from the KPLC backbone. The third is the credit-expiry clause that quietly resets every prosumer’s solar bank account each financial year. Together these three rules have produced the strangest renewable market in East Africa. Solar installs are exploding. Net metering uptake is crawling. And most large commercial systems still operate as private captive plants with no grid export at all. For Africa-specific compliance details, see Africa solar compliance.

This guide covers every regulation that touches solar in Kenya. We map EPRA, KPLC, KEBS, NEMA and the county governments. We explain the Energy (Net Metering) Regulations 2024, the draft Energy (Mini-Grid) Regulations, and the brand-new Open Access Regulations 2026. We size the commercial and industrial market with real installed capacity numbers. And we show the numbers that determine whether net metering, captive solar, or a direct PPA is the right answer for a Kenyan business in 2026.

Quick Answer

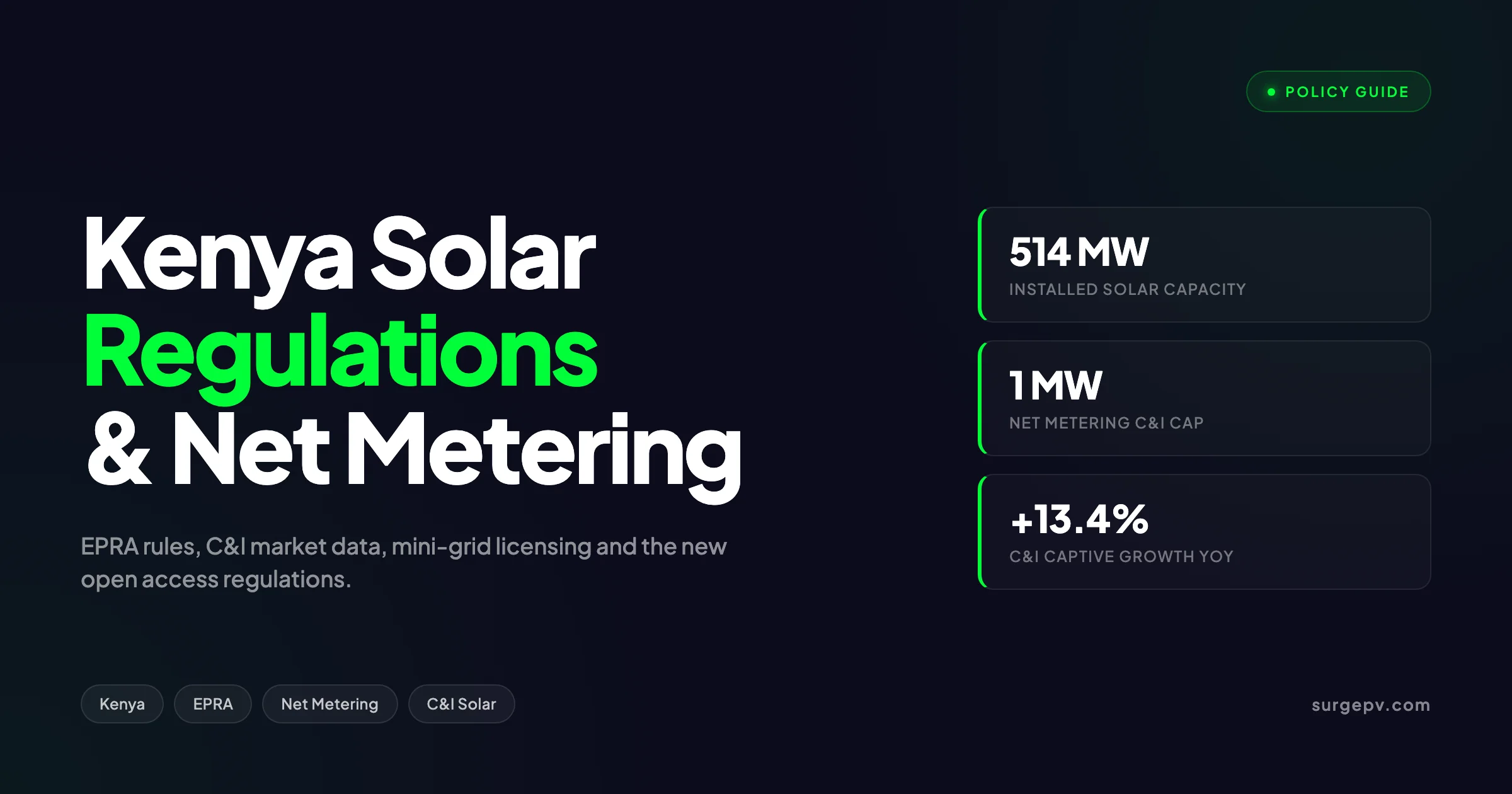

Kenya solar regulations are anchored by the Energy Act 2019 and enforced by the Energy and Petroleum Regulatory Authority (EPRA). The Energy (Net Metering) Regulations 2024 allow systems up to 1 MW to export surplus power to KPLC’s grid for bill credits at retail tariff. Installed solar reached 514.1 MW by June 2025, with C&I captive solar at 300.5 MW. New Open Access Regulations from May 2026 now let large consumers buy power directly from licensed solar generators.

