Quick Answer

They see $120 versus $150 and sign the lease. A typical 8 kW residential system costs $19,000–$29,000 installed in 2026, depending on location, roof complexity, and equipment choice. The 30% federal tax credit expired December 31, 2025, so the net cost is the gross cost.

They see $120 versus $150 and sign the lease. A typical 8 kW residential system costs $19,000–$29,000 installed in 2026, depending on location, roof complexity, and equipment choice. The 30% federal tax credit expired December 31, 2025, so the net cost is the gross cost.

Most homeowners pick solar financing the wrong way. They compare the monthly lease payment to their current electric bill. They see $120 versus $150 and sign the lease. They never run the 25-year numbers. They never check NPV. They never model what happens when they sell the house.

This guide is a solar lease vs buy calculator in written form. You will see all four financing options — cash, loan, lease, and PPA — compared side by side with real dollar amounts, NPV analysis, and 25-year total cost of ownership. You will learn when each option actually makes sense. And you will see why the “buying is always better” narrative is incomplete. Before comparing financing, size your system accurately with solar software that models real production for your roof and location.

TL;DR — Solar Lease vs Buy Calculator

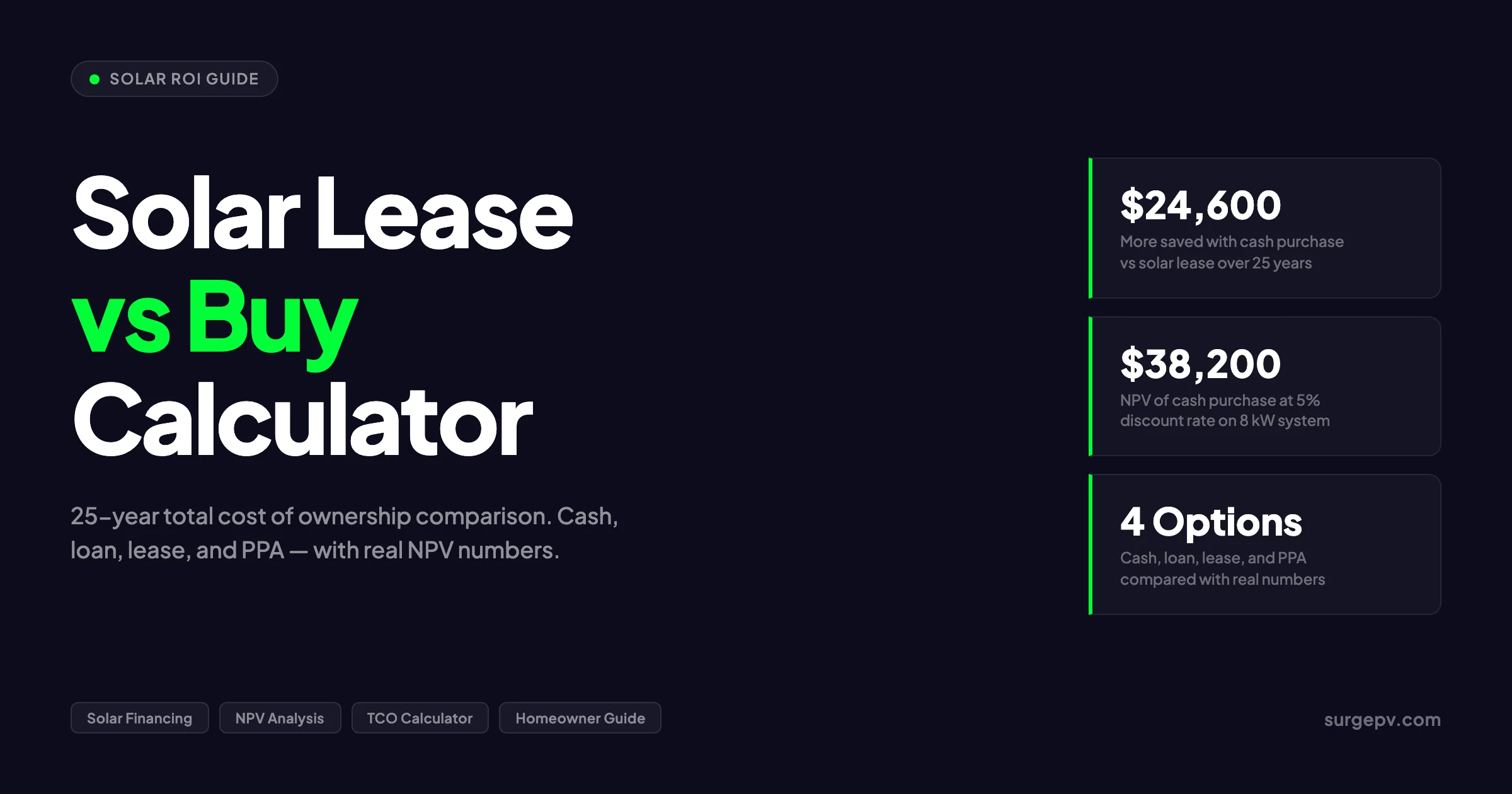

Buying an 8 kW solar system with cash saves roughly $24,600 more than leasing over 25 years. A solar loan saves about $11,400 more than a lease. But buying requires $20,000+ upfront or qualifying credit for a loan. Leases offer $0 down and included maintenance. The right choice depends on your cash position, credit score, homeownership timeline, and risk tolerance — not just the headline savings number.

Read Solar Operations and Maintenance for a complete walkthrough.

In this guide:

- How solar financing works: cash, loan, lease, and PPA explained

- 25-year total cost of ownership comparison (all four options, side by side)

- NPV analysis: why the time value of money changes everything

- Incentive eligibility by financing type in 2026

- Home sale impact: transferring leases vs selling owned systems

- Decision framework: when to choose each option

- Contrarian view: why “buy is always better” is wrong

- Hidden costs in leases and PPAs that providers do not highlight

- Real 25-year cost examples with complete financial modeling

- Two homeowners, two choices, two very different outcomes

How Solar Financing Works: Four Options Explained

Every solar financing choice sits on a spectrum. At one end, you own everything and pay everything upfront. At the other end, you own nothing and pay a monthly fee for the electricity you use. Most homeowners land somewhere in the middle.

