Quick Answer

Brazil's 2026 solar incentives center on net metering under Law 14,300/2022, state ICMS exemptions on equipment via Convênio ICMS 101/97, subsidised BNDES financing, and federal TUSD/TUST tariff reductions under Law 14,120/2021. The zero-import-tax window for solar panels is closing in stages during 2026, so project timing matters.

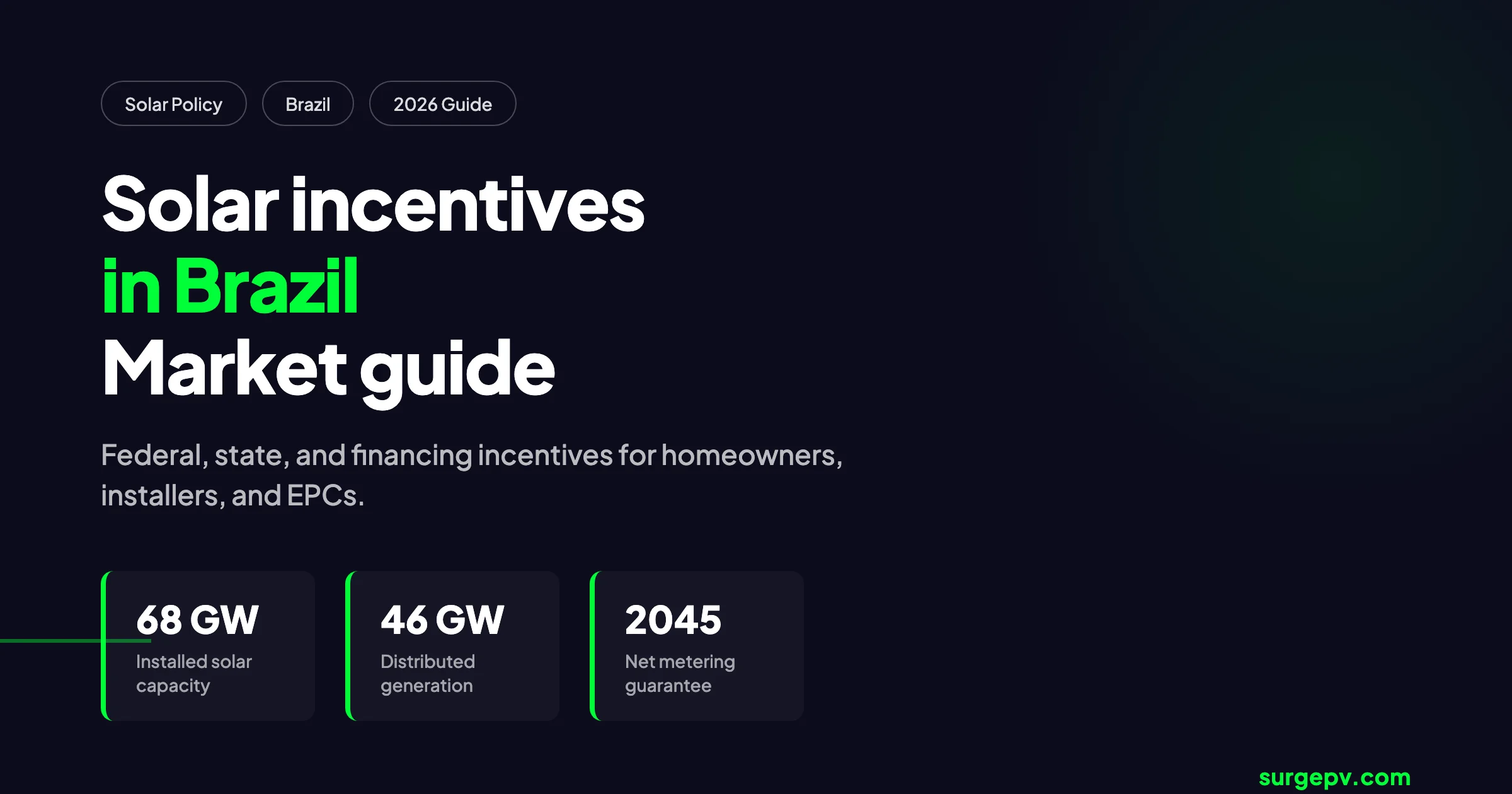

Brazil became the world’s fifth-largest solar market in less than a decade. By early 2026, installed photovoltaic capacity reached 68 GW. Distributed generation accounted for 46 GW and centralized solar farms for 22.3 GW, according to ANEEL data reported by PV Magazine (2026). That scale was built on high irradiance, expensive grid electricity, and a layered incentive system of tax exemptions, subsidised credit, and favourable net metering.

