Quick Answer

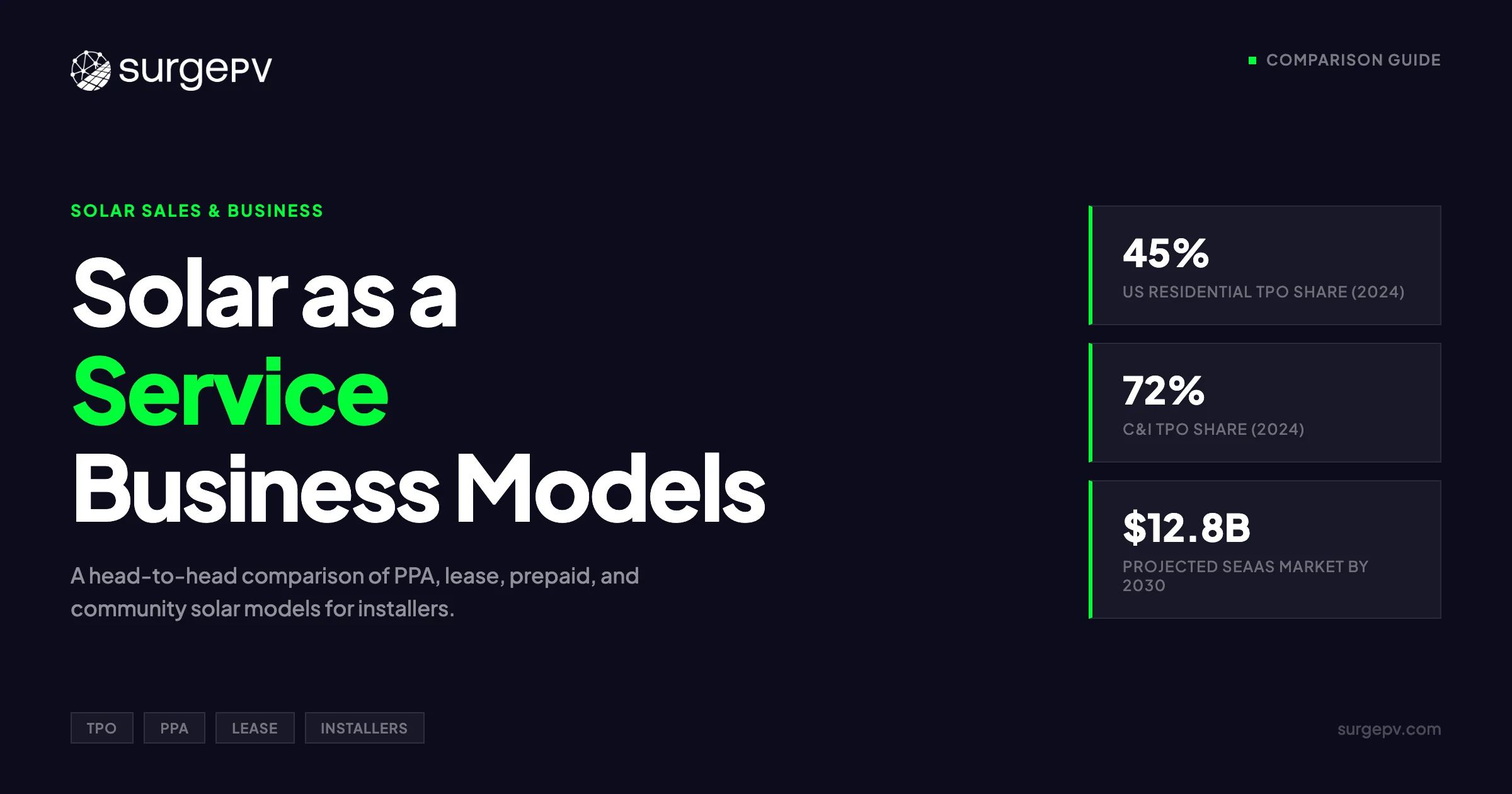

Third-party ownership — solar as a service — is where the sale gets complicated. TPO financing powered 45% of US residential solar in 2024 and 72% of non-residential capacity, per Wood Mackenzie. After the residential ITC expired on Dec 31, 2025, more than 50% of H1 2025 residential sales used third-party ownership, per SEIA.