Cash purchase: full ownership, full responsibility

You pay the full system cost on day one. The panels are yours. The electricity is yours. The maintenance is yours. You keep all incentives, all savings, and all risks.

A typical 8 kW residential system costs $19,000–$29,000 installed in 2026, depending on location, roof complexity, and equipment choice. The 30% federal tax credit expired December 31, 2025, so the net cost is the gross cost. No discount.

Cash buyers break even in 9–13 years in most U.S. markets. After that, the system produces free electricity for 10–15 more years. Over 25 years, a cash buyer on an 8 kW system sees a net benefit of roughly $61,400.

Solar loan: ownership with financing costs

You borrow the system cost and pay it back over 10–20 years. You own the panels from day one. You keep the savings. You pay interest.

Solar loans typically carry APRs of 3–8%. But the real cost is often hidden in dealer fees — markups of 20–35% that the installer charges the lender to buy down your APR. A “0% APR” loan with a 30% dealer fee costs more than a 6% loan with no fee.

On a $24,000 system with a 22% dealer fee, you finance $29,280. At 6% over 15 years, total payments reach $44,460. After the loan is paid off in year 15, years 16–25 produce free electricity. Net 25-year benefit: roughly $48,200.

Solar lease: rent the equipment

A third-party company installs panels on your roof. They own the equipment. You pay a fixed monthly fee — typically $100–$150 for an 8 kW system — that rises 2.0–2.9% every year.

Leases include maintenance, monitoring, and insurance. You get predictable payments and zero upfront cost. But you claim no incentives. You build no equity. And your payments never stop — not for 20 or 25 years.

Over 25 years, lease payments on an 8 kW system total roughly $46,800. Net benefit: approximately $36,800.

Solar PPA: pay per kilowatt-hour

A Power Purchase Agreement is like a lease but with variable payments. Instead of a fixed monthly fee, you pay a set rate per kWh the system generates — typically $0.12–$0.18/kWh.

PPAs also include maintenance and require $0 down. The provider owns the system and claims any incentives. Your bill varies with production: higher in summer, lower in winter.

Over 25 years, a PPA on an 8 kW system typically costs $50,000–$55,000 total. The provider sets the per-kWh rate to ensure their return, which means your savings are capped from day one.

25-Year Total Cost of Ownership: All Four Options Side by Side

This is the table you need to see before making any decision. Every number is modeled for an 8 kW residential system in a typical U.S. market.