TL;DR — Kenya Solar Regulations 2026

EPRA gazetted the Energy (Net Metering) Regulations in 2024 with a 1 MW cap, a 60-day approval window, and bill credits at retail tariff. Credits expire at year-end. The Open Access Regulations 2026 broke KPLC’s bulk supply monopoly in May 2026. C&I captive solar grew 13.4% year-on-year and now sits at 300.5 MW. Solar PV modules are duty-free and VAT-exempt, but the Finance Bill 2026 may reclassify batteries in ways that increase consumer prices.

In this guide:

- Kenya’s installed solar capacity and 2026 market snapshot

- The full regulatory stack: EPRA, KPLC, KEBS, NEMA and county roles

- Net metering rules: caps, bi-directional meters, 60-day approvals and credit limits

- The licensing path for installers, importers and large generators

- Mini-grid regulations and the 15-km buffer problem

- C&I market data with named projects from Two Rivers Mall, Mabati and others

- Open Access Regulations 2026 and the new PPA market

- Tax, import duty and VAT framework for solar

- Real ROI numbers and the math that drives 2026 decisions

Kenya Solar Market at a Glance: 2026 Snapshot

Kenya’s installed solar capacity hit 514.1 MW by June 2025, according to EPRA’s June 2025 report. That number splits into 210.3 MW of utility-scale projects, 300.5 MW of captive C&I plants and 3.9 MW of off-grid systems. Total installed energy capacity across all fuels sat at 3,840.8 MW.

The headline number underplays the shift inside the mix. Captive solar added 71.3 MW in the 12 months to June 2025. That is a 13.4% year-on-year jump in a market where total grid capacity actually dipped slightly. Roughly half of new captive capacity came from solar PV. The rest was diesel, biomass and hybrid.

Key Takeaway

Captive C&I solar is now the fastest-growing segment of Kenya’s power system. At 300.5 MW it already exceeds utility-scale solar capacity. This shift is driven by KES 22-25 per kWh commercial tariffs and the simple fact that Kenya Power’s bulk supply has not kept pace with industrial demand growth.

The country’s broader energy mix remains heavily renewable. Geothermal, hydro, wind and solar together produce more than 90% of grid electricity. Kenya’s stated target is 100% clean energy by 2035. Universal electricity access is targeted for 2030. Both goals depend on the regulatory choices we cover in the next sections.

For installers and developers, three market signals matter in 2026. Commercial tariffs are climbing. Captive solar adoption is widening. And the regulator has begun to crack open the long-protected wholesale market for the first time in 25 years. Each signal opens a different revenue path for solar businesses operating in Kenya.

The Regulatory Stack: Who Governs Kenya Solar in 2026

Solar in Kenya is not regulated by a single body. Six agencies own different parts of the compliance journey. Getting one wrong can void an installation, delay a permit, or block a grid connection. The table below maps each regulator to its scope.

| Agency | Acronym | Scope | What They Approve |

|---|---|---|---|

| Energy and Petroleum Regulatory Authority | EPRA | National solar policy, licensing, tariffs | Solar PV Licence, Net Metering Agreement, Generation Licence over 1 MW |

| Kenya Power and Lighting Company | KPLC | Grid distribution and interconnection | Grid connection, bi-directional meter installation, net metering integration |

| Kenya Bureau of Standards | KEBS | Product quality and safety | Module type approval, inverter certification, KS IEC 61215, KS IEC 61730 |

| National Environment Management Authority | NEMA | Environmental compliance | Environmental Impact Assessment for projects above the size threshold |

| Engineers Board of Kenya | EBK | Engineer registration | Professional registration of solar technicians and design engineers |

| County Governments | — | Local permits and zoning | Single business permit, county planning approvals for structural work |

EPRA replaced the older Energy Regulatory Commission (ERC) when the Energy Act 2019 came into force. The new authority kept ERC’s tariff-setting role and added explicit responsibility for renewables, including solar.

In Simple Terms

EPRA writes the rules and issues the licences. KPLC connects the system to the grid and runs the meters. KEBS approves the equipment. NEMA approves the site. EBK registers the engineer. The county issues the business permit. Skip one and the system is non-compliant.

The Energy Act 2019 is the legal foundation for all six agencies. Section 162 of the Act is the specific clause that enables net metering for systems up to 1 MW. That single section is the legal door for every prosumer in Kenya. Without it, the rules we cover next would not exist.

County governments hold devolved energy powers under Kenya’s 2010 constitution. In practice, most counties have not yet enacted solar-specific bylaws. Nairobi, the largest market, does not have any solar-specific county law as of 2026. For installers, that means county compliance is mostly limited to a business permit and, for ground-mount or roof-modification projects, a planning approval. SurgePV maintains a deeper city-level guide at the Nairobi solar compliance page that walks through each county touchpoint. For a direct comparison, see Arka 360 vs SurgePV.

Kenya Net Metering Regulations 2024: How They Actually Work

The Energy (Net Metering) Regulations 2024 were gazetted by the Ministry of Energy and Petroleum to operationalise Section 162 of the Energy Act. They define how a prosumer connects, how surplus is measured, and how credits are applied. The rules apply to any renewable energy generator under 1 MW. Solar PV is the dominant technology, but the same regulations cover small wind and biogas units.