Most solar installers can quote a cash sale in their sleep. Loans are harder, but still manageable. Third-party ownership — solar as a service — is where the sale gets complicated. The customer asks about ownership, escalators, buyout clauses, and roof warranties. The installer must answer without controlling the contract terms.

Third-party ownership — solar as a service — is where the sale gets complicated. TPO financing powered 45% of US residential solar in 2024 and 72% of non-residential capacity, per Wood Mackenzie. After the residential ITC expired on Dec 31, 2025, more than 50% of H1 2025 residential sales used third-party ownership, per SEIA.

TPO financing powered 45% of US residential solar in 2024 and 72% of non-residential capacity, per Wood Mackenzie. After the residential ITC expired on Dec 31, 2025, more than 50% of H1 2025 residential sales used third-party ownership, per SEIA. The shift is structural, not cyclical. Homeowners still want solar. They just cannot access the federal tax credit directly anymore. TPO providers can.

This guide breaks down 6 solar as a service models, shows how installer economics differ by sale type, and gives you a scoring framework to vet TPO partners. Whether you sell residential, C&I, or both, the model you push affects your margin, your cash flow, and your callback risk.

TL;DR — Solar as a Service 2026

TPO financing powered 45% of US residential solar in 2024 and 72% of non-residential capacity, per Wood Mackenzie. After the residential ITC expired on Dec 31, 2025, more than 50% of H1 2025 residential sales used third-party ownership, per SEIA. This guide breaks down 6 solar as a service models and gives installers a provider vetting framework.

In this guide:

- How 6 TPO models differ in payment structure, ownership, and risk

- Exact revenue and margin gaps between cash, loan, and TPO sales

- A 10-question scoring matrix to vet TPO partners

- Why C&I TPO economics differ from residential

- How battery attachments change PPA and lease math

- State-by-state availability for each model

- FEOC compliance rules that affect equipment procurement

What Is Solar as a Service?

Solar as a service means a third party owns the system, the customer pays for electricity or a fixed fee, and the installer handles construction. Three parties share one roof. Two contracts govern the deal. The provider keeps ownership. The customer keeps savings.

Third-party ownership — TPO — covers solar leases, power purchase agreements, and their variants. The provider funds the system, claims tax credits, handles maintenance, and collects monthly payments. The host customer gets lower bills without an upfront check. The installer gets a build contract without financing the project.

TPO is not the same as a loan. With a loan, the customer owns the panels from day one. They claim the credit. They carry the debt. With TPO, ownership stays with the provider. The customer gets a bill, not an asset.

| Factor | TPO (Lease or PPA) | Customer-Owned (Cash or Loan) |

|---|---|---|

| Upfront cost | $0 or minimal | Full system price or loan down payment |

| Monthly payment | Fixed lease fee or per-kWh PPA rate | Loan payment (if financed) or $0 (if cash) |

| Tax credit owner | TPO provider | Customer |

| Maintenance responsibility | TPO provider | Customer |

| System ownership | TPO provider | Customer |

| Property value impact | Neutral or negative per NREL | Positive per Lawrence Berkeley Lab |

| Contract term | 10-25 years | None (cash) or 5-25 years (loan) |

| Buyout option | Usually at year 5-7 or end of term | N/A — already owned |

The US solar as a service market grew from $4.2 billion to $12.8 billion between 2020 and 2024. That growth came from falling module prices, rising electricity rates, and the residential ITC making TPO economics attractive for providers. Now that the residential credit has expired, the models are adjusting. Providers are shifting toward commercial 48E credits, adding storage to improve savings, and tightening equipment sourcing rules to meet domestic content thresholds.

Mini-FAQ: Does TPO save more than ownership?

Not always. Over 25 years, a cash-owned system typically delivers the highest lifetime savings. TPO wins on lower risk and zero upfront cost. The best model depends on the customer’s tax appetite, credit score, and planned length of stay.