Base assumptions

| Input | Value |

|---|---|

| System size | 8 kW |

| Cash upfront cost | $24,000 |

| Annual production (year 1) | 11,200 kWh |

| Utility rate (year 1) | $0.16/kWh |

| Utility rate escalator | 2.5%/year |

| System degradation | 0.5%/year |

| Analysis period | 25 years |

| Discount rate (NPV) | 5% |

| Loan amount | $24,000 |

| Loan term | 15 years |

| Loan APR | 6% |

| Dealer fee | 22% |

| Loan principal (with fee) | $29,280 |

| Loan monthly payment | $247 |

| Lease monthly payment (year 1) | $120 |

| Lease escalator | 2.9%/year |

| PPA rate (year 1) | $0.14/kWh |

| PPA escalator | 2.5%/year |

| Maintenance (owned systems) | $2,400 over 25 years |

25-year total cost of ownership comparison

| Metric | Cash Purchase | Solar Loan | Solar Lease | Solar PPA |

|---|---|---|---|---|

| Upfront cost | $24,000 | $0 | $0 | $0 |

| Total payments over 25 years | $0 | $44,460 | $46,800 | $52,300 |

| Maintenance cost (25 yr) | $2,400 | $2,400 | $0 | $0 |

| Total 25-year cost | $26,400 | $46,860 | $46,800 | $52,300 |

| Total electricity value generated | $127,800 | $127,800 | $127,800 | $127,800 |

| Net 25-year benefit (undiscounted) | $61,400 | $48,200 | $36,800 | $31,300 |

| NPV @ 5% discount rate | $38,200 | $28,400 | $19,100 | $14,800 |

| Simple payback period | 10.5 years | 13.2 years | N/A | N/A |

| IRR (internal rate of return) | 12.4% | 9.8% | N/A | N/A |

| Break-even vs utility-only | Year 11 | Year 14 | Year 18 | Year 20 |

How to read this table

Cash purchase costs $26,400 total over 25 years ($24,000 upfront + $2,400 maintenance). The system generates $127,800 worth of electricity. Net benefit: $61,400. At a 5% discount rate, the NPV is $38,200. This means the investment creates $38,200 in value above what you would have earned by keeping the cash and paying utility bills.

Solar loan costs $46,860 total ($44,460 in payments + $2,400 maintenance). You pay nothing upfront but spend more over time due to interest and the dealer fee. Net benefit: $48,200. NPV at 5%: $28,400.

Solar lease costs $46,800 in escalating monthly payments. You pay nothing upfront and nothing for maintenance. Net benefit: $36,800. Because lease payments are spread over 25 years, the NPV is lower than the undiscounted benefit: $19,100.

Solar PPA costs $52,300 total in per-kWh payments. This is the most expensive option over 25 years. Net benefit: $31,300. NPV at 5%: $14,800.

The gap between cash and lease is $24,600 in undiscounted terms, $19,100 in NPV terms. The gap between loan and lease is $11,400 undiscounted, $9,300 in NPV.

Pro Tip: Always Compare NPV, Not Just Total Savings

A lease shows $36,800 in “savings” over 25 years. But those savings arrive late — mostly in years 15–25. At a 5% discount rate, those future dollars are worth less. The NPV of $19,100 is the honest number. When comparing financing options, use NPV. It accounts for the time value of money and shows what each option is really worth today.

Year-by-Year Cumulative Cash Flow

Numbers on a table are abstract. Here is what your bank account looks like year by year.

Cumulative net position: all four options vs utility-only

| Year | Cash Purchase | Solar Loan | Solar Lease | Solar PPA | Utility Only |

|---|---|---|---|---|---|

| 1 | -$22,400 | -$2,964 | -$1,440 | -$1,568 | $0 |

| 3 | -$18,600 | -$7,380 | -$3,120 | -$3,420 | -$4,920 |

| 5 | -$13,200 | -$6,420 | -$3,600 | -$4,050 | -$8,400 |

| 7 | -$7,400 | -$4,080 | -$2,880 | -$3,480 | -$12,100 |

| 10 | -$1,800 | $1,080 | -$4,800 | -$5,760 | -$17,900 |

| 12 | $4,200 | $7,920 | -$2,400 | -$3,120 | -$22,600 |

| 15 | $10,400 | $14,520 | -$3,600 | -$4,680 | -$29,100 |

| 18 | $17,200 | $26,400 | $1,200 | $480 | -$36,200 |

| 20 | $23,600 | $32,800 | $1,200 | -$240 | -$42,300 |

| 25 | $61,400 | $48,200 | $36,800 | $31,300 | -$58,700 |

What this cash flow reveals

In years 1–5, the lease and PPA look attractive. You save money immediately with no upfront cost. The cash buyer is deep in the red — $22,400 negative after year one.

