Quick Answer

Solar energy in Brazil costs R$3.50–R$5.50 per watt peak installed. Net metering under Law 14.300 allows 100% compensation for systems up to 75 kW and 80% for larger systems. PROINFA and FUNGET incentives support distributed generation. The Brazilian solar market grew 70% in 2024, reaching 40 GW total installed capacity.

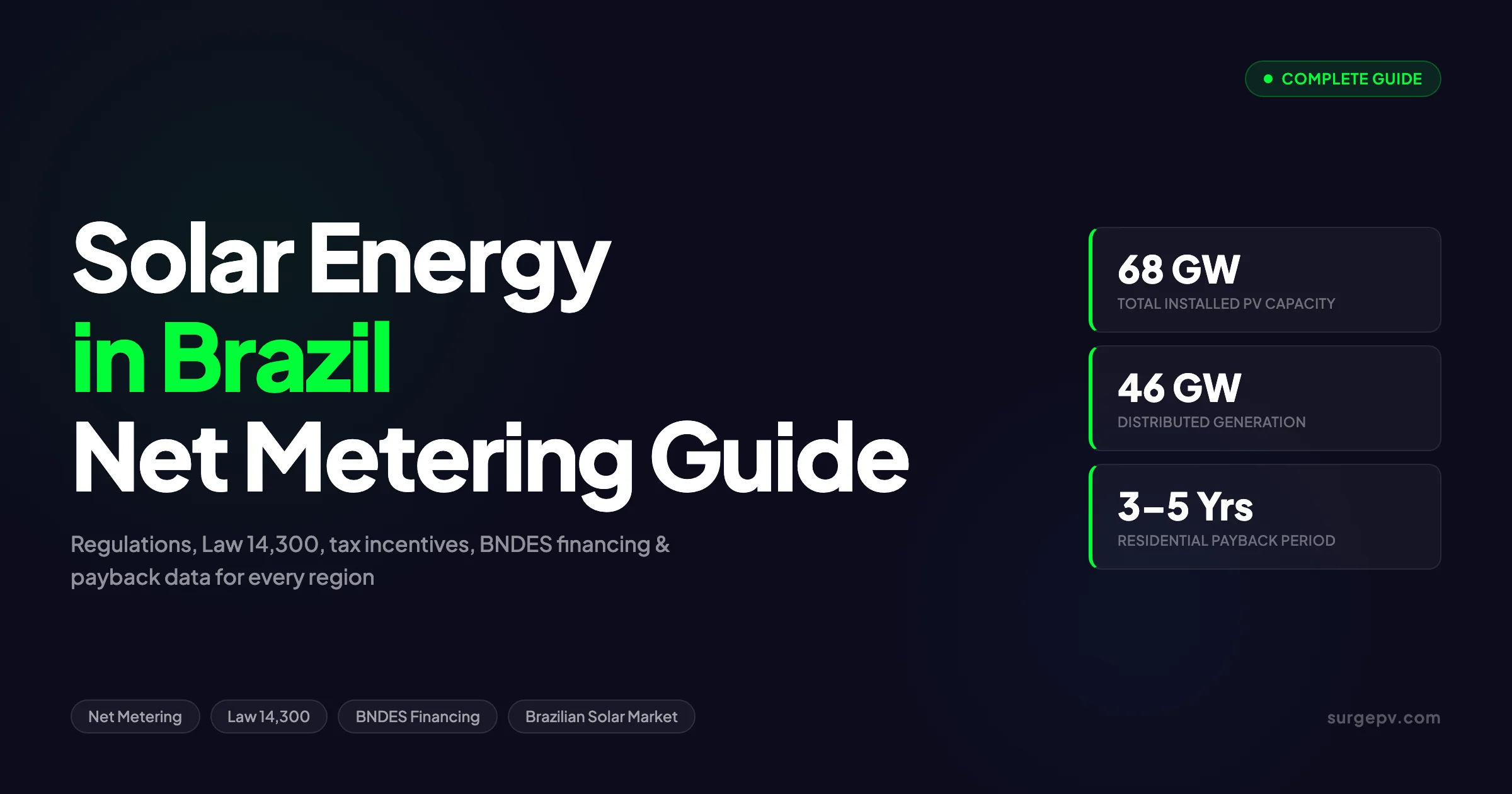

Brazil is the world’s fifth-largest solar market — and the fastest-growing among the top ten. With 68 GW of installed PV capacity by early 2026, split between 46 GW of distributed generation and 22.3 GW of centralized farms, the country has built one of the most significant solar industries outside of China in less than a decade. This guide covers how Brazil’s net metering system works under the Marco Legal (Law 14,300/2022), which states offer the best tax incentives and irradiance, what a rooftop system actually costs in reais and when it pays back, how the free energy market opens new doors for commercial solar from August 2026, and where the market is headed through 2031.