This guide is a market-focused manual for homeowners, installers, EPCs, and investors who need to understand what is actually active in Brazil in 2026. It covers the legal framework, the federal and state incentive stack, financing, commercial and utility-scale support, and the policy shifts changing project economics right now. For the broader Brazilian solar market context, see our solar energy in Brazil 2026 guide.

If you are sizing systems or preparing proposals for Brazilian clients, a solar design platform with local tariffs can save hours on every project. Model payback, self-consumption ratios, and tax effects automatically, then generate solar proposals in minutes. Check pricing or book a demo to see how SurgePV handles Brazil.

Quick Answer

Brazil’s 2026 solar incentives center on net metering under Law 14,300/2022. State ICMS exemptions on equipment, subsidised BNDES financing, and federal TUSD/TUST reductions under Law 14,120/2021 are also active. The zero-import-tax window for solar panels is closing in stages during 2026, so project timing matters.

In this guide:

- Latest 2026 status of every active Brazilian solar incentive

- The legal foundation: Law 14,300/2022, ANEEL, and net metering

- Federal incentives: import tax, IPI, PIS/COFINS, PADIS, and TUSD/TUST

- State incentives: ICMS exemptions and regional variation

- Financing: BNDES, BNB, Caixa, Banco do Brasil, and rural credit

- Commercial, industrial, and utility-scale support, including the ACL free market

- Three real-world stacking examples with payback impact

- Common mistakes and how to avoid them

Latest Updates: Brazil Solar Incentives 2026

The Brazilian solar policy environment changed materially in 2025 and early 2026. Import tax exemptions on panels began to expire. Net metering surcharges continued their scheduled rise. The free energy market opened to a much larger pool of commercial consumers. For installers and project developers, the practical effect is that every proposal must be rebuilt around the 2026 rulebook, not the older, more generous framework.

Brazil Solar Incentive Status — June 2026

| Incentive | Type | Status | Key Terms |

|---|---|---|---|

| Net metering under Law 14,300/2022 | Regulatory | Active | Guaranteed until 2045 for systems under 5 MW; TUSD surcharge rising through 2029 |

| ICMS exemption on solar equipment | State tax break | Active in most states | Convênio ICMS 101/97; rates vary 12–25% by state |

| TUSD/TUST tariff reduction | Federal tariff break | Active, reduced for new projects | Law 14,120/2021; sliding scale by commissioning year |

| BNDES Finame Baixo Carbono | Subsidised financing | Active | Effective rates typically 10–14% p.a. for C&I and residential |

| BNB FNE Sol / Pronaf Eco | Regional/rural financing | Active | Northeast-focused FNE Sol; family-farmer Pronaf Eco near 3% p.a. |

| Zero import tax on solar panels | Federal import break | Phasing out in 2026 | Gecex/Camex schedule; some quota exemptions remain |

| PADIS manufacturer incentives | Federal tax exemption | Active for qualified producers | IPI, PIS/COFINS exemptions on qualified solar equipment |

| Infrastructure debentures | Tax-advantaged bonds | Active for utility-scale | REIDI and green-bond structures for qualifying projects |

| Free energy market ACL | Market access | Expanding August 2026 | All low-voltage C&I customers become eligible |

| Tax reform EC 132/2023 | Structural change | Transition started | ICMS, IPI, PIS, COFINS, ISS replaced by CBS/IBS between 2027 and 2033 |

Key Changes Since 2025

Import tax on solar panels is returning. After years of zero rates, Gecex/Camex began reinstating import duties on photovoltaic panels and cells in stages during 2025. By mid-2026, duties could reach 35% for some product categories, according to Click Petróleo e Gás (2026). Some quota-based exemptions remain, but the trend is clear: imported equipment will cost more.

TUSD surcharge continues to rise. Law 14,300/2022 introduced a progressive distribution tariff surcharge on exported energy. The surcharge started low in 2023 and reaches the full TUSD rate by 2029. Systems installed before January 2023 were grandfathered under the old rules. Every new project must model this erosion of net metering value.