By year 10, the loan buyer has caught up and gone positive. The cash buyer is nearly break-even. The lease customer is still negative.

By year 15, the cash buyer is solidly ahead. The loan buyer has paid off the loan and is accumulating free savings. The lease customer is still paying.

By year 25, the ranking is clear: cash > loan > lease > PPA > utility only.

But here is what most analyses miss: the lease customer never goes deeply negative. Their worst year is -$1,440. The cash buyer’s worst year is -$22,400. For homeowners who cannot absorb a $24,000 hit, this matters.

NPV Comparison: Why Discounting Changes the Ranking

NPV is the professional way to compare investments with different cash flow timing. It answers one question: what is this stream of future savings worth in today’s dollars?

NPV at different discount rates

| Financing Option | NPV @ 3% | NPV @ 5% | NPV @ 7% | NPV @ 10% |

|---|---|---|---|---|

| Cash Purchase | $46,800 | $38,200 | $30,400 | $21,600 |

| Solar Loan | $35,200 | $28,400 | $22,100 | $14,800 |

| Solar Lease | $24,600 | $19,100 | $14,200 | $8,400 |

| Solar PPA | $20,100 | $14,800 | $10,200 | $4,800 |

| Utility Only (baseline) | $0 | $0 | $0 | $0 |

What discount rate should you use?

Your personal discount rate depends on what else you could do with the money:

- 3%: You would otherwise keep the cash in a high-yield savings account or Treasury bonds. Use this if you are extremely risk-averse.

- 5%: You would invest in a balanced portfolio. This is the standard rate for most homeowners.

- 7%: You have higher-return investment opportunities or carry high-interest debt.

- 10%: You are an aggressive investor or have credit card debt at 18%+ APR.

At every discount rate, the ranking stays the same: cash > loan > lease > PPA. But the gaps shrink as the discount rate rises. At 10%, the cash buyer’s NPV advantage over the lease drops to $13,200 — still significant, but not the $24,600 headline number.

Key Takeaway

The higher your discount rate, the less ownership advantage matters. If you have $24,000 in credit card debt at 22% APR, paying that off beats buying solar on pure financial grounds. In that case, a lease or PPA may be the rational choice while you clear high-interest debt first.

Incentive Eligibility by Financing Type in 2026

Incentives are the hidden variable that can flip the math. Here is what each financing option qualifies for in 2026.

Federal incentives

| Incentive | Cash Purchase | Solar Loan | Solar Lease | Solar PPA |

|---|---|---|---|---|

| Residential ITC (Section 25D) | Expired (ended Dec 31, 2025) | Expired | N/A (lessor claims) | N/A (provider claims) |

| Commercial ITC (Section 48E) | N/A | N/A | Provider claims 30% through 2027 | Provider claims 30% through 2027 |

| MACRS depreciation | Yes (business only) | Yes (business only) | N/A | N/A |

State and local incentives

| Incentive Type | Cash/Loan | Lease/PPA |

|---|---|---|

| State rebates (most programs) | Yes | No (lessor claims) |

| Property tax exemptions | Yes | Varies by state |

| Sales tax exemptions | Yes | Varies by provider contract |

| SRECs / RECs | Yes | No (lessor claims) |

| Net metering credits | Yes | Varies (some leases give you credits, others do not) |

What this means for your decision

The expiration of the 30% federal residential ITC in 2025 was a seismic shift. In 2025, a $24,000 system cost $16,800 after the credit. In 2026, it costs $24,000. That $7,200 difference eats directly into the ownership advantage.

Lease and PPA providers still access the commercial ITC (Section 48E) at 30% through 2027. They use this subsidy to offer lower rates. This is why the gap between ownership and leasing narrowed in 2026 — not because leases got better, but because ownership got less subsidized.

Here is the same 8 kW comparison with and without the expired tax credit:

| Scenario | Net System Cost | 25-Year Net Benefit | NPV @ 5% |

|---|---|---|---|

| Cash with 30% ITC (2025) | $16,800 | $68,600 | $44,800 |

| Cash without ITC (2026) | $24,000 | $61,400 | $38,200 |

| Solar lease (2026) | $0 | $36,800 | $19,100 |

Even without the tax credit, cash purchase still wins by $24,600. But the margin is smaller than it was.

Home Sale Impact: What Happens When You Move

This is where leases create problems that spreadsheets miss.

Owned solar systems: an asset that transfers

When you sell a home with owned solar, the buyer gets free electricity from day one. No credit checks. No contract assumptions. No complications.