Solar energy in Brazil costs R$3.50–R$5.50 per watt peak installed. Net metering under Law 14.300 allows 100% compensation for systems up to 75 kW and 80% for larger systems. PROINFA and FUNGET incentives support distributed generation.

Solar energy in Brazil costs R$3.50–R$5.50 per watt peak installed. Net metering under Law 14.300 allows 100% compensation for systems up to 75 kW and 80% for larger systems. PROINFA and FUNGET incentives support distributed generation. The Brazilian solar market grew 70% in 2024, reaching 40 GW total installed capacity.

TL;DR — Brazilian Solar in 2026

Brazil has 68 GW of installed PV capacity and expects 10.6 GW of new additions in 2026. Net metering under Law 14,300/2022 is guaranteed until 2045 but carries a rising distribution surcharge through 2029. Residential payback runs 3–5 years with BNDES financing available at ~3% p.a. The free energy market opens to all low-voltage commercial and industrial customers in August 2026.

Brazil’s Solar Market: Scale and Context

Distributed solar generation in Brazil grew from under 1 GW in 2018 to 46 GW by 2026 — a 46-fold expansion in eight years. That trajectory is not an accident of geography or policy alone. It reflects falling equipment costs, high electricity tariffs that make solar savings immediate, and a regulatory framework that, while imperfect, has provided enough certainty for millions of homes and businesses to invest.

Total installed PV capacity across Brazil stood at 68 GW in early 2026, comprising:

| Segment | Installed Capacity | Share |

|---|---|---|

| Distributed Generation (rooftop, small-scale) | 46 GW | 68% |

| Centralized (utility-scale solar farms) | 22.3 GW | 32% |

| Total | 68 GW | 100% |

The Brazilian Photovoltaic Solar Energy Association (Absolar) forecasts 10.6 GW of new additions in 2026, with total capacity reaching approximately 75.87 GW by year-end. By 2031, the market is projected to reach 140.25 GW — a CAGR of 13.07%.

In the first two months of 2026, Brazil added 2,331 MW:

- Centralized: 1,186 MW (more than doubled year-on-year)

- Distributed: 1,145 MW (down 37% on the prior year’s pace, reflecting post-incentive normalisation)

The distributed generation segment’s short-term cooling is structural, not cyclical. Law 14,300/2022 introduced a distribution tariff surcharge that increases annually through 2029, reducing the financial advantage of net metering for new installations compared to the old regime. Utility-scale additions, by contrast, are accelerating as grid infrastructure catches up with demand.

Key Takeaway

Brazil’s solar market is bifurcating: utility-scale additions are surging as grid-scale economics improve, while distributed generation growth is moderating due to the tariff phase-in under Law 14,300. Both segments remain strong by global standards.

For Global-specific compliance details, see Global net-metering-by-country.

How Net Metering Works in Brazil

Brazil’s net metering system is formally called the Sistema de Compensação de Energia Elétrica (electricity energy compensation system). It functions differently from net metering in the United States or Australia — understanding the distinction matters for financial modelling. See our guide on Solar Energy in Australia for more. For Australia-specific compliance details, see Australia comparisons/lgc-vs-stc.

The Basic Mechanics

When a solar system generates more electricity than the property consumes at any given moment, the surplus is exported to the grid. The grid operator credits the prosumer’s account in kWh — not in cash. Those credits can then offset future electricity consumption at any point within the next 60 months.

The key difference from simple net metering: Brazil credits kilowatt-hours, not monetary value. The credit offsets your usage rate — which includes the cost of energy, distribution fees, and taxes — making the effective value per kWh exported higher than in markets where only the energy component is credited. Also see: Us Residential Solar Market Trends 2026.

Who Qualifies

Under the current framework:

- Microgeração: systems up to 75 kW — eligible for full net metering

- Minigeração: systems from 75 kW to 5 MW — eligible for net metering under certain conditions

- Technologies covered: solar PV, wind, biomass, small hydro, and qualified cogeneration

Eligible technologies must use renewable sources. Systems with battery storage are subject to a 3 MW cap to qualify for net metering. For more on this topic, see Adding Battery Storage Services.

Credit Validity and Rollover

Credits are valid for 60 months from the billing period in which they are generated. Unused credits expire — a consideration for system sizing in climates with strong seasonal variation. Most of Brazil has high year-round irradiance, so seasonal imbalances are less pronounced than in Europe, but sizing still matters. Also see: European Solar Incentives.