ACL opens to all low-voltage C&I consumers in August 2026. The free energy market was previously restricted to large consumers. From August 2026, any low-voltage commercial or industrial consumer can negotiate directly with generators and traders. This is a major new route for corporate solar PPAs and remote self-consumption.

Tax reform begins its transition. Constitutional Amendment 132/2023 and Supplementary Law 214/2025 launched the replacement of ICMS, IPI, PIS, COFINS, and ISS with CBS and IBS. The transition runs from 2026 to 2033. ICMS exemptions on solar equipment will remain in force until ICMS is fully phased out, but the state-based incentive structure will disappear after 2033.

Key Takeaway

2026 is a transition year for Brazilian solar incentives. The most reliable tools are net metering, ICMS exemptions, and BNDES financing. The import tax change is the single biggest new variable and must be checked before every equipment purchase.

Why Brazil’s Incentive Stack Matters in 2026

Brazil has some of the world’s best solar resources. Global horizontal irradiance ranges from 4.8 kWh/m²/day in the South to 6.2 kWh/m²/day in the Northeast. The country also has high retail electricity tariffs, which makes self-consumption valuable. The gap between solar potential and deployment is now mostly a question of financing cost, administrative complexity, and installer ability to stack incentives.

Market Size and Targets

Brazil reached 68 GW of total solar capacity by early 2026, according to ANEEL data reported by PV Magazine. The distributed segment alone accounted for 46 GW, with roughly 3.9 million systems connected. The Brazilian Photovoltaic Solar Energy Association (Absolar) forecasts 10.6 GW of new additions in 2026 and total capacity of approximately 140 GW by 2031.

Solar generated 70.7 TWh in 2024, up 39.6% year on year. Installed capacity at that point was 48.5 GW, according to the BEN 2025 energy balance reported by GNPW Group (2026). Solar and wind together supplied nearly 24% of Brazil’s electricity.

What the Transition Means for Incentives

The old model of generous import tax exemptions and grandfathered net metering is fading. The new model relies on three pillars: correctly sized self-consumption systems, low-cost public financing, and state tax exemptions that the national VAT reform will eventually replace.

For installers, this means proposals must emphasise avoided retail electricity purchases rather than export revenue. A kWh consumed on site offsets the full retail tariff, which often exceeds R$ 0.80/kWh for residential and C&I consumers. A kWh exported earns a credit that is gradually losing value as the TUSD surcharge rises.

For homeowners and businesses, the message is similar: the best 2026 incentive is a correctly sized system paired with low-cost BNDES financing. A solar design platform that models Brazilian tariffs, the TUSD surcharge schedule, and self-consumption ratios can show the real payback, not a simplistic estimate.

The Legal Foundation: Law 14,300/2022 and Net Metering

Every Brazilian solar incentive is built on the same legal base. Law 14,300/2022, known as the Marco Legal da Geração Distribuída, replaced ANEEL Resolution 482/2012 and created a 23-year regulatory horizon for distributed generation.

What Law 14,300/2022 Changed

| Before Law 14,300/2022 | After Law 14,300/2022 |

|---|---|

| Net metering rules under ANEEL Resolution 482/2012 | Dedicated federal law with guarantee until 2045 |

| No clear long-term regulatory certainty | 23-year participation guarantee for systems under 5 MW |

| Limited shared generation options | Shared generation and remote self-consumption legalised |

| No distribution tariff surcharge for prosumers | Gradual TUSD surcharge on exported energy through 2029 |

System Size Categories

Brazilian distributed generation uses two main size categories:

- Microgeração: systems up to 75 kW. These qualify for full net metering compensation.

- Minigeração: systems from 75 kW to 5 MW. These also qualify for net metering but under terms that include the TUSD surcharge and may have different compensation ratios.

Battery storage systems can qualify for net metering up to a 3 MW cap. The rules are administered by ANEEL through Normative Resolution No. 1,000/2021, amended by Resolution No. 1,059/2023.

Net Metering in Practice

Under the Sistema de Compensação de Energia Elétrica, surplus solar generation is exported to the grid and credited in kWh, not in cash. Credits can offset consumption at the same consumer unit for up to 60 months. Shared generation allows multiple consumer units to share credits from one installation, provided they are in the same concession area or meet remote self-consumption rules.