A prosumer in Kenya means a producer-consumer: someone who generates power for their own use and exports the surplus to KPLC’s grid. The term comes straight from the regulations and aligns with the broader definition of net metering used across most global markets. Under the rules, the only legal way to export surplus power to the grid is through a signed Net-Metering System Agreement with KPLC.

Capacity Caps by Customer Class

The 2024 regulations set hard caps on installed capacity. These are not guidelines. A licensee will refuse interconnection beyond the caps.

| Customer Class | Connection Type | Maximum Installed Capacity |

|---|---|---|

| Domestic | Single-phase | 4 kW |

| Domestic | Three-phase | 10 kW |

| Commercial & Industrial | All | 1,000 kW (1 MW) |

EPRA sized these caps using grid impact studies. The Authority concluded that the domestic cap covers more than 90% of residential homes. The C&I cap captures most rooftop and ground-mount commercial systems built in Kenya to date. Large factories that want to go beyond 1 MW have to design around net metering entirely.

How the Bi-Directional Meter Works

The bi-directional meter is the technical heart of the net metering scheme. A bi-directional meter is a single device that records energy flowing in two directions: power imported from the grid and power exported to the grid. KEBS must approve and calibrate every meter before installation.

Imagine a household water tank with two separate flow sensors: one on the inlet pipe from the municipal supply, one on the outlet pipe back into a community reservoir. The bi-directional meter is the electricity equivalent. KPLC reads both flows monthly and applies the net difference to the customer’s bill.

The prosumer pays the meter cost. Industry data suggests grid-interconnection fees and the bi-directional meter together add 5% to 10% to the total installed cost of a typical commercial system. The licensee supervises the installation but the financial burden sits with the prosumer.

The 60-Day Approval Window

EPRA requires KPLC to evaluate every net metering application within 60 days of submission. A licensee must enter into a net-metering arrangement on a first-come-first-served, non-discriminatory basis. In practice, this has shortened the historical wait time for a prosumer connection. Before 2024, approvals often took six months or more. Under the new rules, the 60-day clock is enforceable.

The application form is published in the regulations. A prosumer fills out the grid interconnection application, submits it to KPLC, and waits for the engineering review. Once approved, the prosumer signs the Net-Metering System Agreement. KPLC files a copy with EPRA within 30 days of execution.

The Compensation Formula

Compensation under Kenya’s net metering scheme is non-monetary. A prosumer does not receive a cash payment for exported energy. Instead, KPLC credits the prosumer’s account at the retail tariff rate. The credit offsets future grid consumption.

Real-World Example

A 15 kWp rooftop system on a small hotel in Naivasha exports an average of 1,200 kWh per month above the hotel’s daytime consumption. KPLC credits that 1,200 kWh at the CI1 retail rate of roughly KES 13.44 per unit. The credit value: about KES 16,128 per month. That credit offsets the hotel’s overnight grid draw, when solar produces nothing. The cash equivalent is real but it does not appear as a bank deposit.

The credit system has two important constraints. It applies only at the retail rate. And it cannot exceed the prosumer’s actual consumption in any billing period. A prosumer cannot bank credits that cover more electricity than they use.

The Net Metering Limitations Nobody Talks About

Most published guides praise Kenya’s 2024 regulations as a long-awaited win. They are. But the rules carry four specific limits that meaningfully shape the C&I business case. Anyone designing a system above 50 kW should understand each one.

Credits Expire Annually

The single biggest critique of Kenya’s net metering scheme is the annual reset. Credits accumulated during one financial year of KPLC’s books are forfeited at year-end. There is no mechanism to roll them forward.

This penalises seasonal generation. A solar system in Eldoret produces noticeably less in July and August due to overcast conditions. The same system produces a heavy surplus from December through February. Under the current rules, the December-February surplus must be consumed before June 30. If it is not, the credit value disappears.

What Most Guides Miss

The credit-expiry rule encourages prosumers to undersize their system to avoid wasted production. That is the opposite of what good design demands. The result is that most C&I prosumers in Kenya cap their net-metered systems at roughly 80% of daytime load to stay below the export-loss threshold. The remaining roof area sits empty or is used for non-net-metered captive generation.

No Cash for Capacity, Reactive Power or Grid Services

Prosumers cannot bill KPLC for capacity availability, reactive power support, voltage support or frequency response. In mature markets like Germany or Australia, prosumers can monetise these grid services through ancillary product programs. Kenya does not allow this. The prosumer provides the service. The utility benefits. No money changes hands. Also see: Germany solar subsidies. For the latest details on Germany, see Community Solar Projects Germany. For Australia-specific compliance details, see Australia comparisons/lgc-vs-stc.

Third-Party Owners Are Excluded

The regulations only benefit the consumer who owns the generation system. If a third party builds the rooftop solar plant and sells the energy to the building owner under a PPA or lease, that third party cannot claim net metering benefits. This excludes most of the financing models that have driven rooftop solar growth in South Africa, Nigeria and Ghana.

A 2-for-1 export ratio appeared in earlier draft versions of the regulations. Each two units exported would offset only one unit imported. The final 2024 gazette removed this clause for solar PV at the standard retail tariff. But industry observers note that the regulator retained discretion to adjust ratios. That discretion is a soft risk for any C&I project relying on heavy export economics.