Shared Arrangements (Geração Compartilhada)

Law 14,300/2022 expanded the framework to allow shared generation: multiple units in a condominium or cooperative can share credits from a single solar installation. This opened rooftop solar to apartment residents who previously could not install their own system.

Remote self-consumption (autoconsumo remoto) allows credits from a solar installation at one property to be used at a different property, provided both are registered to the same legal entity or consumer group. This is particularly relevant for agribusiness and companies with multiple sites.

See also: Spain net metering.

Pro Tip

For businesses with multiple sites in the same distribution area, remote self-consumption under Law 14,300/2022 allows a single large solar installation — potentially on cheaper industrial land — to supply multiple commercial or industrial addresses. The economics often exceed site-by-site rooftop installations.

Law 14,300/2022: The Marco Legal Explained

Law 14,300/2022, known as the Marco Legal da Microgeração e Minigeração Distribuída, is the most consequential piece of solar legislation in Brazil’s history. It replaced the previous framework under ANEEL Resolution 482/2012 and its subsequent amendments, providing long-term legal certainty for the distributed generation sector.

What the Law Guarantees

Net metering until 2045: Any solar system below 5 MW connected under the distributed generation framework retains the right to participate in the energy compensation system until 31 December 2045. This 23-year guarantee removed the legislative risk that had slowed some commercial investments.

Grandfathering for existing installations: Systems connected before the law took full effect in January 2023 were grandfathered under the previous, more favourable rules for the life of the installation.

The Distribution Tariff Phase-in

The trade-off in Law 14,300/2022 is a gradual increase in the distribution tariff (TUSD) charged to prosumers on the energy they export. The logic: as more solar penetrates the grid, non-solar customers would face rising costs to maintain the distribution network that solar prosumers use at no charge. The law redistributes this cost back to prosumers progressively.

| Period | Distribution Tariff Applied to Exports |

|---|---|

| Pre-2023 (grandfathered) | No surcharge |

| 2023 | ~15% of TUSD applicable |

| 2024–2025 | Progressive increases |

| 2029 onwards | Full TUSD rate applicable |

The financial impact depends on your distribution company and tariff class. For most residential consumers in 2026, the surcharge reduces the effective value of exported energy but does not eliminate the advantage of solar — self-consumption remains highly favourable regardless.

ANEEL’s Implementation Rules

ANEEL implemented the law through Ruling No. 1,000/2021 (amended by Ruling No. 1,059/2023), which specifies:

- Connection procedures and timelines for distributed generators

- Metering requirements for prosumers

- Billing and credit accounting rules

- Obligations for distribution utilities

Distribution utilities are required to connect qualifying distributed generation systems within a defined timeline. Delays by the utility are subject to regulatory penalties — a provision that improved connection speeds significantly after 2022.

Key Takeaway

Systems installed before January 2023 operate under the old, more favourable regime with no TUSD surcharge. If you have an older installation, the financial case for keeping it running until its end-of-life is strong. New installations need to model the surcharge phase-in into their payback projections.

ANEEL and the Regulatory Framework

ANEEL (Agência Nacional de Energia Elétrica) is Brazil’s federal electricity regulator, operating under the Ministry of Mines and Energy. It sets the rules for every aspect of the electricity sector — generation, transmission, distribution, and commercialisation.

For solar specifically, ANEEL’s responsibilities include:

Distributed generation regulation: Setting connection standards, approving the metering framework, and overseeing distribution utilities’ compliance with connection timelines.

Public auctions: Conducting energy auctions on behalf of the federal government. ANEEL’s 2026 Long-Term Reserve Capacity Auction, held in March 2026, contracted approximately 19 GW of firm capacity — the largest reliability-focused procurement in Brazil’s history — expected to mobilise USD 12–13 billion in investments.

Battery storage auctions: A dedicated battery energy storage auction was scheduled for April 2026 with 18 GW of registered projects, the first of its kind in Brazil.

Environmental licensing: Solar installations require prior, installation, and operation licences. Small and medium-scale projects can access simplified state-level licensing procedures in most states.

The Two Energy Market Segments

Brazil’s electricity market has two distinct trading environments:

ACR (Ambiente de Contratação Regulado): The regulated market, where distribution utilities procure electricity through ANEEL-administered auctions. Residential and smaller commercial consumers are typically served under this system.

ACL (Ambiente de Contratação Livre): The free market, where eligible consumers negotiate directly with generators and traders through bilateral contracts registered with CCEE (Câmara de Comercialização de Energia Elétrica). This market is where corporate solar PPAs operate.

