Quick Answer

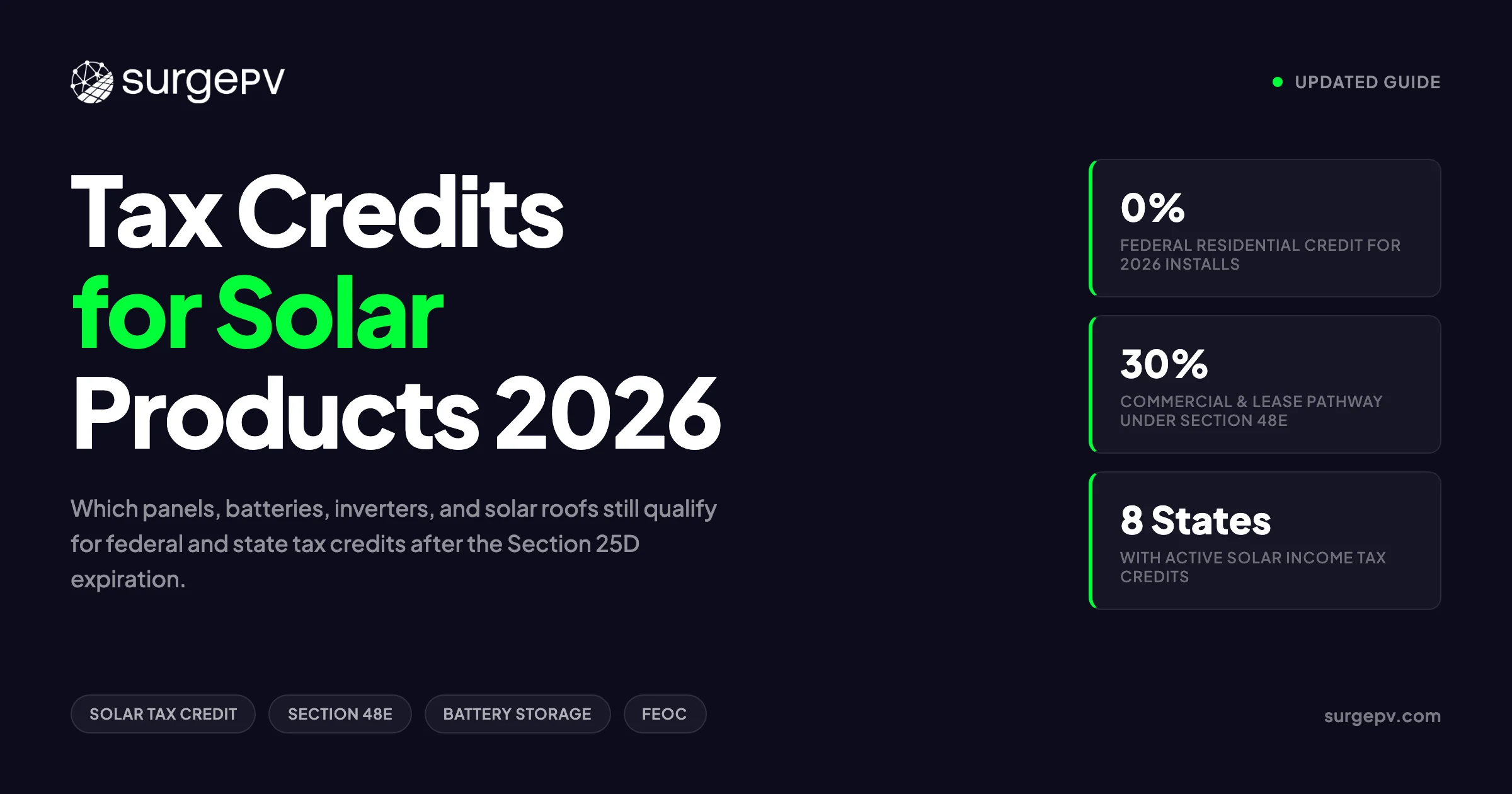

Homeowner-owned solar products installed in 2026 no longer qualify for the federal Section 25D tax credit. Commercial solar products, third-party-owned residential systems like leases and PPAs, and standalone battery storage may still qualify under Section 48E through 2027. State tax credits and rebates remain active in at least eight states.

The 30% federal tax credit shaped solar product purchases for more than a decade. Then it ended. On January 1, 2026, the Residential Clean Energy Credit under Section 25D dropped to zero for homeowner-owned systems. That single change turned every sales conversation about solar products into a compliance conversation first.