The value of a credit depends on the consumer’s tariff class. Because the credit offsets energy, distribution, and tax components, it is typically worth more than the simple wholesale price of electricity. However, the rising TUSD surcharge reduces the effective value of exported kWh over time.

The TUSD Surcharge Schedule

| Period | TUSD Treatment for Exported Energy |

|---|---|

| Pre-January 2023 systems | Grandfathered; no surcharge |

| 2023 | Low initial surcharge |

| 2024–2025 | Progressive increases |

| 2026 | Mid-transition rate |

| 2029 onwards | Full TUSD rate on exports |

The exact percentage varies by distribution utility and tariff class. For a residential consumer in São Paulo, the 2026 surcharge may reduce the value of exported energy by roughly 20–30% compared with the pre-2023 regime. By 2029, the reduction could approach 50%.

Federal Tax Incentives and Financing

Brazil does not offer a single federal solar tax credit. Instead, it layers multiple federal instruments. These include import tax and IPI exemptions on equipment, PADIS manufacturer incentives, TUSD/TUST tariff reductions, and subsidised financing through BNDES and other public banks.

Import Tax, IPI, and PIS/COFINS on Equipment

The Lula administration announced a “zero tax” policy for solar panels in 2023, covering import tax, IPI, and COFINS, according to TV BRICS (2023). The programme was allocated more than R$600 million and was tied to the inclusion of solar cells in the PADIS semiconductor support programme.

That policy is now reversing. Gecex/Camex has begun reinstating import duties on photovoltaic panels and cells in stages during 2025 and 2026. By July 2026, import duties could reach 35% for some categories, according to Click Petróleo e Gás (2026). Some quota-based exemptions remain for certain import volumes, but the general direction is toward restored taxation.

This is the single most important equipment-cost variable for 2026. A residential system priced at R$ 20,000 under the zero-tax regime could cost R$ 25,000 or more once import duties are fully restored.

PADIS for Manufacturers

The Programme for the Support of the Technological Development of the Semiconductor Industry, or PADIS, was extended to cover solar photovoltaic manufacturing. Qualified companies receive exemptions from IPI on products and capital goods, and from PIS/COFINS on sales of qualified equipment, according to PV Know How (2025).

PADIS eligibility requires a commitment to local research and development spending. The application process can take several months and demands a detailed investment plan. For domestic module assemblers, PADIS is a prerequisite for competing with imported panels once import duties return.

TUSD/TUST Tariff Reductions

Law 14,120/2021 provides reductions in the Distribution System Usage Tariff and Transmission System Usage Tariff for qualifying renewable energy generators. The benefit depends on the commissioning year and project size.

| Commissioning Period | Typical TUSD/TUST Treatment |

|---|---|

| Before 2020 | 100% reduction for 10 years under original framework |

| 2020–2023 | Partial reductions on sliding scale |

| 2024 onwards | Reduced but still available in modified form |

For utility-scale solar farms in the Northeast, TUST exemptions have historically been a major component of project economics. Their value has been progressively reduced for newer projects but remains meaningful for bankable revenue projections.

PROINFA and FUNGET

PROINFA, the Programme for the Incentive of Alternative Sources of Electricity, was created by Law 10,438/2002. It primarily supports wind, biomass, and small hydro, but it has shaped the broader renewable finance environment. In December 2025, ANEEL approved PROINFA cost quotas for 2026 totaling R$ 5.23 billion, a 14.99% reduction from 2025, according to ANEEL (2025).

FUNGET, the Fundo de Universalização dos Serviços de Telecomunicações, has also supported distributed generation deployment in rural and remote areas. These funds are administered by ANEEL and public banks, not by end consumers directly.

State-Level Incentives: ICMS Exemption

The most valuable state-level solar incentive is the ICMS exemption. ICMS is the state tax on the circulation of goods and services, similar to a value-added tax. Rates vary from 12% to 25% depending on the state and product.

Convênio ICMS 101/97

Convênio ICMS 101/97 authorises Brazilian states to exempt solar and wind energy equipment from ICMS. Most major states have adopted the exemption, including São Paulo, Minas Gerais, Rio de Janeiro, Paraná, Rio Grande do Sul, Bahia, Ceará, and Piauí. The exemption typically covers modules, inverters, charge controllers, mounting structures, and metering equipment.

The effective saving depends on the state rate. In São Paulo, where the general ICMS rate is 18%, the exemption reduces equipment cost by roughly that amount. In states with higher rates, the saving is larger.