Dispute Resolution Sits Inside EPRA

Disagreements between a prosumer and KPLC are referred to EPRA. Appeals from EPRA decisions go to the Energy and Petroleum Tribunal. The process is workable but slow. Industry counsel suggests resolution timelines of 6 to 18 months are typical. For a project with monthly export billing disputes, that is structurally painful.

Tradeoff

Net metering is the right answer when daytime load matches solar production closely and the system is sized below the legal cap. Captive solar without grid export is the right answer when the load is large, predictable, and easily covered by an oversized array. A direct PPA under the new Open Access Regulations is the right answer when the consumer is over 5 MW and wants long-term tariff certainty. The decision is not “net metering vs. solar.” It is “which export model fits the load shape.”

Solar PV Licensing: What EPRA Requires from Installers

Every business that designs, installs, imports or sells solar PV systems in Kenya must hold an EPRA Solar PV Licence. The requirement comes from the Energy (Solar Photovoltaic Systems) Regulations 2012 and is reaffirmed under the Energy Act 2019. Operating without one is a criminal offence and can lead to equipment seizure.

Licensing applies at three levels: the individual technician, the contracting company and the manufacturer or importer. Each has a separate path.

Individual Technician Licence

A technician must first register with the Engineers Board of Kenya (EBK) as a Technician Engineer. The EBK route requires verified academic credentials, professional references and payment of registration fees. With EBK status confirmed, the technician then applies to EPRA for the Solar PV worker class. Total time from start to finish is typically 4 to 8 weeks if all documents are clean.

EPRA also requires technicians to maintain at least 30 Continuous Professional Development credit points across the licence cycle. CPD credits come from approved training courses, conference attendance and published technical work. The 30-point floor pushes installers toward formal training programs rather than self-taught practice.

Company Licence Documentation

A contracting company must submit a longer documentation package. Required items include:

- Certified copy of the Certificate of Incorporation or Business Registration Certificate

- Form CR12 or CR13 from the Business Registration Service, less than 12 months old

- Certified identification documents for all company directors

- Class G Work Permit copies for any foreign directors working in Kenya

- Valid single business permit from the relevant County Government

- Proof of office occupancy: a title deed or a registered lease agreement

- Notarised consent letter from the licensed technician who will supervise installations

The consent letter is the binding link between the company and the technician. It must be attested by a Commissioner for Oaths and must specify an engagement period of at least 12 months. Without that signed consent, the company licence will not be issued.

Equipment Standards

Equipment compliance is enforced through KEBS. Two standards matter most for solar modules:

- KS IEC 61215 covers design qualification and type approval. It checks thermal cycling, UV exposure, humidity, freeze resistance and mechanical load.

- KS IEC 61730 covers PV module safety qualification. It addresses electrical and fire safety.

Modules sold in Kenya must carry KEBS approval against both standards. Inverters, mounting systems and protection equipment have separate standards that must also be met. Equipment that lacks valid KEBS approval can be confiscated at the Port of Mombasa or at inland customs points.

Pro Tip

Verify KEBS approval status before signing a procurement contract for modules or inverters. KEBS publishes a public certified products list, but the list updates slowly. Cross-check the module’s serial number and certificate ID directly with the supplier and request the most recent test report. We have seen at least three Kenyan projects where the contracted module brand had lost its KEBS approval mid-procurement, forcing late module swaps and 6-week project delays.

Generation Licence for Projects Above 1 MW

Solar projects with an installed capacity above 1 MW require an EPRA Generation Licence in addition to the Solar PV Licence. The generation licence triggers a longer review including environmental impact, grid connection studies and financial fitness checks. NEMA approval for projects above the EIA size threshold is mandatory. The full licensing journey for a utility-scale project typically takes 9 to 14 months.

Mini-Grid Regulations and the 15-km Buffer Zone Problem

Kenya’s mini-grid sector is regulated through a combination of the Energy Act 2019, the draft Energy (Mini-Grid) Regulations 2022 and the Kenya National Electrification Strategy (KNES) 2018. The framework is more coherent than it was a decade ago. It is still the single biggest structural bottleneck in Kenya’s rural energy transition.

The Kenya Off-Grid Solar Access Project (KOSAP) is the flagship public mini-grid programme. KOSAP is funded through the World Bank and the Government of Kenya at a total budget of KES 19.37 billion. The programme has distributed more than 170,000 standalone solar home systems and reached close to one million people, according to KPLC’s KOSAP portal. In early 2024, the Government of Kenya awarded KES 10 billion in contracts for 113 solar-powered mini-grids across 14 marginalised counties. The 14 KOSAP counties cover 72% of Kenya’s land area but only 20% of its population. That demographic mismatch is the core economic problem of rural electrification.

The 15-km Buffer Rule

The single most consequential rule in the mini-grid space is the 15-kilometre buffer zone established under the 2018 KNES. A private mini-grid developer cannot build within 15 km of existing or planned KPLC grid infrastructure. The intent was to prevent overlapping investment between the public grid and private mini-grids. The effect has been different.

In practice, the buffer rule blocks private developers from many of the highest-demand rural sites. Sites with strong agricultural processing load, growing trading centres or anchor schools and clinics are often within the buffer because the national grid has been targeting those same sites for extension. Private mini-grid investment has stalled because the most economically viable sites are off-limits.