Installers now field the same question daily: which solar products still get a tax credit? The honest answer depends on who owns the product, where it is installed, when construction began, and where the components were made. A battery that does not qualify for a homeowner in Texas may qualify for a business in Texas. A solar roof that loses federal credit in one ownership structure keeps it in another.

This guide sorts the products by eligibility. It covers what qualified under the expired residential credit, what still qualifies under commercial and state programs, and which products homeowners routinely mistake for eligible. For installers, solar design software that models incentives accurately is now essential to closing deals in a post-ITC market. For the broader policy picture, see our post on solar tax credit 2026. For state-by-state details, see solar tax credits 2026 country and state guide.

Quick Answer

Homeowner-owned solar products installed in 2026 no longer qualify for the federal Section 25D tax credit. Commercial solar products, third-party-owned residential systems like leases and PPAs, and standalone battery storage may still qualify under Section 48E through 2027. State tax credits and rebates remain active in at least eight states.

In this guide:

- Which solar products qualified under Section 25D before it expired.

- Which products still qualify in 2026 through commercial, lease, and state pathways.

- Products that look eligible but are not, and why.

- How to claim credits, which forms to use, and what documentation to keep.

- How FEOC and domestic content rules change product sourcing in 2026.

- State-level product eligibility examples for batteries, inverters, and solar water heaters.

What Changed in 2026: Section 25D vs Section 48E

The One Big Beautiful Bill Act, signed July 4, 2025, terminated the residential clean energy credit rather than phasing it down. Section 25D now allows no credit for expenditures made after December 31, 2025. An expenditure is treated as made when original installation is completed, not when the contract is signed or the deposit is paid, according to IRS FAQs on the OBBB changes.

Commercial and third-party-owned products took a different path. Section 48E, the Clean Electricity Investment Tax Credit, remains available for projects that begin construction by July 4, 2026, or are placed in service by December 31, 2027. The base rate is 6%, but projects that meet prevailing wage and apprenticeship requirements qualify for 30%. Bonus adders can push the total higher.

| Ownership Path | 2026 Federal Credit | Products Covered | Key Deadline |

|---|---|---|---|

| Homeowner-owned residential | 0% under Section 25D | None for new 2026 installs | Expired December 31, 2025 |

| Third-party-owned residential (lease/PPA) | 30% under Section 48E | Panels, inverters, batteries, racking, labor | Placed in service by December 31, 2027 |

| Commercial / industrial | 30% under Section 48E | Same product set plus standalone storage | Begin construction by July 4, 2026, or placed in service by December 31, 2027 |

| Standalone battery storage | 30% under Section 48E | Batteries 5 kWh or larger for commercial | Construction timeline under Section 48E |

This split matters for product sales. A homeowner who buys panels outright in 2026 gets no federal credit. The same panels, sold through a lease or PPA, can support a 30% credit claimed by the financing entity. That difference often shows up as lower monthly payments rather than a direct tax benefit to the homeowner.

Solar Products That Qualified Under Section 25D (Through 2025)

Section 25D covered “qualified solar electric property,” solar water heating property, fuel cell property, small wind energy property, geothermal heat pump property, and battery storage technology. The credit applied to the product plus eligible installation costs. Used or previously owned property did not qualify.

Solar PV Panels and Modules

Standard crystalline silicon and thin-film panels qualified as long as they were new and used to generate electricity for a U.S. residence. There was no manufacturer restriction, no efficiency minimum, and no cap on the credit. The 30% rate applied to the full installed cost.

Inverters, Power Optimizers, and Microinverters

Inverters counted as part of the solar energy system. String inverters, microinverters, and power optimizers with monitoring hardware were all eligible because they are necessary to convert DC power from panels into usable AC power. Integrated monitoring systems also qualified when part of the original installation.

Racking, Mounting, and Wiring

Racking, mounting hardware, conduit, wiring, and electrical components directly tied to the solar system qualified. The IRS allowed these as part of the onsite preparation and interconnection costs. Structural roof work that merely supported the panels did not qualify.

Battery Storage Technology

Battery storage qualified if it had a capacity of at least 3 kWh and was installed in connection with a residence. Standalone batteries became eligible beginning in 2023. The battery did not need to be charged exclusively by solar, though it had to be installed in connection with the home.

Solar Water Heaters

Solar water heaters qualified if certified by the Solar Rating and Certification Corporation (SRCC) or a comparable state-endorsed entity. At least half the energy used to heat water had to come from the sun. The water had to be used in the dwelling. Solar pool heaters and hot tub heaters did not qualify.