How the Tax Reform Affects ICMS

Brazil’s tax reform, approved as Constitutional Amendment 132/2023, will replace ICMS, IPI, PIS, COFINS, and ISS with two VAT-style taxes. CBS will apply at the federal level and IBS at the state and municipal level. The transition runs from 2026 to 2033.

For solar, the key implication is that state-level ICMS exemptions will disappear as ICMS is phased out between 2029 and 2033. The reform may introduce new national incentives for renewable energy, but these had not been fully defined at the time of writing. Long-term financial models should include a scenario without ICMS savings.

Financing: BNDES, BNB, and Public Credit

Public financing is arguably Brazil’s most powerful solar incentive. Commercial consumer credit in Brazil often runs at 15–30% per year. BNDES and regional public banks can offer far lower rates, which changes payback dramatically.

BNDES Finame Baixo Carbono

The BNDES Finame Baixo Carbono line finances solar equipment for residential, commercial, and industrial projects. The bank operates through accredited commercial banks, so borrowers do not deal directly with BNDES. Equipment must be listed in the BNDES CFI supplier registry.

The effective rate has three components:

| Component | Typical Value |

|---|---|

| Base financial cost, usually TLP | ~7–8% p.a. |

| BNDES remuneration | 0.75% p.a. |

| Bank spread | 1.5–3.5% p.a., negotiable |

| Effective total | ~10–14% p.a. |

Rates vary with market conditions and borrower risk. BNDES financing can cover up to 100% of eligible equipment and up to 30% of installation costs. Terms reach up to 10 years, with grace periods of up to two years, according to Energia Solar Explicada (2026).

In May 2026, BNDES updated the Fundo Clima Automático line for solar. The financial cost is 9.5% per year, plus the BNDES fee and bank spread. The programme allows financing up to 100% of investment, terms up to 16 years, and grace periods up to five years.

Banco do Nordeste FNE Sol

The Banco do Nordeste do Brasil operates the FNE Sol line for renewable energy projects in the Northeast region, northern Minas Gerais, and northern Espírito Santo. The line serves individuals, companies, and rural producers. Terms can reach 12 years with grace periods up to 24 months. Rates are typically subsidised and can be lower than BNDES Finame for qualifying borrowers.

Pronaf Eco and Rural Credit

For family farmers enrolled in the National Programme for Strengthening Family Agriculture, Pronaf Eco offers renewable-energy credit at rates near 3% per year. The loan limit is R$ 165,000 per year for agricultural activities. This is one of the cheapest solar financing routes in Brazil but is restricted to qualifying rural borrowers.

Caixa Econômica Federal and Banco do Brasil

Caixa offers solar financing through Construcard Verde and energy-specific lines, sometimes packaged with home construction or renovation credit. Banco do Brasil offers BNDES Finame repurchase lines and its own renewable energy credit for individuals and companies, with terms typically up to 8–12 years.

Pro Tip — Compare CET, Not Just the Headline Rate

The Custo Efetivo Total, or CET, includes interest, IOF, administrative fees, insurance, and appraisal costs. Always ask the bank for the CET in writing before comparing financing options. A lower nominal rate with high fees can be more expensive than a higher rate with lower fees.

Commercial, Industrial, and Utility-Scale Incentives

Residential self-consumption gets the most attention, but Brazil’s solar market is large across all segments. C&I and utility-scale projects use different incentive logic.

C&I Self-Consumption and the Free Energy Market

The C&I segment benefits from net metering under Law 14,300/2022 and from the expansion of the free energy market. From August 2026, all low-voltage commercial and industrial consumers can migrate to the ACL. This allows them to sign bilateral power purchase agreements directly with generators or traders registered with CCEE.

Two arrangements dominate the C&I solar market:

- On-site self-generation: Install solar on the company’s roof or land and offset consumption through net metering.

- Corporate solar PPA: Buy solar power from a third-party generator under a long-term contract, often indexed to inflation rather than utility tariffs.

The second option is attractive for businesses that lack suitable rooftop space. It does not use net metering but provides price certainty for 10–20 years.

Utility-Scale Solar

Utility-scale projects above 5 MW do not use the distributed generation net metering framework. They operate in the regulated market, through ANEEL auctions, or in the free market through merchant sales or PPAs.