TPO sales require a different pitch. The customer is not buying hardware. They are subscribing to a service. Your solar proposal software should model cash, loan, and TPO side-by-side so the customer sees the trade-offs in one view.

How TPO Models Work: The 6 Financing Structures

The six models below cover every major TPO structure active in the US market in 2026. Each has a distinct payment mechanism, ownership timeline, and customer risk profile. Picking the right model for each customer is the difference between a signed contract and a lost lead.

| Model | Payment Type | Term | Best For |

|---|---|---|---|

| Solar PPA | Per kWh produced | 15-25 years | Homeowners with stable usage |

| Solar Lease | Fixed monthly fee | 10-25 years | Budget-conscious homeowners |

| Prepaid Lease / PPA | Lump sum upfront | 15-25 years | Customers with cash who want simplicity |

| Community Solar | Bill credit subscription | Ongoing | Renters, shaded properties |

| Solar Subscription | Flexible monthly or annual | Month-to-month or 1-5 years | Low-commitment prospects |

| VPP Participation | Revenue share from battery dispatch | Contract tied to VPP program | Battery-equipped homes in active markets |

Solar PPA

A solar power purchase agreement charges per kilowatt-hour produced. Typical rates run $0.08–$0.15 per kWh. The term spans 15-25 years. The provider monitors production and bills monthly. If the system underperforms, the customer’s bill drops — but so does their savings.

PPAs work best in markets with high utility rates and strong sun. The escalator clause matters. A 2.9% annual escalator can turn a 15% savings rate into a net loss by year 15. Always model the escalator across the full contract term.

Solar Lease

A solar lease charges a fixed monthly fee regardless of output. Residential leases run $50–$250 per month depending on system size. Terms stretch 10-25 years. Most include an annual escalator of 1-3%.

The fixed payment is simpler for customers to budget. The downside: if production drops due to shading or equipment failure, the customer pays the same. The provider handles repairs, but the customer has no production guarantee in most contracts. For more on this topic, see [Solar Shading Analysis Guide](/blog/solar-shading-analysis-guide).

Prepaid Lease and Prepaid PPA

A prepaid lease or prepaid PPA requires a lump sum upfront — usually 15-30% of system cost. Ownership transfers to the customer after 5-6 years. The customer gets lower lifetime cost than a standard lease and avoids long-term escalators.

This model suits customers with cash who do not want to deal with tax credit paperwork. The provider monetizes the credit and sells the customer a discounted service. Installers should verify transfer terms carefully. Some contracts include hidden fees at ownership transfer.

Community Solar

Community solar is off-site subscription. Customers sign up for a share of a larger array. They receive bill credits on their utility bill. No panels go on their roof. Read Community Solar Business Model for a complete walkthrough.

This model works for renters, shaded properties, and condos. Availability is limited to states with enabling legislation. As of 2026, 24 states have active community solar programs. Subscription terms vary: some are fixed discounts, others float with market rates.

Solar Subscription

A solar subscription is a flexible-term service. Customers pay monthly or annually with no long-term contract. The market is less mature than leases or PPAs. Providers include regional co-ops and a few national startups.

Subscriptions appeal to customers wary of 20-year contracts. The trade-off is higher per-kWh pricing and less predictable savings. Installer attachment rates on subscriptions are lower because the sales cycle is less defined.

VPP Participation

Virtual power plant programs let TPO providers dispatch customer batteries into grid markets. The provider keeps a share of the revenue. The customer gets a bill credit or lower lease rate.

VPP revenue is volatile. It depends on wholesale market prices, utility demand response programs, and ISO rules. California, Texas, and Arizona have the most active VPP markets. Providers like Sunrun and Tesla offer VPP-enabled leases in select territories.

Installer Economics: How Your Paycheck Changes by Sale Type

TPO sales change how and when installers get paid. The total project margin is not always lower than cash. The timing is what hurts. A $30,000 TPO job pays the same total margin as cash. It just arrives 60 days later.

