Quick Answer

Wood Mackenzie forecasts a 40% spike to $0.84 per watt in 2026 (Wood Mackenzie, 2026). Soft costs now eat about 50% of every residential system price (NREL, 2024). Reps who deliver a tailored quote during the first visit close 15–25 percentage points higher than reps who delay. The FTC documented a pattern of misleading 'free solar' ads and high-pressure tactics (FTC, 2024).

The residential solar market is getting harder to close. Customer acquisition costs hit $0.60 per watt in 2025. Wood Mackenzie forecasts a 40% spike to $0.84 per watt in 2026 (Wood Mackenzie, 2026). Soft costs now eat about 50% of every residential system price (NREL, 2024). Reps cannot afford to burn leads with the wrong pitch.

Wood Mackenzie forecasts a 40% spike to $0.84 per watt in 2026 (Wood Mackenzie, 2026). Soft costs now eat about 50% of every residential system price (NREL, 2024). Reps who deliver a tailored quote during the first visit close 15–25 percentage points higher than reps who delay.

Most sales training tells reps what to say. It rarely tells them who to say it to. A lease pitch to a cash-ready empty nester wastes everyone’s time. A loan pitch to a credit-challenged renter kills the deal before the first objection.

This guide gives you a profile-matched pitch system. You will learn which financing option to lead with for five common homeowner types. You will get four proven pitch frameworks with scripts. You will see the five objections that specifically kill lease-vs-purchase decisions. And you will learn how to handle them. You will also understand why on-site proposals matter. Reps who deliver a tailored quote during the first visit close 15–25 percentage points higher than reps who delay.