Solar Shingles and Solar Roofing Tiles

Solar shingles and building-integrated photovoltaics qualified because they generate electricity. The IRS specifically distinguished them from traditional roofing materials. Only the solar-generating portion counted. Decking, rafters, and conventional shingles did not.

Geothermal Heat Pumps, Fuel Cells, and Wind Turbines

Geothermal heat pumps that met Energy Star requirements, fuel cells with capacity limits, and small residential wind turbines also qualified under Section 25D. Fuel cells had a special cap of $500 for each half kilowatt of capacity.

Solar Products That Still Qualify for Tax Credits in 2026

The federal residential credit is gone, but several pathways remain. The product list is nearly identical. What changed is the ownership structure and the section of the tax code.

Commercial Solar Products Under Section 48E

Businesses that purchase solar products for commercial, industrial, or utility-scale projects can still claim a 30% credit. Eligible products include:

- Solar PV panels and modules

- Inverters, optimizers, and monitoring systems

- Racking, mounting, and tracking systems

- Wiring, conduit, and switchgear

- Installation labor and sales tax on eligible equipment

- Battery storage systems of 5 kWh or larger, standalone or paired with solar

Projects over 1 MW AC must meet prevailing wage and apprenticeship requirements to receive the 30% rate. Otherwise the base rate is 6%. This distinction makes labor compliance a product-cost issue for large commercial jobs.

Third-Party-Owned Residential Products

Leases, power purchase agreements, and prepaid solar products may still qualify under Section 48E through the end of 2027. The financing company owns the products and claims the credit. Homeowners do not file Form 5695. They receive the benefit indirectly through lower lease payments or PPA rates.

The eligible product set is the same as commercial: panels, inverters, racking, wiring, and batteries. The key difference is scale. Most residential lease systems are under 1 MW AC, so they avoid the prevailing wage complexity that affects large commercial projects.

Standalone Battery Storage

Standalone battery storage has a longer federal runway than solar panels under the OBBB framework. Commercial batteries of 5 kWh or larger can qualify under Section 48(c)(6) and Section 48E. Residential homeowner-owned batteries installed in 2026 do not qualify for Section 25D, but third-party-owned residential batteries may qualify under Section 48E.

This creates a practical opportunity for installers. A homeowner who wants backup power but missed the 2025 solar credit deadline may still benefit from a battery lease or solar-plus-storage PPA where the financier claims the commercial credit.

State Tax Credit Products

At least eight states still offer direct income tax credits for solar products in 2026. State credits are independent of federal law. They often cover the same product categories, but each state has its own forms, caps, and carryforward rules.

| State | Credit | Cap | Products Typically Covered |

|---|---|---|---|

| Hawaii | 35% | $5,000 | PV systems, inverters, batteries, installation |

| New York | 25% | $5,000 | PV equipment and installation |

| South Carolina | 25% | $3,500 per year | PV systems, batteries, labor |

| Arizona | 25% | $1,000 | Solar energy devices |

| Massachusetts | 15% | $1,000 | Solar and storage equipment |

| Iowa | 15% | $5,000 | Solar energy systems |

| Utah | 25% | $1,600 | Renewable energy systems |

| New Mexico | Variable | $6,500 per installation | Solar electric and thermal systems |

Sales tax exemptions and property tax exclusions are even more widespread. Over 25 states exempt solar products from sales tax. Over 35 states exclude the value of solar equipment from property tax assessments. These are not credits, but they reduce the net cost of the same products.

What Solar Products Do Not Qualify: Common Misconceptions

Homeowners and some sales reps assume that anything with a solar label qualifies. That assumption leads to denied credits and angry customers. Here are the products and costs that do not qualify.

Solar Pool Heaters and Hot Tub Heaters

Solar water heaters qualify only when the heated water is used in the dwelling. The IRS explicitly excludes swimming pools and hot tubs. A solar pool heater, no matter how efficient, does not qualify for the federal credit.

Solar Attic Fans

This is a persistent gray area. The solar panel that powers a fan may qualify as solar electric property, but the fan itself is ventilation equipment, not clean energy property. Some manufacturers claim their products are eligible, but IRS guidance has generally treated attic fans as not qualifying. In 2026, with Section 25D expired, the question is largely moot for homeowner-owned systems.

Portable Solar Panels and Solar Chargers

Small portable panels, solar phone chargers, and solar-powered lights do not qualify. They are not permanently installed property used to power a residence. Even large portable solar generators generally do not qualify unless they are integrated into a qualifying system.