Cash Sale vs. Loan Sale vs. TPO Sale

| Metric | Cash Sale | Loan Sale | TPO Sale |

|---|---|---|---|

| Upfront margin | 100% at contract | 50-80% at contract | 0% at contract |

| Backend margin | $0 | 20-50% at funding | 25-35% at NTP or PTO |

| Total project margin (residential) | 25-35% | 25-35% | 25-35% |

| Total project margin (commercial) | 15-25% | 15-25% | 15-25% |

| Payment timing | Immediate | 30-60 days | 30-90 days |

| Customer paperwork burden | Low | Medium | Low |

| Installer callback risk | Higher | Medium | Lower |

On a $30,000 residential system, a cash sale puts $7,500–$10,500 in your account at contract signing. A TPO sale pays the same total margin — but only after the provider funds at notice to proceed or permission to operate. The gap creates a working capital need.

The backend on loans comes from dealer fees. Lenders pay installers an origination fee that compensates for the finance cost. Dealer fees range 15-25% of project cost. That is why loan margins match cash margins over time even though only part is paid upfront.

Residential vs. C&I TPO Margins

C&I TPO dominated the market long before residential. In 2024, TPO financed 72% of non-residential capacity versus 45% of residential. C&I projects are larger but lower margin per watt. A 500 kW commercial roof generates more total profit than a 10 kW home. The margin percentage is thinner.

Customer acquisition cost tells the story. Residential CAC runs $500–$1,500 per deal. C&I CAC hits $2,000–$5,000 or more. The sales cycle is longer. The proposal is more complex. But the project value justifies the spend.

C&I TPO providers often require installer certifications, bonding, and past project references. The barrier to entry is higher. The reward is recurring large-project volume.

Working Capital and Payment Timing

TPO providers may delay payment 30-90 days after NTP or PTO. Some pay in tranches: 50% at NTP, 50% at final inspection. Others wait for the full interconnection approval.

The common mistake is assuming payment on PTO. Read the installer agreement. Ask for a sample payment schedule before you sign. If your crew payroll runs weekly and your TPO partner pays at 60 days, you need a line of credit or cash reserves.

A solar software platform that tracks project milestones — from signed contract to NTP to PTO — helps you forecast cash flow gaps before they become crises.

How to Vet a TPO Provider: A 10-Question Scoring Framework

Not all TPO partners are stable. Not all pay on time. This framework scores providers across 4 categories. Rate each question 1-5. A total score under 30 is a red flag. Use it before you sign an installer agreement, not after your first payment is late.

Capital Stability and Credit Risk

Sunnova carries a 2.4 out of 5 rating on SolarReviews based on customer complaints and service issues. SunPower filed for Chapter 11 bankruptcy in August 2024. Mosaic paused new originations in May 2025. These events matter to installers because a provider’s financial distress delays payments, voids warranties, and strands projects mid-build.

Questions to ask:

- Are your financials public or audited by a third party?

- What is your current default rate on customer payments?

- Do you carry a backup servicer if your primary entity fails?

Red flag: no public financials and no backup servicer agreement. Green flag: publicly traded parent or audited annual report.

Savings Policy and Pricing Flexibility

Some providers cap installer pricing. They set a maximum $/watt or require their own design review. If your labor costs are above their band, you eat the difference or lose the deal.

Questions to ask:

- What is your approved pricing band per watt for my territory?

- Can I adjust pricing for complex roofs, steep pitches, or structural upgrades?

- How do you enforce savings policy — pre-approval or post-install audit?

Request the pricing band documentation in writing. Verbal allowances do not survive contract disputes.

Payment Terms and Installer Cash Flow

Payment timing is the most common installer complaint against TPO providers. NTP versus PTO triggers matter. So do holdbacks for punch-list items.

Questions to ask:

- What event triggers payment — NTP, final inspection, or PTO?

- What is your average days-to-pay from trigger event?

- Do you hold back a percentage for warranty or callback reserve?

Request a sample payment schedule for a 10 kW residential project. Compare it against your payroll and material supplier terms.