Key federal supports for utility-scale solar include:

- TUSD/TUST reductions under Law 14,120/2021

- REIDI: Special Regime of Incentives for Infrastructure Development, which suspends PIS/COFINS on equipment and construction

- Infrastructure debentures: Tax-advantaged bonds for qualifying renewable energy projects

- BNDES Finem Geração de Energia: Direct financing for large projects above R$ 5–10 million

Major utility-scale development is concentrated in the Northeast, where Bahia, Piauí, and Ceará combine the country’s best irradiance with available land and transmission access.

How to Apply for Solar Incentives in Brazil

The application sequence in Brazil is more about documentation, registration, and financing than about a single grant form. Getting the order wrong can delay connection by months or void eligibility.

Step 1 — Confirm Eligibility and System Size

Start with a 12-month load profile. Collect electricity bills to understand consumption patterns, peak demand, and tariff class. Size the system to maximise self-consumption rather than generation. For most residential consumers, a system covering 70–90% of annual consumption is optimal.

Check whether the state offers ICMS exemption on solar equipment. This affects the equipment quote and must be reflected in the invoice.

Step 2 — Choose a Certified Installer

ANEEL requires that distributed generation systems be installed by qualified professionals. The installer is responsible for the technical project, the ART (technical responsibility annotation), and submission to the distribution utility. Ask for:

- Proof of installer qualification and ART

- Reference projects of similar size

- Written quote separating equipment, labour, and taxes

- Confirmation that equipment has BNDES CFI codes if financing is planned

Step 3 — Verify Equipment Tax Status

Confirm whether the quoted equipment is subject to import tax, IPI, PIS/COFINS, or ICMS. In 2026, this is the most volatile part of the quote. Panels imported after mid-2026 may carry restored import duties of up to 35%. Domestic or PADIS-qualified panels may avoid some of these taxes.

Step 4 — Apply for Financing Before Installation

If using BNDES or public bank financing, start the credit analysis before ordering equipment. The bank will require the formal quote, installer documentation, and borrower financials. Approval typically takes 5–15 business days after a complete file is submitted.

Step 5 — Submit the Distributed Generation Access Request

The installer submits the access request to the distribution utility through ANEEL’s regulated process. Under ANEEL Normative Resolution No. 1,000/2021, distribution utilities cannot charge for access analysis for systems up to 75 kW. They must also replace the conventional meter with a bidirectional meter at their own cost.

Step 6 — Commission and Register the System

After installation, the system is inspected and commissioned. The utility activates net metering, and credits begin to accrue. For shared generation or remote self-consumption, additional registration steps are required with ANEEL and the utility.

Step 7 — Monitor Credit Balance and Tariff Changes

Track the credit balance and the TUSD surcharge schedule. Credits expire after 60 months if unused. As the surcharge rises through 2029, the value of exported energy falls, so system size and self-consumption ratio become even more important.

How to Stack Incentives: Three Real-World Scenarios

The following examples are illustrative, based on typical 2026 costs and incentive rates. Actual figures depend on location, installer quote, tariff class, financing terms, and whether import tax exemptions still apply to the equipment.

Scenario 1 — 5 kWp Residential, São Paulo

| Item | Amount |

|---|---|

| Gross installed cost | R$ 22,000 |

| ICMS exemption on equipment (18%) | −R$ 2,800 |

| Net equipment and installation cost | R$ 19,200 |

| BNDES Finame financing at 12% p.a., 96 months | R$ 19,200 financed |

| Monthly financing payment | ~R$ 310 |

| Monthly electricity bill saving | ~R$ 420 |

| Net monthly cash flow | +R$ 110 |

| Simple payback if financed cash-flow neutral | ~4.5 years |

Without BNDES financing, the same household might pay commercial credit at 20% p.a. The monthly payment would exceed the savings, turning the project cash-flow negative for several years.

Scenario 2 — 75 kWp Commercial, Minas Gerais

| Item | Amount |

|---|---|

| Gross installed cost | R$ 280,000 |

| ICMS exemption on equipment (17%) | −R$ 34,000 |

| BNDES Finame at 11% p.a., 120 months | R$ 246,000 financed |

| Annual electricity saving | R$ 72,000 |

| Annual financing payment | R$ 34,000 |

| Net annual cash flow | +R$ 38,000 |

| Simple payback | ~3.8 years |

The project relies on high daytime consumption to maximise self-consumption. Export revenue is secondary. With the TUSD surcharge rising, sizing at 75 kWp instead of 100 kWp keeps the self-consumption ratio high.