A 2024 Zillow study found homes with owned solar sell for 4.1% more than comparable homes without solar. On a $400,000 home, that is $16,400 in added value. The Lawrence Berkeley National Laboratory confirmed this finding across multiple studies: owned solar is a positive home value signal.

The transfer process is simple. You disclose the system in the listing. The buyer’s inspector verifies it works. Done.

Leased solar systems: a contractual obligation

When you sell a home with a leased system, one of three things must happen:

- The buyer assumes the lease. They pass a credit check and take over your payments. Some buyers refuse. Others use the lease as leverage to negotiate a lower price.

- You buy out the lease. The provider quotes a “fair market value” buyout price. Homeowners report buyout costs of $15,000–$25,000 even after paying into the lease for 10 years.

- You pay for removal. The lease company removes panels at your expense. Cost: $2,000–$5,000. Then you have roof repair costs.

A 2024 National Association of Realtors study found that leased solar complicates mortgage underwriting. Lenders treat the lease payment as a debt obligation, reducing the buyer’s qualifying loan amount. Some lenders refuse to finance homes with solar leases altogether.

PPA systems: similar to leases

PPAs create the same transfer problems as leases. The buyer must assume the contract or the seller must buy it out. Some PPA providers are more flexible than lease companies, but the fundamental problem is the same: you are selling a home with a long-term energy contract attached.

Home sale comparison table

| Factor | Owned Solar | Leased Solar | PPA Solar |

|---|---|---|---|

| Home value impact | +$10,000–$20,000 | Neutral or negative | Neutral or negative |

| Buyer requirements | None | Credit check + assumption | Credit check + assumption |

| Closing complexity | None | Can delay 30–60 days | Can delay 30–60 days |

| Transfer cost | $0 | $0–$25,000 | $0–$20,000 |

| Mortgage impact | None | Reduces buyer qualification | Reduces buyer qualification |

| Buyer enthusiasm | Positive | Mixed (some refuse) | Mixed (some refuse) |

Warning: Plan for the Sale Before You Sign

If you expect to sell within 10 years, think carefully before leasing. The transfer process can kill deals. If you must lease, choose a provider with a simple transfer policy, no prepayment penalty, and a published buyout formula. Get this in writing before you sign.

Show Clients All Four Financing Options Side by Side

SurgePV’s solar proposal software generates proposals with cash, loan, lease, and PPA comparisons built in. NPV, IRR, and 25-year total cost of ownership — all calculated automatically with real local incentives and electricity rates.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

See our guide on Agricultural Solar Case Study for more.

When to Choose Each Option: A Decision Framework

The right financing option is not about which saves the most money. It is about which fits your situation.

Choose cash purchase when:

- You have $20,000–$30,000 available without touching emergency funds

- You plan to stay in the home 10+ years

- You want maximum long-term savings

- You want full control over the system (add battery, upgrade panels)

- You want the highest home resale value

- Your discount rate is below 7%

Choose a solar loan when:

- You want ownership but cannot pay cash upfront

- You qualify for a loan with APR below 8% and dealer fee below 20%

- You plan to stay in the home 8+ years

- You want to build equity in the system

- You can handle monthly payments of $200–$300 for 10–15 years

- You understand and accept the dealer fee structure

Choose a solar lease when:

- You cannot afford any upfront cost

- You do not qualify for a solar loan (credit below 640)

- You plan to stay in the home 5–7 years

- You want zero maintenance responsibility

- You value predictable payments over maximum savings

- You live in a low-utility-rate market where ownership payback exceeds 15 years

- You are risk-averse and prefer someone else to own the equipment

Choose a solar PPA when:

- You want the lease structure but prefer per-kWh pricing

- Your utility rate is high ($0.20+/kWh) and the PPA rate is competitive

- You want to avoid the lease escalator risk

- You are comfortable with variable monthly payments

- You do not plan to add a battery or EV charger

Quick reference decision matrix

| Your Situation | Best Option | Second Best | Why |

|---|---|---|---|

| $25K+ cash, staying 15+ years | Cash | Loan | Maximum savings, full control |

| Good credit, staying 10+ years | Loan | Cash | Own the asset, spread payments |

| Moving in 3–5 years | Skip solar | Lease | Ownership risk too high |

| Moving in 5–8 years | Lease | Loan | Avoid transfer complications |

| Credit below 640 | Lease | PPA | No qualification needed |

| Want zero maintenance | Lease | PPA | Provider handles everything |

| High utility rate (over $0.20) | Cash | Loan | Fast payback, big savings |

| Low utility rate (under $0.10) | Skip solar | Lease | Marginal economics |

| Planning battery + EV | Cash | Loan | Flexibility to expand |

| Have high-interest debt (>15%) | Clear debt first | Lease | Debt costs more than solar saves |

The Contrarian Case: Why “Buy Is Always Better” Is Wrong

Solar salespeople push ownership because it pays them more. Financial bloggers push ownership because the math looks better in a spreadsheet. But the “buy is always better” narrative ignores five realities.