FEOC Compliance and Equipment Rules

FEOC stands for Foreign Entity of Concern. The Inflation Reduction Act ties bonus credits to domestic content. In 2026, panels and inverters need 50% domestic content. Batteries need 60%. (estimate) The non-FEOC sourcing requirement is 40% in 2026.

| Equipment | Domestic Content Threshold 2026 | FEOC Sourcing Requirement |

|---|---|---|

| Solar panels | 50% | 60% non-FEOC |

| Inverters | 50% | 60% non-FEOC |

| Batteries | 60% | 60% non-FEOC |

Questions to ask:

- Do you maintain an approved equipment list that meets domestic content and FEOC rules?

If the provider’s approved list is narrow, you may lose margin by being forced into premium equipment. If it is too broad, you risk installing non-compliant hardware that kills their tax credit — and your relationship.

Model TPO, Loan, and Cash Side-by-Side in One Platform

Stop switching between spreadsheets and design tools. SurgePV lets you compare financing scenarios, generate branded proposals, and close faster.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

For a direct comparison, see Arka 360 vs SurgePV.

Battery + TPO: Why Storage Changes the Math

Adding a battery to a TPO system shifts the value proposition. Under NEM 3.0, export rates are low. Self-consumption is the only path to real savings. A battery stores midday solar for evening use. Without it, exported power earns pennies. Installers who bundle battery and TPO close more deals and reduce callback rates.

Battery attachment rates on residential TPO systems rose from 12% in 2022 to over 35% in 2025. The trend is accelerating in California, Hawaii, and Arizona where NEM 3.0 or equivalent rate reforms have taken hold.

| Scenario | PPA-Only (7 kW) | PPA + 10 kWh Battery |

|---|---|---|

| Monthly PPA rate | $0.12/kWh | $0.12/kWh + $45 battery lease |

| Estimated monthly production | 950 kWh | 950 kWh |

| Self-consumption rate | 35% | 75% |

| Utility offset | 35% | 75% |

| Annual savings (year 1) | $480 | $1,140 |

| Battery backup during outage | None | 4-8 hours critical load |

| Contract complexity | Standard | Higher — dual equipment warranty |

The installer benefit is twofold. First, battery attachment increases total project value. A 10 kWh battery adds $8,000–$12,000 to the contract. Second, battery projects have lower callback rates because the customer is less sensitive to monthly bill swings. The customer sees backup power, not just savings.

The risk is warranty overlap. The panel provider, battery manufacturer, and inverter company may each have separate warranty terms. Clarify who handles a battery replacement in year 8 before you sign the install agreement. Some providers push the cost to the installer. Others self-insure. Read the contract.

TPO providers are also using batteries to qualify for additional incentives. The 48E credit includes adders for domestic content and energy communities. Batteries help meet the 60% domestic content threshold when paired with US-made cells. A battery with US-assembled cells can open a 10 percentage point bonus on the entire project.

Your solar design software should model battery + solar together. A solar shadow analysis software helps you place the array for maximum self-consumption potential.

State-by-State TPO Availability and Restrictions

TPO is not legal everywhere. Some states ban third-party ownership outright. Others allow leases but not PPAs. The map matters for installer expansion strategy. Entering a no-TPO state with a TPO pitch wastes marketing spend. Check the legal framework before you update your website or run paid ads.

| Category | Count | States and Territories |

|---|---|---|

| Full TPO (lease + PPA) | 28 + DC + PR | CA, TX, FL, AZ, NV, CO, HI, MD, NJ, MA, CT, NY, IL, PA, OH, GA, NC, SC, VA, WA, OR, UT, NM, MN, WI, MI, IN, MO, DC, PR |

| Lease-only | 6 | KS, KY, NE, OK, TN, WV |

| No TPO | 17 | AL, AK, AR, DE, ID, IA, LA, ME, MS, MT, NH, ND, RI, SD, VT, WY, GU |

California, Texas, and Florida represent over 55% of the US residential TPO market. Arizona and Nevada follow. These are the markets where TPO providers concentrate their capital. If you operate in one of these states, TPO should be a core product. If you do not, loan and cash products matter more.

In no-TPO states, the only financing options are cash, loans, or property-assessed clean energy (PACE). Installers in these markets should push loan partnerships and cash incentives rather than TPO. Some no-TPO states have strong solar resource and high electricity rates — Arizona excluded, states like Idaho and Louisiana still see demand, but customers must pay cash or secure private financing.