From August 2026, all low-voltage industrial and commercial customers gain access to the ACL — a major expansion that allows a far wider range of businesses to contract renewable energy directly, whether through PPAs or on-site self-generation structures.

Design Solar Systems Built for the Brazilian Market

SurgePV’s generation and financial tool models Brazilian electricity tariff structures, net metering credits, and self-consumption scenarios for any site.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

For a direct comparison, see Arka 360 vs SurgePV.

Tax Incentives and Financing

Brazil’s solar incentive structure is distributed across federal and state instruments. No single rebate program exists like Australia’s STC scheme — instead, the savings come from tax exemptions, subsidised financing, and tariff structures.

ICMS Exemption (State-Level)

The ICMS (Imposto sobre Circulação de Mercadorias e Serviços) is a state-level value-added tax on goods and services, including electricity. Convênio ICMS 101/97 authorises Brazilian states to exempt solar and wind energy equipment from ICMS. Most major states have adopted this exemption, including São Paulo, Minas Gerais, and Rio de Janeiro.

The exemption applies to:

- Solar panels and modules

- Inverters and charge controllers

- Mounting structures

- Metering equipment

The effective saving depends on the ICMS rate in your state, which ranges from 12% to 25%. In high-ICMS states like São Paulo (18%), the exemption meaningfully reduces the cost of equipment.

Important 2026 update: Brazil’s comprehensive tax reform (approved in 2023, taking effect progressively) will phase out ICMS entirely from 2030 to 2033 as the new CBS and IBS consumption taxes replace the existing system. State-level solar incentives tied to ICMS will diminish progressively from 2030. Projects evaluating long-term incentive stacking should factor this into lifecycle financial models.

TUSD/TUST Exemptions (Federal)

Law 14,120/2021 provides tariff reductions on the Distribution System Usage Tariff (TUSD) and Transmission System Usage Tariff (TUST) for qualifying renewable energy generators. Projects connected to the distribution or transmission grid under certain capacity and technology thresholds can reduce or eliminate these infrastructure charges for up to 10 years.

The exemption percentage depends on the commissioning year:

- Projects commissioned before 2020: 100% TUSD/TUST reduction for 10 years (under the original framework)

- More recent projects: partial reductions on a sliding scale

For utility-scale solar farms in the Northeast, TUST exemptions have historically been a major component of project economics. Their value has been progressively reduced for newer projects but remains available in modified form.

BNDES Financing

The Brazilian Development Bank (BNDES) is the primary public financing channel for solar energy. Its Finame programme provides equipment financing with subsidised interest rates. For small-scale solar installations — including residential and rural applications — BNDES has offered rates as low as approximately 3% per annum, well below commercial lending rates in Brazil (which often run 15–30% per annum for consumer credit).

Other public financing sources:

- BNB (Banco do Nordeste do Brasil): Specifically targets the Northeast region with favourable terms for rural and residential solar, aligned with the high-irradiance potential of the region

- Banco do Brasil and Caixa Econômica Federal: Both offer credit lines for solar installations, frequently packaged with financing for other home improvements

- Infrastructure Debentures: Tax-advantaged bonds for qualifying renewable energy infrastructure projects, primarily used for utility-scale development

Pro Tip

BNDES rates for solar are typically 8–12 percentage points below commercial loan rates. For a R$25,000 residential system, the difference between BNDES financing at 3% and a consumer credit line at 20% is approximately R$12,000 in total interest payments over 5 years. Always compare BNDES-eligible installer quotes against commercially financed options.

Tax Reform Implications for Solar

Brazil’s 2026 tax reform consolidates multiple federal and state taxes into CBS (Contribuição sobre Bens e Serviços) and IBS (Imposto sobre Bens e Serviços). The transition affects solar in two ways:

- ICMS exemptions on equipment will disappear progressively from 2030 to 2033

- The new CBS/IBS framework may offer solar-specific incentives, but these have not been fully defined

Businesses planning solar investments beyond 2030 should model scenarios with and without ICMS savings to stress-test their financial cases.

Solar by Region and State

Brazil’s solar irradiance is exceptional across most of the country, with Global Horizontal Irradiance (GHI) ranging from 5.0 to 6.2 kWh/m²/day across nearly the entire territory. The variation between best and worst locations is smaller than in most European or North American markets — even the south of Brazil receives more solar radiation than the sunniest parts of Germany. Also see: Germany solar subsidies.