Off-Grid Solar Systems for Non-Residence Use

Off-grid solar can qualify if it powers a U.S. residence. A system installed on an RV, boat, or remote cabin that is not a dwelling generally does not qualify for the residential credit. Commercial off-grid systems may have a different path under Section 48E if they serve a business.

Roof Repairs and Structural Work

This is the most expensive misconception. Customers often want to roll a full roof replacement into the solar project and claim the credit. The IRS allows only solar roofing tiles and solar shingles that generate electricity. Traditional shingles, decking, rafters, and structural repairs do not qualify. If a roof must be replaced to support solar, only the solar equipment portion gets credit. The roof replacement is a separate, non-qualifying cost.

Electrical Panel Upgrades

An electrical panel upgrade qualifies only when it is necessary for the solar or battery interconnection and properly documented on the invoice. A standalone panel upgrade unrelated to solar does not qualify. The contractor’s invoice should clearly state that the upgrade is required for solar interconnection.

Used and Pre-Owned Equipment

The credit applies only to new clean energy property. Used panels, refurbished inverters, and secondhand batteries do not qualify. This rule matters for the growing secondary market in solar equipment.

How to Claim: Forms, Deadlines, and Documentation

The claiming process depends on which credit pathway applies. Get the pathway wrong and the credit is denied.

Homeowner Claims for 2025 Installations

If the system was placed in service on or before December 31, 2025, the homeowner claims the credit on IRS Form 5695, Residential Energy Credits. The credit transfers to Schedule 3 and then to Form 1040. Unused credits can be carried forward.

Required documents:

- Itemized final invoice showing eligible products and costs

- Proof of placed-in-service date, usually the interconnection approval or final inspection

- Manufacturer certification statement for the equipment

- Proof of payment

Business Claims Under Section 48E

Businesses claim the credit on Form 3468, Investment Credit. Large projects must also document prevailing wage and apprenticeship compliance. Projects beginning construction in 2026 or later must maintain FEOC and domestic content records.

Required documents:

- Itemized invoices separating eligible solar products from ineligible structural costs

- Certified payroll records for projects over 1 MW AC

- Apprenticeship records

- Supplier chain affidavits tracing component origin

- Continuous construction documentation for safe-harbor claims

State Credit Claims

Each state uses its own form. Most require the final installation invoice, interconnection agreement, and proof of payment. Some states require pre-approval before installation begins. Deadlines usually follow the tax year, but budget-limited programs can close early.

State Solar Tax Credits and Product Eligibility

State programs often define eligible products more narrowly or more broadly than federal law. Installers should read each program’s equipment list before quoting a price.

Hawaii: 35% Credit, $5,000 Cap

Hawaii’s Renewable Energy Technologies Income Tax Credit covers solar water heating and PV systems. The credit is 35% of actual cost or $5,000, whichever is lower. It must be used in the year claimed; carryforward is not allowed. Batteries are typically included if they are part of the PV system.

New York: 25% Credit, $5,000 Cap

New York’s solar equipment tax credit covers solar PV systems installed on residential property. The credit is 25% of qualified costs up to $5,000. It can be carried forward for five years. The program generally covers panels, inverters, racking, and installation.

South Carolina: 25% Credit, 10-Year Carryforward

South Carolina allows a 25% state income tax credit for solar energy systems. The credit is capped at $3,500 per year but can be carried forward for up to 10 years. This makes it valuable for homeowners with limited annual tax liability. Eligible products include PV systems and battery storage.

Massachusetts: 15% Credit, $1,000 Cap

Massachusetts offers a 15% credit up to $1,000 for solar and wind energy systems. The program also interacts with the SMART program, which provides performance-based incentives for solar and storage. Battery adders can significantly improve project economics.

California: No State Tax Credit, But Product Rebates

California does not offer a state income tax credit, but the Self-Generation Incentive Program (SGIP) provides rebates for battery storage. Equity resiliency incentives can reach $1,000 or more per kWh. These rebates reduce the cost basis for any remaining federal calculations.

FEOC and Domestic Content: New 2026 Rules

Two new compliance layers affect which solar products can support a federal credit in 2026. They sound similar but work differently.

Foreign Entity of Concern Rules

FEOC restrictions took effect January 1, 2026. Projects beginning construction after December 31, 2025, must show that a minimum percentage of manufactured product costs come from non-FEOC sources. Covered entities include those with ties to China, Russia, Iran, and North Korea.

| Year | Solar Facility Non-FEOC Threshold | Battery Storage Non-FEOC Threshold |

|---|---|---|

| 2026 | 40% | 55% |

| 2027 | 45% | 60% |

| 2028 | 50% | 65% |

| 2029 | 55% | 70% |

| 2030+ | 60% | 75% |

Failing the FEOC threshold can disqualify the entire credit. This makes component sourcing a credit decision, not just a procurement decision. A U.S.-assembled module using Chinese cells may still count as FEOC-sourced because ownership and control matter more than assembly location.