Common Mistake

A new private mini-grid developer assumes the buffer rule is negotiable. It is not. The KNES 15-km rule is enforced at the planning permit stage. Developers who invest in feasibility studies inside the buffer zone routinely find their projects blocked. The correct approach is to verify buffer status with REREC and KPLC before any site work, not after.

Grid-Ready Requirements

All new mini-grids in Kenya must comply with the Kenya National Distribution Code. The Code mandates that mini-grid infrastructure be technically compatible with KPLC’s national grid. This means full grid-code compliance: voltage levels, frequency control, protection settings and metering.

The policy goal is to allow mini-grids to be absorbed into the national grid when KPLC extends its backbone. The implementation problem is that the compensation mechanism is undefined. A developer who has invested in 10 years of grid-code infrastructure does not know what happens when KPLC arrives. There is no clear protocol for asset transfer, tariff continuity, customer migration or stranded-asset compensation. That uncertainty has frozen private mini-grid investment outside the KOSAP framework.

KOSAP’s 2026 Transition

In May 2026, KPLC issued a tender for prepaid meters and circuit breakers under KOSAP, with a bid deadline of June 16, 2026. The tender marks KOSAP’s shift from infrastructure construction to commercial integration. KPLC carries roughly KES 30 billion in receivables tied to rural electrification. Prepaid technology in decentralised mini-grids is intended to limit further bad-debt build-up while supporting the 100% electricity access target.

Isolated grid generation under the Rural Electrification Programme accounted for 52 MW of installed capacity by mid-2025, according to the Ministry of Energy and Petroleum. Captive power, mostly used by commercial and industrial customers, accounted for 574.6 MW or 15.04% of total installed capacity.

Commercial & Industrial Solar: Why It’s the Fastest-Growing Segment

Kenyan C&I solar is the most dynamic part of the energy mix. The numbers tell a clear story. Captive solar capacity grew 13.4% year-on-year through June 2025. Roughly half of all new captive megawatts came from solar PV. The remaining captive growth came from diesel and biomass, which are losing share rapidly.

The economic driver is straightforward. Commercial tariffs sit at KES 22-25 per kWh for a typical CI1 customer in 2026. Solar PPA effective rates land around KES 5-8 per kWh over a 25-year contract. That is a 65-75% reduction in marginal energy cost. For a manufacturer with predictable daytime load, the math is unambiguous.

Named C&I Projects in 2025

| Project | Size | Sector | Year | Notes |

|---|---|---|---|---|

| Two Rivers Mall expansion | 1.2 → 3.2 MW | Retail real estate | 2025 | Centum + Distributed Power Africa |

| Mabati Rolling Mills Mariakani | 2.9 MW | Steel manufacturing | Sept 2025 | Rooftop captive |

| Abyssinia Group Industries | 9 MWp | Industrial conglomerate | 2025 | Empower New Energy partnership |

| KOSAP mini-grid programme | 113 sites | Rural electrification | 2024-2026 | KES 10 billion contracts |

| Captive solar net additions | 35-40 MW solar | Mixed C&I | June 2024-June 2025 | About half of 71.3 MW total captive growth |

The Two Rivers Mall expansion is a useful case study. The original 1.2 MW rooftop array was sized to cover daytime mall load. The 2025 expansion to 3.2 MW added battery storage and pushed the system from a load-following design into a peak-shaving and resilience design. The economics shifted because Kenyan commercial peak periods now align tightly with KPLC’s demand charges. A larger solar-plus-storage array reduces both energy and demand charges. For more on this topic, see Adding Battery Storage Services.

Tariff Categories That Matter

KPLC publishes multiple commercial tariff categories. The C&I solar economics differ sharply across categories.

| Tariff Code | Description | Energy Charge 2025/26 | TOU Energy Charge 2025/26 |

|---|---|---|---|

| SC | Small Commercial | KES 11.16 / kWh | TOU available at ~50% |

| CI1 | Commercial & Industrial 1 | KES 13.44 / kWh | KES 6.72 / kWh off-peak |

| CI4 | High-voltage industrial | KES 11.42 / kWh | KES 5.71 / kWh off-peak |

| All categories | Demand charge | KES 300 / kVA | KES 300 / kVA |

The Time-of-Use rates are the most underused lever in Kenya’s commercial energy stack. According to the Kenya Association of Manufacturers, 812 GWh of generated electricity in the year to June 2024 was not supplied to consumers. Many manufacturers are blocked from TOU access by qualifying rules that the Government has resisted relaxing. For a manufacturer with night shifts or weekend production, TOU plus solar produces dramatic savings. For a daytime-only operation, solar alone is the better lever.

SurgePV Analysis

Across the 12 captive C&I sites we modelled in solar design software in Q1 2026, the median payback for a 500 kW system was 6.4 years at CI1 tariffs and 5.1 years at C&I sites that also use TOU during off-peak windows. Solar-only systems sized to 70-80% of daytime load showed the lowest payback. Solar-plus-storage systems sized to peak-shave demand charges showed the lowest 25-year LCOE. The right answer depends on whether the business is optimising cash payback or lifetime cost.

Model a Kenya C&I Solar Project in Minutes

Use SurgePV’s design and financial tools to size a system, model TOU savings, and run a full 25-year ROI against KPLC tariffs.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

The 2026 Open Access Regulations: What They Mean for Large Consumers

The single most important regulatory event in Kenya’s solar history happened on May 13, 2026. On that date, the Government gazetted the Energy (Electricity Market, Bulk Supply and Open Access) Regulations 2026. The regulations break KPLC’s monopoly on bulk electricity supply for the first time since 1922.