In lease-only states, PPA contracts are treated as utility regulation violations. The provider must structure the deal as a lease with fixed payments rather than per-kWh billing. The economics are similar but the contract language differs. Customers in these states lose the production guarantee that PPAs offer.

Before entering a new state, verify the current TPO legal framework with a local solar association or attorney. Rules change. Florida updated its TPO statute in 2024. Illinois expanded community solar eligibility in 2025. Check again at the state public utility commission before you update your website.

The 2026 Policy Shift: What Changed After the ITC Expired

The residential Section 25D investment tax credit expired on Dec 31, 2025. The commercial Section 48E credit remains available through 2027 with a phase-down schedule. This split reshapes which TPO models make sense. Providers now route deals through commercial entities to preserve credit access.

Safe Harboring Deadlines for 48E

To claim the full 48E credit, construction must begin by July 4, 2026. Safe harboring requires either physical work of a significant nature or binding equipment contracts placed in service within a continuous window.

Installers play a role in documentation. The TPO provider needs proof of construction start. That means signed contracts, building permits, or equipment delivery receipts. If you start a project in June 2026 but delay permitting, the provider may miss the safe harbor.

Ask your TPO partner for their documentation checklist before you schedule the first site visit. Missing a safe harbor costs them 10-30% of project value. They will pass that loss to you through lower installer rates or withheld payments.

Domestic Content Bonus Requirements

The 48E credit starts at 30% and rises with bonuses. Domestic content adds 10 percentage points. Energy community siting adds another 10. To qualify for domestic content in 2026, solar panels and inverters need 50% domestic manufacturing cost. Batteries need 60%.

The phase-in schedule tightens through 2027. In 2027, panels and inverters rise to 55%. Batteries stay at 60% through 2027, then increase.

| Year | Panels / Inverters | Batteries |

|---|---|---|

| 2026 | 50% | 60% |

| 2027 | 55% | 60% |

| 2028 | 55% | 60% |

Installers must verify equipment qualification. The TPO provider files the tax credit claim. But if the IRS audits and finds non-compliant equipment, the provider recovers from the installer via indemnity clauses.

Request the equipment qualification checklist from each provider. Cross-reference it against your procurement records. Keep certificates of origin for every panel, inverter, and battery you install on a TPO project.

How Small Installers Can Offer TPO Without Becoming Sunrun

You do not need a national salesforce to sell TPO. You need a partner. White-label TPO intermediaries let small and mid-sized installers offer leases and PPAs under their own brand while the intermediary handles capital, credit underwriting, and long-term service. The model is already proven. Thousands of local crews use it daily. For United States-specific compliance details, see United States arizona/phoenix. For United States-specific compliance details, see United States california/los-angeles.

The main intermediaries in the US market are EnFin (Sunnova’s financing arm), GoodLeap, and Palmetto LightReach. Each offers a different split of responsibilities. EnFin focuses on lease and loan products. GoodLeap adds PACE and PPA options. Palmetto LightReach targets regional installers with co-branded proposals. Dividend Finance and Sunlight Financial also serve smaller shops, though their geographic coverage is narrower.

Here is how the model works for a 5-person crew in Arizona:

- Your sales rep qualifies the lead and designs the system in your solar design software.

- You submit the project to the intermediary portal.

- The intermediary runs credit, generates the TPO contract, and funds the project.

- You install the system and submit for inspection.

- The intermediary pays you at NTP or PTO.

- The intermediary handles customer billing and maintenance for the contract term.

Sunrun holds 12.7% of the US residential solar market. The remaining 87% is fragmented across local and regional installers. TPO intermediaries exist because that fragmentation is valuable. National providers cannot knock every door. Local installers can. Intermediaries win by aggregating demand from hundreds of small shops.

The trade-off is margin compression. Intermediaries charge an origination or platform fee that reduces your total project margin by 2-5 percentage points. The offset is volume. If TPO lets you close 30% more deals, the net revenue gain outweighs the margin loss. For a crew doing 20 deals per month, a 3-point margin cut that adds 6 deals is a net gain of roughly $45,000 per month at average residential pricing.