Scenario 3 — 1 MWp Utility-Scale, Bahia

| Item | Amount |

|---|---|

| Gross installed cost | R$ 2,800,000 |

| REIDI PIS/COFINS suspension | −R$ 180,000 |

| TUST reduction benefit over 10 years | −R$ 420,000 |

| Infrastructure debenture tax benefit | −R$ 150,000 |

| Net effective cost | R$ 2,050,000 |

| Annual revenue from PPA at R$ 220/MWh | R$ 330,000 |

| Simple payback | ~6.2 years |

Utility-scale economics depend on the PPA price, land cost, and transmission access. Northeast projects benefit from irradiance of 5.5–6.2 kWh/m²/day, which lifts capacity factors above 22%.

Common Mistakes and Misconceptions

Even experienced installers lose money on Brazilian projects by mishandling the incentive sequence. Here are the most common errors.

Assuming the Zero Import Tax Still Applies

This is the most expensive 2026 mistake. The zero-import-tax policy is ending in stages. Panels ordered in mid-2026 may be subject to restored duties of up to 35%. Quotes must specify whether the price includes current import taxes or assumes an exemption that may no longer exist.

Ignoring the TUSD Surcharge Schedule

Many proposals still model net metering as if it were 2022. Law 14,300/2022 introduces a rising surcharge through 2029. A project with attractive payback today may look mediocre in 2029 if the model assumes full net metering value for the entire system lifetime.

Oversizing for Export

Because exported energy loses value as the TUSD surcharge rises, every oversized kWp wastes capital. A system sized for 75–85% self-consumption ratio usually outperforms a larger system with high export.

Missing the ICMS Exemption in the Quote

Some installers quote equipment with ICMS included, even when the state exempts solar equipment. The invoice must be structured correctly to claim the exemption. Homeowners should ask for the CFOP tax code and confirm the exemption with the state tax authority.

Financing Without Checking CET

A “low” BNDES rate can be misleading if the bank adds high fees, insurance, or IOF. Always compare the CET across at least two financing proposals. The cheapest nominal rate is not always the cheapest total cost.

Applying Residential Logic to C&I Projects

C&I projects should evaluate the ACL free energy market from August 2026 onward. A corporate PPA or remote self-consumption arrangement may deliver lower cost and less regulatory risk than an on-site net metering system.

Brazil Solar Incentives Outlook for 2026–2027

The next 18 months will determine whether Brazil’s distributed solar market keeps growing or slows. Restored import taxes and rising net metering surcharges are the main weights. Three factors are worth watching closely.

The Import Tax Transition

The phased return of import duties on solar panels is the biggest near-term variable. If domestic manufacturing scales quickly under PADIS, the price impact may be modest. If domestic supply cannot meet demand, equipment prices could rise sharply in late 2026. The Gecex/Camex schedule and any quota extensions should be monitored monthly.

The Tax Reform

The transition from ICMS, IPI, PIS, and COFINS to CBS and IBS will reshape solar economics between 2027 and 2033. The reform promises simpler compliance and full tax credits, but it removes state-level ICMS exemptions. Whether the new framework includes targeted renewable energy incentives will be critical for long-term project returns.

The Free Energy Market Expansion

The August 2026 opening of the ACL to all low-voltage C&I consumers is a structural change. It allows small and mid-sized businesses to access corporate PPAs and remote self-consumption for the first time. This could shift C&I solar growth away from rooftop net metering and toward contracted off-site supply.

Conclusion

Brazil’s solar incentive framework in 2026 is still supportive, but it is no longer as simple as it was two years ago. Net metering remains guaranteed until 2045, yet its value is being eroded by the TUSD surcharge. State ICMS exemptions are still widely available, but they will disappear after 2033 under tax reform. BNDES financing remains a powerful tool, while the zero-import-tax policy is ending and pushing equipment costs up.

For solar professionals, the competitive edge is threefold: model the full incentive stack accurately, apply for financing early, and size systems for self-consumption. Tools like Clara AI and SurgePV’s generation and financial tool can automate that workflow for Brazilian projects.

Three actions to take now:

- Verify equipment tax status before quoting — confirm whether import duties, IPI, and ICMS apply to the specific panels and inverters.