TL;DR — Solar Lease vs Purchase Pitch

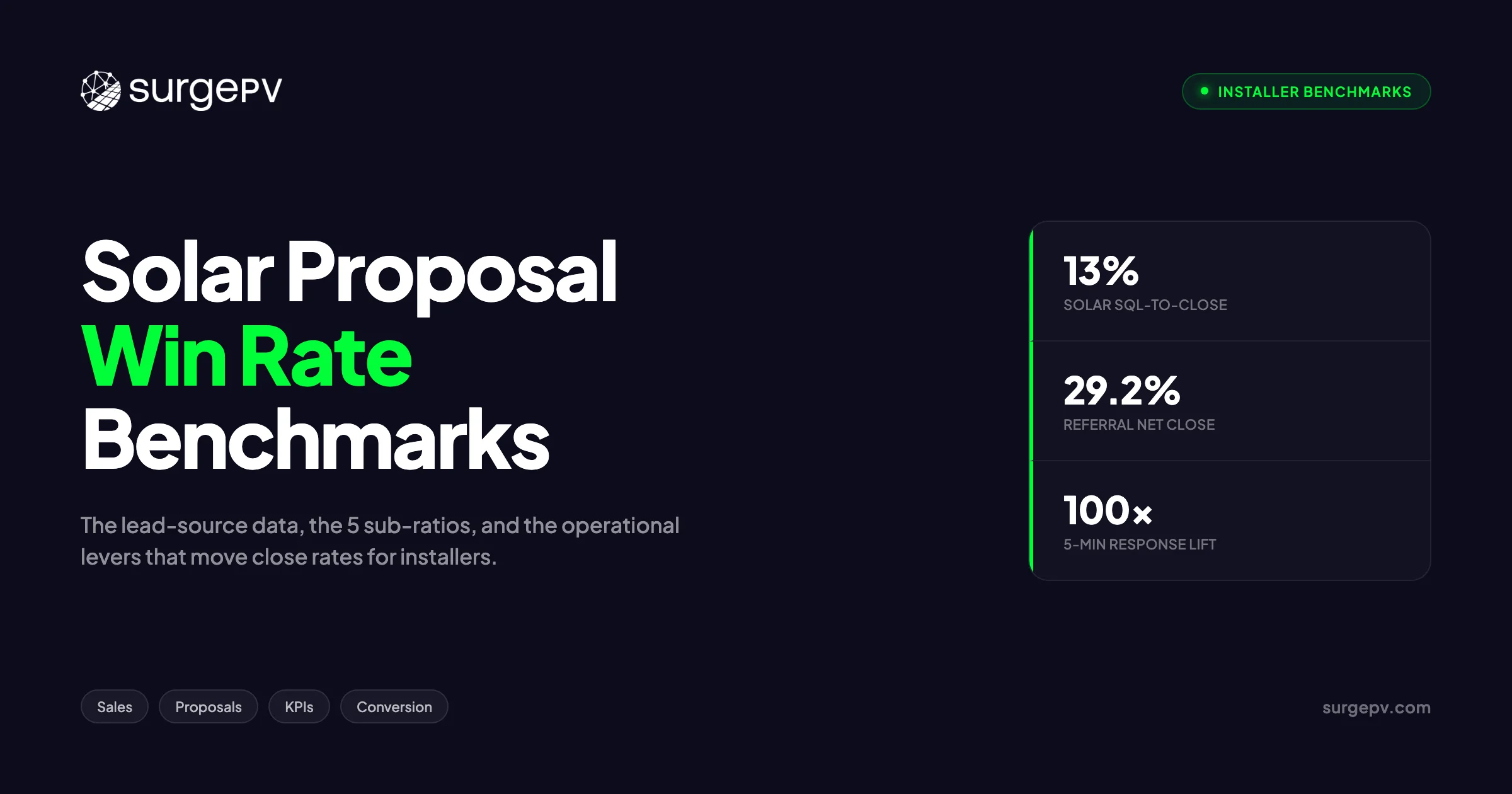

Reps who profile-match their pitch and deliver an interactive proposal during the first visit close 15–25 points higher than reps who delay quoting. The average solar SQL-to-close rate is 13% (First Page Sage, 2025). Top-quartile installers now turn around proposals in under 24 hours.

In this guide:

- The Rep’s Dilemma: Lease vs Purchase in 2026

- Close Rates by Financing Type: What the Data Says

- The 5 Homeowner Archetypes and Their Matched Pitch

- Four Proven Pitch Frameworks (with Scripts)

- The 5 Objections That Kill Lease-vs-Purchase Deals

- Speed-to-Proposal: The 15-Point Close-Rate Lift

The Rep’s Dilemma: Lease vs Purchase in 2026

Reps face a tougher financing market in 2026. The residential ITC expired at the end of 2025. Third-party-owned systems still access Section 48E credits. This flips the economics. Leases and PPAs now carry a tax advantage that cash and loans lack. Reps must explain this clearly without sounding like finance lawyers. Read Solar PPA Negotiation Guide for a complete walkthrough.

The bigger problem is trust. Connecticut’s Attorney General sued Sunrun and two dealers in July 2024 for forged signatures, impersonation on verification calls, and hidden escalator clauses (Connecticut Office of the Attorney General, 2024). The FTC documented a pattern of misleading “free solar” ads and high-pressure tactics (FTC, 2024). Sunrun holds a 2 out of 5 star rating on EnergySage, with recurring complaints about over-promised savings and undersized systems (EnergySage, 2025).

Homeowners are skeptical before the rep knocks. The rep who leads with a generic pitch walks into a wall of distrust. The rep who leads with a tailored comparison builds credibility in the first 90 seconds. Read more about Agricultural Solar Case Study. For the latest details on France, see Floating Solar Farms France.

What changed in 2026. The residential ITC sunset means homeowner-owned systems no longer qualify for the 30% federal credit. Commercial and third-party-owned systems can still access Section 48E credits. This makes leases and PPAs relatively more attractive than before. But it also adds complexity. Reps must explain why a lease might make sense without implying that ownership is now a bad deal.

The core principle. Match the financing recommendation to the homeowner’s credit profile, debt-to-income ratio, homeownership horizon, and tax appetite. Never lead with the product you prefer. Lead with the product the homeowner qualifies for and will benefit from.

The SEIA Solar Business Code requires standardized disclosure forms for leases and PPAs (SEIA, 2016). Use them. Transparency is no longer optional. It is a competitive advantage.