Regional Irradiance Overview

| Region | GHI Range | Key States | Best Use |

|---|---|---|---|

| Northeast | 5.5–6.2 kWh/m²/day | Bahia, Piauí, Ceará, RN | Utility-scale solar farms |

| Center-West | 5.2–6.0 kWh/m²/day | Goiás, Mato Grosso, MS | Agrivoltaics, rural solar |

| Southeast | 5.0–5.8 kWh/m²/day | São Paulo, Minas Gerais, RJ | Distributed generation, commercial |

| South | 4.8–5.5 kWh/m²/day | Paraná, RS, SC | Distributed generation |

| North | 5.0–6.0 kWh/m²/day | Pará, Amazonas | Rural and off-grid |

Top States by Distributed Solar Capacity

The states with the most rooftop and small-scale solar reflect economic activity and policy environment more than raw irradiance:

| State | Distributed Solar Capacity | Driver |

|---|---|---|

| São Paulo | 5.8 GW | Largest economy, high tariffs, strong installer ecosystem |

| Minas Gerais | 4.9 GW | Strong rural sector, good irradiance, CEMIG tariff rates |

| Paraná | 3.7 GW | High energy costs, Copel tariff increases |

| Rio Grande do Sul | 3.4 GW | Strong agribusiness adoption |

| Mato Grosso | 2.6 GW | Rural and agro-industrial demand |

Utility-Scale Solar: The Northeast Dominance

The Northeast region hosts the majority of Brazil’s utility-scale solar farms, combining the country’s best irradiance with available land and grid access. Bahia (1,354 MW), Piauí (1,205 MW), and Ceará (499 MW) lead the centralized capacity rankings. ANEEL’s 2026 auction additions are expected to further concentrate utility-scale development in this region.

The Northeast’s Dual Advantage

The same states that dominate utility-scale solar are also home to Brazil’s lowest electricity tariffs — historically, because of large hydropower resources. As drought cycles reduce hydro output, electricity tariffs in the Northeast have risen, paradoxically making distributed solar more financially attractive in the region with the best solar resource in the country.

System Costs and Payback

Brazil’s solar installation costs have fallen sharply since 2020, driven by imported panel price reductions and a growing domestic installer base. Prices vary significantly by state, system type, and equipment quality.

Residential System Costs

| System Size | Typical Cost Range | Monthly Generation (est.) | Best For |

|---|---|---|---|

| 2–3 kWp | R$8,000–R$13,000 | 240–360 kWh | Small apartments, low consumption |

| 4–5 kWp | R$11,000–R$12,500 | 480–600 kWh | Average family home (~300 kWh/month) |

| 6–8 kWp | R$20,000–R$25,000 | 720–960 kWh | High-consumption homes, small pools |

| 10–12 kWp | R$25,000–R$35,000 | 1,200–1,440 kWh | Large homes, home offices, EVs |

Rondônia is currently the cheapest state for residential solar at R$2.30/Wp, followed by Roraima (R$2.34/Wp) and Amapá (R$2.36/Wp). São Paulo typically runs higher at R$2.70–R$3.20/Wp due to labor costs and logistics.

Commercial System Costs

| System Size | Typical Cost Range | Payback Period |

|---|---|---|

| 15–30 kWp | R$40,000–R$70,000 | 4–5 years |

| 30–75 kWp (microgeração cap) | R$70,000–R$150,000 | 3–5 years |

| 75 kW–500 kWp (minigeração) | R$150,000–R$900,000 | 3–6 years |

| 500 kWp–5 MW | R$900,000–R$9M+ | 5–8 years |

Self-Generation vs PPA: The 2026 Numbers

A 2026 analysis by PV Magazine found that solar self-generation at commercial and industrial sites can deliver up to 32.9% in energy cost savings compared to purchasing electricity under a power purchase agreement. The gap exists because self-consumption offsets the full retail tariff (including distribution fees and taxes), while PPA electricity is priced at wholesale generation cost.

For businesses with high daytime consumption profiles — retail, manufacturing, food processing, logistics — self-generation through solar design software that models consumption overlap is the most financially compelling option in the Brazilian market.

Key Takeaway

In Brazil, self-consumption at the commercial rate saves roughly 3–4x more per kWh than selling surplus back to the grid. Any commercial site with significant daytime energy demand should size its system to maximise self-consumption before considering export revenue.

Payback Scenarios

Residential (4 kWp system, R$12,000 net cost, São Paulo):

- Monthly consumption: 300 kWh

- System generation: ~480 kWh/month (São Paulo irradiance, north-facing roof)

- Self-consumption (50%): 240 kWh × R$0.85/kWh tariff = R$204 saved

- Credits exported (50%): 240 kWh credited at full tariff value

- Monthly bill saving: ~R$400 (60–70% bill reduction)

- Simple payback: ~2.5 years

Commercial (50 kWp system, R$110,000, Minas Gerais):

- Generation: ~6,000 kWh/month

- Self-consumption (70%): 4,200 kWh × R$0.72/kWh = R$3,024/month

- Export credits (30%): 1,800 kWh credited

- Monthly saving: ~R$4,300

- Simple payback: ~25 months

Using the generation and financial tool to model consumption overlap accurately is the difference between a realistic projection and an optimistic one that causes post-installation disappointment.