- Model the TUSD surcharge through 2029 — size systems for high self-consumption and conservative export value.

- Compare public financing CETs — BNDES and regional banks can cut total financing cost by 30–50% compared with commercial credit.

For the broader Latin American context, see our solar energy in Brazil 2026 guide. For installers looking to scale, our guide for solar installers covers proposal automation and compliance workflows.

Frequently Asked Questions

What solar incentives are available in Brazil in 2026?

Active solar incentives in Brazil for 2026 include net metering under Law 14,300/2022. State ICMS exemptions on equipment, federal TUSD/TUST tariff reductions under Law 14,120/2021, and subsidised BNDES financing are also available. Rural credit lines such as FNE Sol and Pronaf Eco, plus infrastructure debentures, support specific segments. Several federal tax exemptions on imported panels are being phased out during 2026.

How does net metering work in Brazil?

Brazil’s net metering system is called the Sistema de Compensação de Energia Elétrica. Surplus solar generation is exported to the grid and credited in kWh. These credits offset future consumption over up to 60 months. Systems up to 75 kW receive full compensation. Systems from 75 kW to 5 MW can participate under modified terms. Law 14,300/2022 guarantees the framework until 2045 but introduces a rising TUSD surcharge through 2029.

What is Law 14,300/2022 for solar in Brazil?

Law 14,300/2022 is the Marco Legal da Geração Distribuída. It governs distributed generation and guarantees net metering until 2045 for systems below 5 MW. It enables shared generation and remote self-consumption. It also introduces a gradual distribution tariff surcharge on exported energy from 2023 to 2029. Systems connected before January 2023 were grandfathered under older, more favourable rules.

Is there a federal solar tax credit in Brazil like the US ITC?

No. Brazil does not have a single federal investment tax credit for solar. The incentive structure is a stack of tax exemptions, subsidised financing, and tariff reductions. The main federal tools are import tax and IPI exemptions on equipment, PIS/COFINS exemptions under PADIS for manufacturers, TUSD/TUST tariff reductions, and BNDES credit lines.

Which Brazilian states exempt solar equipment from ICMS?

Most major states have adopted ICMS exemptions for solar equipment under Convênio ICMS 101/97. These include São Paulo, Minas Gerais, Rio de Janeiro, Paraná, Rio Grande do Sul, and the Northeast states. Rates and exact product coverage vary, so installers must check the current SEFAZ ruling in each state. ICMS exemptions will be phased out between 2030 and 2033 under Brazil’s tax reform.

How much does BNDES financing cost for solar in Brazil in 2026?

BNDES Finame Baixo Carbono for solar typically carries an effective annual rate of roughly 10% to 14% in 2026, well below commercial consumer credit. The rate combines the TLP base cost, a 0.75% BNDES fee, and a negotiable bank spread. Special rural lines such as Pronaf Eco and FNE Sol can be lower, sometimes near 3% to 5% for qualifying family farmers and Northeast borrowers.

Are solar panels taxed on import in Brazil in 2026?

Yes. The zero-import-tax policy for solar panels is being phased out in stages during 2026. Some quota-based exemptions may apply to certain volumes, but the general trend is toward restored import duties that could reach 35% by mid-2026 under Gecex/Camex resolutions. Projects importing equipment should confirm the current rate before ordering.

What is the difference between microgeração and minigeração in Brazil?

Microgeração covers renewable systems up to 75 kW. These qualify for full net metering under the Sistema de Compensação de Energia Elétrica. Minigeração covers systems from 75 kW to 5 MW. They also qualify for net metering but under terms that include a gradual TUSD surcharge and different compensation ratios depending on the connection date and segment.

What is the free energy market in Brazil for solar?

The Ambiente de Contratação Livre, or ACL, lets eligible consumers buy electricity directly from generators or traders through bilateral contracts registered with CCEE. From August 2026, all low-voltage commercial and industrial customers can enter the ACL. This opens corporate solar PPAs and remote self-consumption to small and mid-sized businesses.

What is the biggest mistake when applying for Brazilian solar incentives?

The costliest mistake is assuming the 2026 incentive stack is the same as 2023 or 2024. Import tax exemptions are ending, TUSD surcharges are rising through 2029, and ICMS exemptions will disappear after 2030. Proposals must be modelled with current equipment costs, current financing rates, and the correct tariff surcharge schedule.