Close Rates by Financing Type: What the Data Says

Financing type alone does not determine close rates. Proposal speed, follow-up discipline, and profile matching matter more. But the financing option shapes the sales cycle, objection profile, and qualification bar. Cash closes fastest. Loans need credit checks. Leases cast the widest net but carry the highest objections.

Cash purchases close fastest when the homeowner has the capital. The objection is simple: “Is this worth it?” The answer is usually yes. A cash system pays back in 7–10 years and then produces free power for 15+ years. Cash buyers who are ready to buy often close in one or two visits.

Solar loans require credit qualification. The average solar SQL-to-close rate across all financing types is 13% (First Page Sage, 2025). Loan customers add a layer of underwriting complexity. But they keep ownership and can still use some state-level incentives. Loan pitches work best for homeowners with credit scores above 650 and stable debt-to-income ratios.

Leases and PPAs cast the widest net. They require little or no credit. They offer predictable monthly payments. But they also carry the highest objection load: escalator clauses, transfer fees, lack of ownership, and no tax benefits. Close rates vary widely based on rep skill and proposal clarity. Top reps close lease deals at rates near loan deals. Average reps struggle more with lease objections.

Referral leads convert at about 25–33% regardless of financing type (Focus Digital, 2025; Sunvoy / Ipsun Solar, 2022). This shows that trust, not product, is the main driver. The rep’s job is to build that trust fast. For a direct comparison, see Arka 360 vs SurgePV.

| Financing Type | Close Rate Trend | Sales Cycle | Main Objection |

|---|---|---|---|

| Cash purchase | Fastest | 7–14 days | Upfront cost |

| Solar loan | Moderate | 14–30 days | Credit qualification |

| Lease / PPA | Widest variance | 14–45 days | Escalator, ownership loss |

The data is clear. Speed and trust beat product arguments. A fast, transparent proposal for the right financing option outperforms a perfect pitch for the wrong one.

The 5 Homeowner Archetypes and Their Matched Pitch

Generic pitches fail because homeowners are not generic. Here are five archetypes we see in the field. Each gets a primary recommendation and a backup option. Match the pitch to the homeowner’s credit, timeline, and goals. Never lead with the product you prefer. Lead with what fits their life.

1. The Cash-Heavy Empty Nester

Homeowner profile: 55–70 years old, owns home outright, high savings, plans to stay 15+ years, pays high marginal tax rates.

Primary pitch: Cash purchase. Lead with 25-year savings. Show payback in 7–10 years. Emphasize home value increase and full control.

Backup pitch: If they resist tying up capital, offer a short-term solar loan with aggressive paydown.

Objection to expect: “I’ll be dead before it pays back.” Rebuttal: “Your home value rises today. Your heirs get a paid-off asset, not a bill.”

2. The Credit-Conscious First-Timer

Homeowner profile: 28–40 years old, first home, limited savings, credit score 600–680, worried about debt.

Primary pitch: Lease or PPA. Lead with zero-down and predictable payments. Do not discuss ownership unless they ask.

Backup pitch: If their credit clears 650, introduce a zero-down solar loan. Show how the monthly loan payment compares to the lease escalator.

Objection to expect: “What if I want to sell in 5 years?” Rebuttal: “The lease transfers to the buyer. Here is the transfer process in writing.”

3. The 5-Year Plan Relocator

Homeowner profile: 35–50 years old, job involves relocation, plans to sell within 5–7 years, moderate savings.

Primary pitch: Avoid leases. The transfer friction is too high. Recommend a cash purchase if capital allows, or a loan with no prepayment penalty.

Backup pitch: If cash is tight, a short-term loan with a buyout schedule aligned to their move date.

Objection to expect: “I won’t be here long enough to benefit.” Rebuttal: “Owned systems add appraised value and sell faster. Leased systems complicate closing.”

4. The Battery-First Prepper

Homeowner profile: 40–60 years old, motivated by resilience and backup power, owns home, solid credit, watches utility rates closely.