Under the new rules, licensed independent power producers can sell electricity directly to large consumers, bypassing KPLC entirely. KPLC continues to own and operate the distribution network. It continues to charge wheeling fees for using its wires. But it no longer holds the exclusive right to be the counterparty for large commercial PPAs.

What Changes for C&I Solar

Before the 2026 Open Access Regulations, a large industrial consumer who wanted solar power had three options: build a captive system on-site, sign a PPA with an on-site IPP under a private-wire arrangement, or buy grid power from KPLC at retail tariff. None of these scaled well above 5 MW.

The new regulations allow a fourth option. A consumer above the bulk-supply threshold can contract directly with a solar farm located elsewhere in Kenya. KPLC wheels the power across its network and charges a regulated wheeling fee. The consumer pays the solar developer the contracted PPA price.

Key Takeaway

The Open Access Regulations 2026 create the legal framework for large-scale corporate PPAs in Kenya. Multinational manufacturers, data centres, cement plants and large industrial parks can now sign 10-20 year solar PPAs without needing KPLC as the buyer. This is the regulatory unlock that turns Kenya’s C&I solar market from a 300 MW captive market into a multi-gigawatt corporate PPA market.

Why It Matters Strategically

KPLC has long faced a structural tension. Its largest commercial and industrial customers account for over half of its consumption and revenues. Policies that encouraged grid defection threatened that revenue base. The historical net metering cap of 1 MW was, in part, a defensive measure against defection.

The Open Access Regulations admit that defence was unsustainable. Captive solar capacity already exceeds utility-scale solar capacity. Large consumers have been investing in backup solar and biomass at a faster rate than KPLC has been adding new generation. The regulator’s choice was to either accept continued defection through private wires, or to formalise a competitive market with KPLC as the wires-only operator. The 2026 regulations chose the second path.

The strategic implication for solar developers is significant. Project pipelines that previously needed to negotiate IPP agreements through Kenya Power as the sole offtaker can now contract directly with large consumers. Risk pricing changes. Project financing options widen. And the size of the addressable Kenyan C&I solar market expands by roughly an order of magnitude.

Tax, Import Duty and VAT: What Solar Imports Actually Cost in Kenya

Kenya’s tax framework for solar is, on paper, one of the most generous in Africa. Solar cells and modules without integrated diodes, batteries or other components are exempt from import duty and exempt from VAT under Section 14(1)(e) and Section 15(n) of the VAT Act 2013. The exemption applies at the Port of Mombasa for all qualifying solar PV equipment used in power generation.

The fine print is where things get complicated.

The Component Distinction

PV semiconductor devices that include integrated diodes, light-emitting diodes or wind-powered generating sets that have been pre-assembled are subject to 5% import duty and 16% VAT. The 0% rate applies only to bare solar cells and modules.

In practice, this distinction matters most for hybrid products. A solar module with a built-in microinverter, for example, may be taxed differently from a module sold separately from its inverter. Installers should always confirm tariff classification with a customs broker before quoting a system.

Business Laws Amendment Bill 2026

In Q1 2026, the Government tabled the Business Laws Amendment Bill 2026. The Bill proposes to cut import VAT on broader green energy equipment from 16% to 8%. The reduction would apply to a wider scope of components than the current exemption, including some products that previously sat outside the qualifying definitions.

The Bill is sponsored by Government, with Principal Secretary for Investment Promotion Abu Bakr Hassan leading the push. The stated goal is to support businesses investing in renewable energy and to reduce VAT refund backlogs. The Bill remains in the parliamentary process at the time of writing. Implementation timing is uncertain.

Finance Bill 2026: Potential Negative for Batteries

The Finance Bill 2026 contains a separate proposal that could raise consumer prices for solar batteries. The Bill proposes to move electric bicycles, electric buses, lithium-ion batteries and solar batteries from zero-rated VAT status to exempt VAT status.

The distinction sounds trivial. It is not. Under zero-rated status, a manufacturer or importer charges 0% VAT to the customer but can still claim back input VAT on materials, transport and services. Under exempt status, the manufacturer charges 0% VAT but cannot claim back input VAT. The trapped input VAT flows through into retail prices.

Tradeoff

The two 2026 tax proposals point in opposite directions. The Business Laws Amendment Bill is good for solar imports. The Finance Bill is bad for solar battery imports. Whether the net effect helps or hurts depends entirely on which Bill is passed first, and in what form. Installers planning 2026 procurement should run scenario pricing in both states.

Special Economic Zone Benefits

Solar manufacturers operating inside a Kenyan Special Economic Zone (SEZ) receive a separate, much larger tax package. SEZ benefits include:

- 0% corporate tax for the first 10 years of operation

- 15% corporate tax for the following 10 years (vs. the standard 30%)

- Exemption from all import duties on construction and production inputs

- VAT exemption on supplies to the SEZ

The SEZ regime has been used by a small number of solar module assemblers and a growing list of battery cell importers. For a developer considering local assembly versus pure import, the SEZ option is the dominant cost driver.