Commercial Solar and the Free Energy Market (ACL)

Brazil’s Ambiente de Contratação Livre (ACL) — the free energy market — is the most significant policy development for commercial and industrial solar buyers in 2026.

How the ACL Works

In the ACL, eligible consumers negotiate electricity supply directly with generators or traders through bilateral contracts. These contracts are registered with CCEE (Câmara de Comercialização de Energia Elétrica), which acts as the market operator and settles commercial positions.

For solar buyers, the ACL enables two arrangements:

- Corporate Solar PPA: Purchase solar-generated electricity from a third-party generator at a negotiated price, typically indexed to inflation rather than ANEEL’s tariff reviews. Locks in energy cost certainty for 10–20 years.

- Self-generation / Remote Self-consumption: Install solar capacity at a separate location and route credits to consumption sites — fully enabled under Law 14,300/2022.

The August 2026 Market Opening

Before 2019, only large industrial consumers above 3 MW of demand could access the ACL. Progressive threshold reductions have brought eligibility down to 500 kW, and from August 2026, all low-voltage commercial and industrial customers can migrate to the free market regardless of consumption volume.

This opens corporate solar PPAs and direct renewable energy contracting to small and mid-sized businesses — restaurants, offices, retail chains, hotels — for the first time. Analysts expect a surge in solar PPA deal volume in H2 2026 as this cohort begins evaluating its options.

Pro Tip

Businesses migrating to the ACL after August 2026 face a minimum contract term of typically 12 months and switching costs back to the regulated market. The decision is not easily reversed — financial modelling over a 5–10 year horizon is important before migrating. Solar self-generation paired with ACL migration often delivers the strongest combined saving.

Corporate Solar PPA Structure in Brazil

A corporate solar PPA in Brazil typically works as follows:

- An investor or developer builds a solar farm

- The C&I consumer signs a 10–20 year energy supply agreement

- The CCEE settles the contract — the consumer receives “green energy” certification

- Price is usually fixed in R$/MWh with inflation indexation (typically IGP-M or IPCA)

PPA prices for utility-scale solar in Brazil in 2026 run approximately R$200–R$280/MWh for new contracts — well below the regulated residential tariff (R$700–R$900/MWh all-in), making the saving case compelling for large consumers.

Utility-Scale Solar and Public Auctions

Brazil’s centralized solar market operates primarily through government-administered energy auctions held by ANEEL and the Ministry of Mines and Energy. These auctions are the main mechanism for adding large-scale renewable capacity to the grid.

How Auctions Work

Developers bid to supply electricity at a stated price per MWh for a defined contract period (typically 20–30 years). The lowest-price bids that meet grid connection requirements win contracts. The regulated distribution utilities then purchase this energy on behalf of their captive consumers.

2026 Auction Highlights

- Long-Term Reserve Capacity Auction (March 2026): 19 GW of firm capacity contracted — the largest reliability-focused procurement in Brazil’s history, expected to mobilise USD 12–13 billion

- First Battery Storage Auction (April 2026): 18 GW of registered projects competing for grid-scale battery storage contracts — the first dedicated storage auction in the country

- ANEEL projects centralized solar will add 4,954 MW in 2026 alone, nearly double the 2,816 MW installed in 2025

Key Solar States for Utility-Scale

| State | Utility-Scale Capacity | Irradiance | Key Advantage |

|---|---|---|---|

| Bahia | ~1,354 MW | 5.8–6.0 kWh/m²/day | Grid access, land availability |

| Piauí | ~1,205 MW | 5.9–6.2 kWh/m²/day | Highest irradiance, low land cost |

| Ceará | ~499 MW | 5.7–6.0 kWh/m²/day | Coastal wind-solar hybrid sites |

| Minas Gerais | ~730 MW | 5.3–5.8 kWh/m²/day | Proximity to demand centers |

Agrivoltaics and Floating Solar

Brazil is emerging as a significant agrivoltaics market. The country’s vast agricultural sector — including sugar cane, soybeans, and citrus operations — is exploring dual-use solar that generates electricity above crops or on irrigation canal covers. The CMS Expert Guide on Agrivoltaics in Brazil notes significant floating solar potential on the country’s hydropower reservoirs, where solar generation can offset water evaporation losses. For more on this topic, see Agrivoltaics Design.