Primary pitch: Loan or cash purchase with battery. Sunrun attached batteries to 69% of new systems in Q1 2025 (Sunrun Q1 2025 Earnings, via Utility Dive, 2025). Ownership lets them control the battery dispatch and future upgrades.

Backup pitch: If they cannot qualify for a loan large enough, a lease with battery add-on. But warn them about equipment lock-in.

Objection to expect: “What if the battery tech improves?” Rebuttal: “Owners can upgrade. Lease customers are locked to the lessor’s equipment schedule.”

5. The ESG-Driven Professional

Homeowner profile: 30–50 years old, high income, environmentally motivated, reads reviews, asks detailed questions.

Primary pitch: Cash or loan purchase. They want to own their impact. Lead with carbon math and system performance guarantees.

Backup pitch: If they have no tax appetite, a PPA still reduces their carbon footprint without capital outlay.

Objection to expect: “Are solar leases ethical given the complaints?” Rebuttal: “Transparency is the fix. Here is every term, every escalator, every fee—in writing.”

Pro Tip

Never guess the archetype. Ask three questions in the first 5 minutes: How long have you lived here? What is your main goal—savings, backup power, or environmental impact? Have you looked at financing options before? The answers tell you which pitch to open with.

Four Proven Pitch Frameworks (with Scripts)

These four frameworks work across archetypes. Adapt the details to the profile. The rent-vs-own analogy builds on homeownership psychology. The net metering pitch anchors on utility rate pain. The high-rate-plan reframe lowers commitment fear. The Sandler Pain Funnel surfaces objections before you present a solution.

Framework 1: The Rent-vs-Own Analogy

This is the classic close from top solar closer Dev Dayalal, who has closed over $10 million in solar contracts (D2D Experts, 2026). He draws a hand-written side-by-side comparison. Then he asks: Read more about France Solar Feed-in Tariffs.

“Imagine if 17 years ago, when you bought this home, someone had offered you the option to rent it for $1,000 a month or own it for $1,300 a month. What would you have chosen?”

The homeowner almost always says “own.” The rep then maps that logic to solar. Renting power from the utility is like renting the home. Leasing panels is like renting the system. Owning the system is like owning the home. The analogy works because it reframes the decision from “solar or no solar” to “rent or own.”

Use this for: Cash-heavy empty nesters and ESG-driven professionals. Avoid it for credit-challenged first-timers who genuinely cannot afford ownership.

Framework 2: The Net Metering Pitch

Lead with the utility rate. Show the historical increase. Then introduce net metering as a hedge.

“Your utility rate has risen 4% per year for the past decade. At that pace, your bill doubles in 18 years. Net metering lets you sell excess power back to the grid at retail rates. A purchased system locks in your generation cost. A leased system locks in a predictable payment that rises 2.9% per year. Both beat the utility curve. Which fits your budget better?”

Use this for: Battery-first preppers and rate-sensitive homeowners. It works because it anchors the conversation on a known pain point—the utility bill.

Framework 3: The High-Rate-Plan vs Low-Rate-Plan Pitch

This reframes the solar payment as a better utility plan. Instead of “buy solar,” the rep says “switch to a lower-rate energy plan.”

“Right now you are on the utility’s highest-rate plan. They can raise it anytime. I am offering you a fixed-rate energy plan with a 25-year price lock. Plan A is zero down and $120 per month. Plan B is $15,000 upfront and $0 per month. Which plan sounds closer to what you need?”

Use this for: First-time buyers and homeowners who shut down when they hear “loan” or “lease.” The word “plan” feels lower-commitment.

Framework 4: The Sandler Pain Funnel

Sandler Training teaches reps to dig before they pitch (Sandler, via AlphaRun, 2026). The sequence is:

- What are you spending on power?

- What does that mean for your monthly budget?

- What happens if rates keep rising?

- What have you tried before?

- Why didn’t that work?

Only after the fifth question does the rep present a solution. This prevents “presenting before validating pain.” It also surfaces the real objection early.

Use this for: Skeptical homeowners and ESG-driven professionals who want to feel heard. Do not use it for homeowners who are ready to buy and just need paperwork.