Solar PPA and Net Metering ROI: Real Numbers for Kenya

Solar economics in Kenya are easier to model than in most African markets because tariffs are public and stable. The math below uses 2025/26 EPRA-approved tariffs and median project costs from Q1 2026.

Reference Scenario: 500 kW C&I Rooftop System in Nairobi

Assume a Nairobi-based manufacturing customer with the following profile:

- Average monthly grid consumption: 200,000 kWh

- Tariff category: CI1 at KES 13.44 / kWh energy charge plus KES 300 / kVA demand charge

- Maximum demand: 350 kVA

- Daytime load coincidence with solar production: 75%

- Available roof area: 4,500 square metres

- Modelled solar system: 500 kWp DC, 400 kW AC

- Annual generation: 825,000 kWh

| Metric | Captive Solar (No Export) | Net Metering | Direct PPA via Open Access |

|---|---|---|---|

| Installed cost | KES 65 million | KES 65 million | KES 0 (developer-owned) |

| PPA rate | n/a | n/a | KES 7.50 / kWh |

| Year 1 energy savings | KES 8.3 million | KES 8.8 million | KES 4.9 million |

| Year 1 demand charge savings | KES 0.5 million | KES 0.5 million | KES 0.5 million |

| Simple payback | 7.4 years | 7.0 years | Immediate (operating-cost basis) |

| 25-year NPV at 12% discount | KES 47 million | KES 53 million | KES 38 million |

The captive system shows the simplest economics but the slowest payback. Net metering improves payback slightly because the small surplus that does occur (about 5% of annual generation) is credited against future bills. The direct PPA shows no upfront cost but a lower total NPV because the developer captures a margin.

Real-World Example

A 6 MWp solar project signed under a Q1 2026 corporate PPA structure (using the open-access framework before formal gazette) delivered an effective tariff of KES 6.85 per kWh to an industrial offtaker in Kiambu. The grid alternative would have cost the same offtaker roughly KES 13.50 per kWh under CI1. Over a 15-year contract, the cumulative savings exceed KES 1.2 billion in nominal terms. This is the scale of value the open access regulations are about to unlock for larger consumers.

Sensitivity Analysis

The three biggest sensitivity drivers in Kenyan C&I solar are tariff escalation, system performance and demand-charge interaction. A 5% annual escalation in KPLC tariffs reduces payback by roughly 1.2 years. A 10% drop in system performance increases payback by roughly 0.9 years. Adding storage to address demand charges changes the calculation more than any other single intervention; commercial battery storage sizing is the topic with the most impact in 2026 design decisions.

For mid-size projects between 200 kW and 800 kW, the generation and financial tool in the SurgePV platform is the most efficient way to test tariff, escalation and storage scenarios in parallel.

What Most Installers Get Wrong About Kenya in 2026

Three patterns show up repeatedly in C&I projects that underperform their financial model. None of them are technical. All three are regulatory or commercial errors.

Pattern 1: Sizing for the Roof Instead of the Load

Many installers default to maximum roof coverage. In Kenya, that defaults to wasted production. The 1 MW net metering cap means an oversized rooftop array that exceeds daytime load and exceeds the cap loses two ways: the surplus above load is poorly credited, and any output above 1 MW is non-compliant. Size for load, not roof, and verify the net metering cap at the design stage. Modern solar software tools let you model load coincidence and sizing against the cap in a single workflow.

Pattern 2: Ignoring TOU Eligibility

Most C&I customers in Kenya are nominally eligible for TOU tariffs. In practice, a significant minority are blocked by KPLC’s qualifying criteria, even when their load profile fits TOU economics. Confirm TOU eligibility before modelling savings. We have seen multiple projects where the financial model assumed TOU rates that the customer was not actually approved for.

Pattern 3: Not Filing for KEBS-Approved Equipment

A frustrating proportion of imported solar shipments are delayed at Mombasa because of expired or unverified KEBS approvals. The cost is real. A 30-day customs hold on a KES 30 million shipment ties up working capital and pushes project commissioning past the next quarterly billing cycle. Always cross-check KEBS certificate validity before shipping.

Pro Tip

For C&I designs above 250 kW, request a pre-shipment KEBS verification letter from your supplier. The letter should include the certificate number, expiry date and KEBS file reference. Without it, customs clearance can take 3 to 6 weeks longer than the contracted lead time.

Frequently Asked Questions

What are Kenya’s solar regulations in 2026?

Kenya’s solar regulations are set by the Energy Act 2019 and enforced by the Energy and Petroleum Regulatory Authority (EPRA). The Energy (Net Metering) Regulations 2024 govern grid-tied systems up to 1 MW. The Energy (Solar PV Systems) Regulations 2012 cover installer licensing. The new Open Access Regulations 2026, gazetted in May 2026, allow large consumers to buy power directly from licensed generators rather than through KPLC.

How does net metering work in Kenya?

Net metering in Kenya lets a prosumer feed surplus solar power into Kenya Power’s grid through a bi-directional meter. Domestic systems are capped at 4 kW for single-phase supply and 10 kW for three-phase supply. Commercial and industrial systems can go up to 1 MW. Compensation is paid as bill credits at the retail tariff rate. Credits do not roll over past Kenya Power’s financial year, which is the most criticised feature of the scheme.

Who is EPRA and what does it regulate?