Domestic Content Bonus

The domestic content bonus adds 10% to the ITC for projects that meet U.S. manufacturing thresholds. For 2026 construction starts, at least 50% of manufactured products must be U.S.-made, and all steel and iron must be U.S.-produced. Missing this threshold only forfeits the 10% bonus, not the base 30% credit.

The practical impact is that product choice now carries tax risk. An installer who specifies the cheapest panels without checking origin may save a few cents per watt but lose 10% or more of the tax credit. Solar proposal software that flags domestic content assumptions helps avoid this mistake.

Model Solar Incentives Accurately in Every Proposal

Tax credit rules change fast. SurgePV’s financial modeling lets you apply the correct federal, state, and utility incentives to each project so your customer sees real net cost and payback.

Explore Financial ModelingNo commitment required · 20 minutes · Live project walkthrough

Conclusion

The era of one-size-fits-all federal solar product credits ended on December 31, 2025. In 2026, product eligibility depends on ownership structure, project type, construction timing, and component origin.

- Homeowner-owned residential products installed in 2026 get no federal Section 25D credit.

- Commercial products and third-party-owned residential systems can still qualify for 30% under Section 48E through 2027.

- State tax credits and rebates remain active in at least eight states and can cover panels, batteries, inverters, and installation.

- FEOC and domestic content rules now make product sourcing a core part of credit compliance.

Before you sell any solar product in 2026, confirm the credit pathway, verify the product list, and document every component origin. The customers who trust you to get this right are the ones who will refer their neighbors.

Frequently Asked Questions

Do solar products still qualify for federal tax credits in 2026?

Homeowner-owned residential solar products no longer qualify for the federal Section 25D credit after December 31, 2025. Commercial solar products, third-party-owned residential systems like leases and PPAs, and standalone battery storage may still qualify under Section 48E through 2027. State tax credits and rebates remain available in many states.

Which solar products qualify for the federal tax credit?

When the credit was active, eligible products included solar PV panels, inverters, racking, wiring, battery storage of 3 kWh or more, solar water heaters, solar shingles, geothermal heat pumps, fuel cells, and residential wind turbines. Solar attic fans, solar pool heaters, portable solar chargers, and standalone generators generally did not qualify.

Can I claim a tax credit for a solar battery in 2026?

A homeowner-owned battery installed in 2026 does not qualify for the expired Section 25D residential credit. Batteries paired with commercial projects or third-party-owned residential systems may qualify under Section 48E. Some state programs, such as California SGIP, New Jersey storage incentives, and Massachusetts SMART, still offer battery rebates or credits.

Do solar shingles and solar roofs qualify for tax credits?

Solar shingles and building-integrated photovoltaics qualified under Section 25D when the credit was active, because they generate electricity. Traditional roofing materials that only serve a structural function did not qualify. For 2026 installations, only commercial or third-party-owned solar roofs may qualify under Section 48E.

What solar products do not qualify for tax credits?

Products that do not qualify include solar pool heaters, solar ovens, portable solar chargers, solar attic fans in most interpretations, traditional roof repairs or replacements, tree removal, electrical panel upgrades not required for solar interconnection, used equipment, and standalone generators not charged by solar.

How do I claim a solar tax credit in 2026?

For systems placed in service by December 31, 2025, homeowners file IRS Form 5695 with their federal tax return. For 2026 commercial or third-party-owned systems, the business or financier claims Section 48E. State credits require state-specific forms, usually filed with the annual state income tax return. Keep itemized invoices, interconnection agreements, and proof of placed-in-service date.

What is the difference between Section 25D and Section 48E?

Section 25D was the residential clean energy credit claimed directly by homeowners. It expired December 31, 2025. Section 48E is the commercial clean electricity investment tax credit. It offers 30% for eligible commercial projects and third-party-owned residential systems through 2027, with bonuses for domestic content, energy communities, and low-income communities.

What are FEOC rules for solar tax credits in 2026?

Foreign Entity of Concern rules took effect January 1, 2026. Solar projects beginning construction in 2026 must show at least 40% of manufactured product costs come from non-FEOC sources. Battery storage must show 55% non-FEOC content. These thresholds rise annually. FEOC violations can disqualify the entire credit, unlike domestic content bonus shortfalls, which only forfeit the 10% adder.