Stop losing deals to slow quoting

Reps who generate proposals on-site close 15–25 points higher. See how solar proposal software cuts quote time from days to minutes.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

The 5 Objections That Kill Lease-vs-Purchase Deals

These five objections come up in almost every lease-vs-purchase conversation. Handle them with data, not defensiveness. Show the escalator chart. Explain the tax credit flow. Map the resale impact. When homeowners see the numbers themselves, trust replaces skepticism. Data beats debate every time.

Objection 1: “The lease payment goes up every year.”

This is the escalator clause objection. Most leases include a 2.9% annual escalator (Solar.com, 2026). U.S. utility rates rose an average of 2.85% per year over the past 25 years (SolarReviews, citing EIA, 2024). The rep’s job is to show the crossover point.

Response: “Yes, the lease payment rises 2.9% per year. The utility rate has risen about 3% per year for the past two decades. Here is a 20-year chart of both. The lease stays below the utility curve until year 18. After that, the gap widens. If you plan to stay longer than 15 years, ownership saves more. If you plan to move sooner, the lease gives you predictable savings now.”

Use solar design software with built-in financial modeling to generate this chart live. Homeowners believe what they see, not what they hear.

Objection 2: “I heard solar leases make it hard to sell the house.”

This is true in many cases. A 2024 analysis found that leased systems complicate mortgage underwriting because the lease is a debt obligation (WattBuild, 2025).

Response: “A leased system adds a monthly obligation that buyers must assume. An owned system adds appraised value. If you plan to sell in the next 5 years, I recommend ownership or a loan with no prepayment penalty. If you plan to stay long-term, the lease transfer is manageable—and we handle the paperwork.”

Objection 3: “Don’t I lose the tax credit with a lease?”

Yes. The lessor claims any available credits. Since the residential ITC expired in 2025, this now applies to new lease and PPA structures under Section 48E.

Response: “The financing company claims the commercial tax credit. They use it to lower your monthly rate. You do not file for it or wait for it. The trade-off is simple: you give up the credit in exchange for zero upfront cost and no maintenance responsibility. If you have the cash and the tax appetite, ownership keeps the credit with you. If not, the lease captures it indirectly through a lower payment.” For more on this topic, see Solar Operations and Maintenance.

Objection 4: “What if the panels break? Who fixes them?”

This is the maintenance myth. Modern panels rarely fail. But lease customers get a performance guarantee. Owners are responsible unless they buy a service plan.

Response: “With a lease, the company monitors and maintains the system. If output drops below the guarantee, they fix it at no cost. With ownership, you monitor it yourself. Most owners add a $10–15 per month service plan for peace of mind. Either way, panel failure is rare. The real question is who you want calling the shots if something does happen.”

Objection 5: “I need to think about it.”

This is not really a financing objection. It is a trust or information gap. The Sandler method teaches reps to reverse the question. Ask what specifically the homeowner needs to think about. This isolates the real objection.

Response: “Of course. To help me get you the right information, what is the one piece you are unsure about—the payment, the equipment, or the timeline?” This isolates the real objection. If they say “payment,” toggle the proposal from lease to loan to cash on the spot. If they say “equipment,” pull up the panel spec sheet. If they say “timeline,” show the install schedule.

The rep who can answer on-site beats the rep who promises an email tomorrow.

Speed-to-Proposal: The 15-Point Close-Rate Lift

Reps who deliver a proposal during the first visit close 15–25 percentage points higher than reps who delay. Momentum dies after the rep leaves. Competitors call. Spouses talk. Doubt creeps in. Fast proposals with interactive financing toggles let homeowners choose instead of feeling sold.

Reps who deliver a proposal during the first visit close 15–25 percentage points higher than reps who delay (SurgePV, citing SEIA and platform studies, 2025). The reason is simple. Momentum dies after the rep leaves. Competitors call. Spouses talk. Doubt creeps in.