Solar Design Considerations for Brazil

Optimal Orientation

Brazil sits in the Southern Hemisphere — panels should face north (not south as in the northern hemisphere). This is the most common installation error made by designers unfamiliar with the market. The optimal tilt angle equals approximately the site’s latitude:

- Fortaleza (3.7° S): 0–5° tilt

- Recife (8° S): 5–10° tilt

- Salvador (12.9° S): 10–15° tilt

- São Paulo (23.5° S): 18–25° tilt

- Porto Alegre (30° S): 25–32° tilt

Shading Analysis

Brazil’s urban rooftop environment — particularly in São Paulo, Rio de Janeiro, and Belo Horizonte — includes significant shading from adjacent buildings, water tanks, and communication equipment mounted on rooftops. A solar shadow analysis using actual site geometry is not optional in dense urban environments. Sizing a system based on nameplate irradiance without shading losses leads to significant over-projections of generation.

Grid Conditions in Remote Areas

Rural and remote installations face grid reliability challenges. Many agribusinesses and rural properties are turning to hybrid solar-battery-generator systems that reduce dependence on unreliable grid supply. Off-grid solar is economically viable where grid extension costs exceed R$30,000–R$50,000 per property.

String Design and High Temperatures

Brazil’s high ambient temperatures — regularly exceeding 35°C in the Northeast — affect panel performance. Temperature coefficients become especially relevant when comparing panel options: a panel with a -0.30%/°C temperature coefficient performs meaningfully better at 45°C cell temperature than one at -0.45%/°C. Using solar software that applies real temperature data from the installation location produces more accurate generation estimates than default climate assumptions.

Model Your Brazilian Solar Project With Real Local Data

SurgePV uses site-specific irradiance and temperature data for any location in Brazil — including shading analysis, string design, and financial modelling in one platform.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

Challenges and Risks in the Brazilian Solar Market

The TUSD Phase-In Effect

The distribution tariff phase-in under Law 14,300/2022 is the most debated element of Brazil’s solar framework. By 2029, new prosumers will pay the full distribution tariff on exported energy — reducing the credit value compared to the pre-2023 regime. The practical effect is that self-consumption becomes even more important relative to export, and oversized systems lose more of their historical economic advantage.

For installers using solar proposal software in Brazil, frontmatter financial models need to reflect the TUSD trajectory through 2029, not just current tariff conditions.

Grid Connection Delays

Despite ANEEL regulations requiring timely connections, distribution utilities in some regions — particularly in underserved rural areas — continue to miss connection timelines. CEMIG (Minas Gerais), CELPE (Pernambuco), and COELBA (Bahia) have faced criticism for connection backlogs. Installers operating in these regions should build realistic connection timelines into project schedules and inform customers accordingly.

Currency Risk

Solar equipment in Brazil is largely imported and priced in USD. The Brazilian Real (BRL) has experienced significant volatility — a 20% BRL depreciation translates directly into higher equipment costs in reais. Installers quoting in BRL for delivery 60–90 days later face margin risk if the exchange rate moves against them. Hedging or USD-indexed pricing clauses are common in commercial contracts above R$100,000.

Financing Access for Lower-Income Households

Despite BNDES programmes, financing access for low-income residential customers remains limited. Credit analysis requirements and documentation burdens exclude a significant share of the addressable market. Several state governments and NGOs are developing alternative financing models (energy cooperatives, green microfinance), but these remain small-scale in 2026.

The 2030 Outlook

Brazil’s solar trajectory through 2030 is set by three forces: falling costs, rising electricity tariffs, and the structural opening of the free energy market.

| Year | Projected Total PV Capacity | Key Driver |

|---|---|---|

| End-2026 | ~75.87 GW | ACL market opening, continued distributed growth |

| 2027–2028 | ~90–100 GW | Utility-scale auction pipeline, commercial C&I surge |

| 2029 | ~110–120 GW | Full TUSD phase-in reshaping distributed economics |

| 2030 | ~125–130 GW | Pre-tax-reform deadline, ICMS phase-out approaching |

| 2031 | ~140.25 GW | Forecast endpoint (IMARC Research) |

The US Energy Information Administration has described distributed solar as the fastest-growing power source in Brazil by capacity additions — a characterisation that remains accurate in 2026 despite the distributed segment’s short-term moderation.

Battery Storage: The Next Phase

Brazil’s first dedicated battery storage auction in April 2026 signals that the energy storage market is moving from niche to mainstream. The combination of expanding solar capacity and the need for grid stability — particularly as hydro output becomes less predictable due to climate-driven drought cycles — is creating demand for storage at all scales.