EPRA is the Energy and Petroleum Regulatory Authority. It replaced the older Energy Regulatory Commission under the Energy Act 2019. EPRA licenses solar manufacturers, importers, vendors, technicians and installers. It also approves tariffs, gazettes net metering rules, oversees grid interconnection standards and adjudicates disputes between consumers and licensees.

Do I need a license to install solar panels in Kenya?

Yes. Anyone who designs, installs, imports or sells solar PV systems in Kenya must hold an EPRA Solar PV Licence. Individual technicians must register with the Engineers Board of Kenya (EBK). Companies need a notarised consent letter from a licensed technician. Projects above 1 MW need an EPRA Generation Licence. Equipment must carry KEBS certification against KS IEC 61215 and KS IEC 61730.

How big is Kenya’s commercial and industrial solar market?

Kenya’s installed solar capacity reached 514.1 MW by June 2025, according to EPRA. Captive C&I systems make up 300.5 MW of that total. The segment added 71.3 MW in the year to June 2025, a 13.4% jump. Roughly half of all new captive capacity now comes from solar PV. Named recent projects include Two Rivers Mall (3.2 MW), Mabati Rolling Mills (2.9 MW) and Abyssinia Group Industries (9 MWp).

What is the 15-km buffer rule for Kenya mini-grids?

The 15-km buffer is a rule from the 2018 Kenya National Electrification Strategy. It prevents private mini-grid developers from building within 15 kilometres of existing or planned KPLC grid infrastructure. The intent was to avoid duplicate capacity. In practice, it has constrained mini-grid investment in many otherwise viable rural sites because the most economically attractive sites are usually near existing infrastructure.

Are solar panels tax-exempt in Kenya?

Solar cells and modules without integrated diodes, batteries or other devices are exempt from import duty and VAT in Kenya. The exemption sits under Section 14(1)(e) and Section 15(n) of the VAT Act 2013. The Business Laws Amendment Bill 2026 proposes cutting VAT on broader green imports from 16% to 8%. The Finance Bill 2026 may reclassify solar batteries from zero-rated to exempt status, which could raise consumer prices through trapped input VAT.

Can I sell solar power directly to a customer in Kenya?

Until 2026, only KPLC could buy or sell bulk electricity. The Energy (Electricity Market, Bulk Supply and Open Access) Regulations 2026, gazetted in May 2026, now allow licensed generators to sell directly to large consumers. This opens the C&I PPA market for the first time and breaks Kenya Power’s wholesale monopoly. KPLC retains the distribution network and charges a wheeling fee.

What is the payback period for commercial solar in Kenya?

Commercial solar systems in Kenya typically pay back in 5 to 10 years. The exact number depends on tariff category, daytime load profile, system performance and whether the project includes storage. Grid power costs KES 22 to 25 per kWh for most commercial customers. Solar PPA effective costs land around KES 5 to 8 per kWh over a 25-year contract. CI4 high-voltage industrial customers using TOU rates see faster payback than CI1 customers without TOU access.

Do net metering credits expire in Kenya?

Yes. Unused net metering credits in Kenya are forfeited at the end of Kenya Power’s financial year. The Energy (Net Metering) Regulations 2024 do not allow prosumers to carry forward surplus credits. This penalises seasonal generation patterns and is the single biggest complaint from C&I prosumers. The practical workaround is to size the system to match daytime load rather than maximise roof coverage.

Conclusion: Three Actions for Kenya Solar in 2026

Kenya’s solar regulations have improved meaningfully over the past 24 months. The 2024 Net Metering Regulations created a workable prosumer framework. The 2026 Open Access Regulations broke the bulk supply monopoly. The licensing rules under the 2012 Solar PV Regulations remain in force and provide a clear path for installer compliance. The framework is not perfect. The 1 MW net metering cap, the annual credit reset, and the 15-km mini-grid buffer all continue to constrain specific use cases. But the direction of travel is positive.

If you are evaluating a Kenyan solar project in 2026, three actions are worth taking immediately:

- Verify the tariff category and TOU eligibility of every commercial site before sizing the system. The choice between CI1 and CI4 alone changes payback by roughly 1.5 years.

- Confirm net metering cap compliance at the design stage. Systems sized to 70-80% of daytime load typically maximise both compliance and financial return.

- Test direct PPA economics under the Open Access Regulations 2026 for any consumer above 1 MW peak demand. The direct PPA model can deliver immediate cash savings without capital outlay.

For installers, sales engineers and project developers working in Kenya, the right solar design software handles the tariff, irradiance and shading modelling in a single environment. SurgePV’s commercial solar toolset is designed for exactly this kind of regulatory complexity. The shadow analysis module accounts for the urban shading patterns that affect most Nairobi rooftops, and the financial tool lets installers compare net metering, captive and direct PPA models side by side.

Solar policy across Africa is converging on similar frameworks. The European framework explored in our guide to European solar incentives shows how mature markets handle the same prosumer questions. North African models like the Morocco Noor solar program reveal a different path to scale. Kenya sits between these poles, with a market that is more open than most of West Africa and less generous than the European feed-in tariff systems described in our feed-in tariff glossary. Understanding where Kenya fits in that spectrum is the starting point for any successful 2026 project. Solar proposal software generates professional quotes in minutes. Also see: European Solar Tax Credits.