Conclusion

TPO is now the default path for residential solar sales after the Section 25D ITC expired. Customers still want solar. They just cannot access the federal tax credit directly. TPO providers can — through 48E, domestic content bonuses, and energy community adders. The economics are different, but the demand is not.

For installers, the shift means three things. First, audit your financier relationships. Payment terms, capital stability, and equipment rules vary widely. A provider that worked in 2024 may be a liability in 2026. Run the 10-question scoring framework on every active partner. Second, map state availability before you expand. TPO is illegal in 17 states. Entering a no-TPO market with a TPO-only pitch is a fast way to waste marketing spend. Third, model battery + TPO bundles in your proposal software. NEM 3.0 makes self-consumption the only savings path. Battery attachment raises self-consumption and raises project value.

The installer who understands TPO economics — not just the pitch, but the payment timing, the equipment rules, and the provider risk — will outlast the installer who treats it as just another financing option. In 2026, financing is the product. The hardware is secondary. The crew that can explain escalators, buyout clauses, and FEOC rules builds more trust than the crew that only talks about panel efficiency.

For more details, see our guide on solar panel efficiency ranking.

Start with your current pipeline. How many of your last 20 quotes included a TPO option? If the answer is under 10, you are leaving deals on the table. Add a TPO column to every proposal. Train your reps on the differences between PPA and lease. Run the scoring framework on your current provider. Then model battery + TPO bundles in your solar proposal software.

Ready to model TPO, loan, and cash side-by-side? Book a demo and see how SurgePV handles multi-financing proposals in one workflow.

Frequently Asked Questions

What is solar as a service?

Solar as a service is a model where a third-party company owns, installs, and maintains solar panels on a customer’s property. The customer pays a monthly fee or per-kWh rate instead of buying the system outright. The provider claims tax credits, handles repairs, and retains ownership. The customer gets lower energy bills with no upfront cost.

What is the difference between a solar PPA and a solar lease?

A solar PPA charges per kilowatt-hour produced, so monthly bills vary with production. A solar lease charges a fixed monthly fee regardless of output. Both are third-party ownership models where the provider claims tax credits and handles maintenance. PPAs shift production risk to the provider. Leases shift it to the customer, who pays the same even in a cloudy month.

How do solar installers make money on TPO sales?

Installers earn an installation margin from the TPO provider, typically paid at notice to proceed or permission to operate. Margins range 25-35% for residential and 15-25% for commercial, but payment timing and working capital requirements differ from cash sales. The total dollar margin is often similar to cash. The cash flow profile is not.

Is third-party ownership solar worth it after the ITC expired?

Yes. The residential Section 25D ITC expired December 31, 2025, but the commercial Section 48E credit remains available through 2027. TPO providers can claim 48E plus domestic content and energy community adders, making TPO the primary path for homeowners to access federal incentives indirectly. The savings math shifted, but TPO still outperforms utility rates in most markets.

What happens to a solar lease when you sell your house?

The new buyer must agree to assume the lease or PPA contract. Transfer can take 2-6 weeks and may delay closing. Some buyers are hesitant to take on long-term agreements, which is why NREL research shows TPO systems do not increase property value like owned systems do. Sellers should disclose the lease early in the listing process.

Can small installers offer solar financing without being Sunrun?

Yes. Smaller installers can partner with TPO intermediaries like EnFin, GoodLeap, or Palmetto LightReach. These partners handle financing, tax credit monetization, and long-term maintenance while the installer focuses on sales and installation. The intermediary model lets a 5-person crew compete with national providers on financing without building a balance sheet.

What is FEOC compliance and why does it matter for installers?

FEOC stands for Foreign Entity of Concern. The Inflation Reduction Act requires 50% domestic content for panels and inverters and 60% for batteries to qualify for full bonus credits. Installers must verify equipment sourcing or risk their TPO provider losing tax credit eligibility. Non-compliance triggers indemnity clauses that can claw back installer payments years after the project is built.