ABSOLAR estimates Brazil could see significant residential and commercial battery adoption from 2027 onwards, following the infrastructure created by the 2026 storage auctions and the falling battery cost curve that has halved prices since 2021.

Agro-Energy Integration

Brazil’s agricultural sector — responsible for approximately 25% of GDP — is a major solar growth driver. Rural electrification via solar, irrigation pump automation, cold chain energy supply for perishables, and grain drying applications are all expanding. The BNB’s rural solar financing programmes target this segment explicitly, and BNDES has separate credit lines for Pronaf (family agriculture) solar installations at reduced rates.

Conclusion

- Install now, before 2029: New distributed generation systems still operate under favourable tariff conditions in 2026. Every year toward 2029 adds to the TUSD burden. Systems commissioned in 2026 retain better economics than those commissioned in 2028 or 2029.

- Stack your incentives: BNDES financing at ~3% p.a. combined with ICMS exemptions and Law 14,120 TUSD/TUST reductions can reduce the effective cost of a commercial system by 25–35% compared to fully unsubsidised installation — before any energy savings are counted.

- Model self-consumption, not export: Brazil’s net metering credits are valuable, but the real return comes from displacing high-tariff grid electricity. Design systems around the consumption profile of the site, not around maximum generation capacity.

Frequently Asked Questions

How does net metering work in Brazil?

Brazil’s net metering system is called the Sistema de Compensação de Energia (energy compensation system). Surplus solar electricity exported to the grid generates credits measured in kWh that offset future consumption. Credits remain valid for 60 months. Under Law 14,300/2022, systems below 5 MW qualify for this framework until 2045, but a distribution tariff surcharge is being phased in from 2023 to 2029.

What is Law 14,300/2022 (Marco Legal) for solar in Brazil?

Law 14,300/2022 is the legal framework that governs distributed generation in Brazil. It guarantees net metering participation until 2045 for systems below 5 MW using renewable sources. It also introduced a gradual surcharge on the distribution network fee (TUSD) for prosumers — starting low in 2023 and reaching the full rate by 2029. Systems installed before January 2023 have more favourable grandfathered conditions.

What are the main solar incentives in Brazil in 2026?

Key incentives include: ICMS tax exemptions on solar equipment (available in most states via Convênio ICMS 101/97), TUSD/TUST tariff reductions for qualifying renewable generators under Law 14,120/2021, subsidised BNDES financing at approximately 3% per annum for small-scale installations, and infrastructure debentures for larger projects. ICMS incentives will be phased out as part of Brazil’s broader tax reform from 2030 to 2033.

How much does a solar system cost in Brazil in 2026?

A small residential system (4–5 kWp) costs approximately R$11,000–R$12,500. A system sized for a household consuming 300 kWh/month typically runs R$20,000–R$30,000. Commercial systems range from R$40,000 to R$80,000. The cheapest state by installation cost is Rondônia at R$2.30 per Wp. Payback periods run 3–5 years for residential and 4–7 years for commercial.

What is Brazil’s total installed solar PV capacity in 2026?

Brazil reached 68 GW of total installed PV capacity by early 2026, split between 46 GW of distributed generation and 22.3 GW of centralized utility-scale capacity. Absolar forecasts 10.6 GW of new additions in 2026, with total capacity projected to reach 75.87 GW by year-end and 140.25 GW by 2031.

Which Brazilian states have the most solar capacity?

For distributed solar (rooftop and small systems), the top states are São Paulo (5.8 GW), Minas Gerais (4.9 GW), Paraná (3.7 GW), Rio Grande do Sul (3.4 GW), and Mato Grosso (2.6 GW). For utility-scale solar farms, the Northeast dominates: Bahia, Piauí, and Ceará lead due to their exceptional irradiance of 5.5–6.2 kWh/m²/day.

Can businesses access the free energy market (ACL) in Brazil for solar?

Yes. Brazil’s free energy market (Ambiente de Contratação Livre, or ACL) allows eligible consumers to negotiate energy directly with generators via bilateral contracts registered with CCEE. From August 2026, all low-voltage industrial and commercial customers gain access to this market, making solar PPAs and self-generation arrangements accessible to a far wider range of businesses than before.

What is ANEEL’s role in Brazil’s solar market?

ANEEL (Agência Nacional de Energia Elétrica) is Brazil’s federal electricity regulator. It sets the rules for distributed generation, administers connection requirements, conducts public auctions for utility-scale capacity, and enforces compliance with laws including Law 14,300/2022. ANEEL Ruling No. 1,000/2021 (amended by Ruling No. 1,059/2023) provides the detailed operational framework for net metering and distributed generation connections.