Top-quartile installers now turn around proposals in under 24 hours (SurgePV, 2025). The typical residential sales cycle runs 30–60 days from first inquiry to signed contract (SolarVis, 2024). That gap is pure profit.

The on-site workflow.

- Satellite imagery pre-loads the roof layout before you arrive.

- A 10-minute site assessment confirms obstructions and electrical capacity.

- The solar design tool generates a 2D/3D layout with panel placement.

- The generation and financial tool models yield, ROI, and payback for cash, loan, and lease.

- The solar proposal software produces a client-facing document with toggles between financing options.

- The homeowner sees real-time savings as they switch between lease, loan, and cash.

This is not future tech. This is what solar software does today.

Follow-up discipline matters too. In B2B sales generally, 48% of reps never make a single follow-up attempt (ProfitOutreach, 2026). Ninety-two percent quit after four tries (SpotIO, citing Close.com, 2026). Yet 80% of deals need five or more follow-ups to close (GrowthList, via SpotIO, 2026).

The fix is automated nurture. When a rep leaves a proposal, the system should trigger a sequence: day 1 FAQ email, day 3 financing comparison video, day 7 testimonial from a similar homeowner, day 14 final call reminder. The rep should not have to remember. The solar proposal tool should handle it.

Interactive proposals beat static PDFs. Installers who use interactive proposals commonly see a 15–25 percentage point lift in sign rates versus static PDFs (SurgePV, citing SEIA and platform studies, 2025). The reason is control. When the homeowner toggles between lease and loan themselves, they feel ownership of the decision. They are not being sold. They are choosing.

Clara AI as the co-pilot. Clara AI can surface the right comparison chart, generate the rent-vs-own analogy, or pull up local net metering rates in real time. It does not replace the rep. It makes the rep faster and more accurate.

The rep who combines profile-matched pitching with on-site proposal delivery is no longer just a salesperson. They are a solar consultant. Consultants close more deals because they build trust first and sell second.

Conclusion

The playbook is simple. Profile before pitch. Propose on-site. Handle objections with data. Ask three qualification questions in the first five minutes. Use software to generate tailored quotes during the first visit. Every day of delay costs you deals. Speed and trust are your real products.

- Profile before pitch. Ask three qualification questions in the first 5 minutes. Match the financing recommendation to the homeowner’s credit, timeline, and goals.

- Propose on-site. Use solar design software and solar proposal generator to generate a tailored quote during the first visit. Every day of delay costs you 15–25 points of close rate.

- Handle objections with data, not defensiveness. Show the escalator chart. Explain the tax credit flow. Map the resale impact. When homeowners see the numbers themselves, trust replaces skepticism.

Your next step: audit your current quote turnaround time. If it is over 24 hours, you are losing deals. Book a demo and see how top-quartile teams quote in under 24 hours.

Frequently Asked Questions

Is it better to lease or buy solar panels?

It depends on the homeowner’s credit score, tax appetite, and how long they plan to stay. Cash purchase gives the highest lifetime savings. Loans work for owners with good credit who want to keep tax benefits. Leases and PPAs fit buyers with lower credit or no upfront budget, but they lose ownership and tax incentives.

Do you save more money leasing vs buying solar?

Buying saves more over 25 years in almost every scenario. A purchased system typically pays for itself in 7–10 years and then produces free power. Lease payments include an escalator clause, so costs rise 2.9% annually and never drop to zero.

Can you get tax credits with a solar lease?

No. The lessor—not the homeowner—claims any available tax credits. For leases and PPAs signed after 2025, the residential ITC is no longer available to the homeowner. The financing company captures that value and may or may not pass it through as a lower monthly rate.

Does leasing solar panels affect home resale value?

Yes, and often negatively. Buyers must assume the lease or the seller must buy it out. A 2024 study found that leased systems can complicate mortgage underwriting. Owned systems add appraised value; leased systems add a contractual obligation.

What is the downside of leasing solar?

The main downsides are the escalator clause, lack of ownership, no tax credits, and transfer complications at sale. Homeowners also have no control over equipment upgrades or system size adjustments. If the lease payment rises faster than utility rates, savings can disappear.