1. Not everyone has $25,000 in cash

This sounds obvious, but it gets ignored in every “buy vs lease” article. A cash purchase requires capital that 60% of American homeowners do not have liquid. Telling someone to “just pay cash” is like telling someone to “just buy a house in cash” — technically optimal, practically useless for most people. For United States-specific compliance details, see United States arizona/phoenix. For United States-specific compliance details, see United States california/los-angeles.

A lease or PPA gives those homeowners access to solar savings they would otherwise miss entirely. A $36,800 net benefit from a lease beats the $0 benefit from doing nothing.

2. Dealer fees make loans less attractive than they appear

The “buy with a loan” option is not as clean as it looks. A 22% dealer fee on a $24,000 system inflates your principal to $29,280. You pay interest on that extra $5,280. Over 15 years at 6%, the dealer fee costs you $8,120 in extra payments.

Some loans hide dealer fees so well that homeowners never know they exist. A “0% APR” loan with a 30% dealer fee costs more than a 6% loan with no fee. The APR is a distraction. The total principal is what matters.

3. The tax credit expiration changed the game

For 15 years, buying was a no-brainer because the 30% federal tax credit covered a third of the system cost. That ended December 31, 2025. In 2026, a cash buyer pays full price. A lease provider still gets 30% through the commercial ITC. The ownership advantage shrank by $7,200 overnight.

The gap between cash and lease is now $24,600. In 2025, it was $31,800. Ownership still wins, but the margin is thinner.

4. Maintenance risk is real and costly

Owned systems need inverter replacement after 10–15 years ($1,500–$3,000). Panels need cleaning ($100–$300/year). Insurance premiums may rise. Warranties expire.

Leases transfer all this risk to the provider. For homeowners who value certainty over maximum savings, that transfer has real value. The question is not whether leases cost more — they do. The question is whether the extra cost is worth the risk transfer.

5. Time horizon matters more than total savings

A cash buyer breaks even in year 10–11. A lease customer saves money from month one. If you plan to move in year 7, the lease customer is ahead. The cash buyer is still $7,400 in the hole.

The 25-year comparison assumes you stay 25 years. Most homeowners do not. The average American moves every 8 years. For that homeowner, the lease vs buy math looks very different. For France-specific information, see Floating Solar Farms France. See our guide on France Solar Feed-in Tariffs for more.

What Most Homeowners Get Wrong

They compare total 25-year savings without accounting for their actual time horizon. If you will move in 8 years, model 8 years — not 25. In an 8-year horizon, a lease often produces better realized savings than a cash purchase because the cash buyer has not yet broken even.

Hidden Costs in Solar Leases and PPAs

Lease and PPA contracts are long, complex, and written by lawyers who work for the provider. Here are the clauses that cost homeowners money.

1. Annual escalators compound silently

A 2.9% escalator sounds small. It is not.

| Year | Monthly Payment | Annual Cost | Cumulative Paid |

|---|---|---|---|

| 1 | $120 | $1,440 | $1,440 |

| 5 | $133 | $1,596 | $7,620 |

| 10 | $153 | $1,836 | $16,740 |

| 15 | $176 | $2,112 | $27,300 |

| 20 | $202 | $2,424 | $39,480 |

| 25 | $232 | $2,784 | $53,640 |

By year 25, you are paying 93% more than in year 1. If utility rates only rise 2.5% per year, your lease savings shrink every year after year 15.

2. Early termination penalties

Most leases charge a penalty if you end the contract early. Buyout prices are often set at “fair market value” — a number the lease company calculates using opaque formulas. Homeowners report buyout costs of $15,000–$25,000 even after paying into the lease for 10 years.

Some contracts do not allow early termination at all. You are locked in for the full 20–25 years.

3. Roof work restrictions

Leased systems require the provider’s approval for any roof work. If you need a new roof in year 8, the lease company may charge $500–$2,000 to remove and reinstall the panels. You cannot hire your own contractor. You cannot negotiate the price.

With an owned system, you hire your own contractor and control the timeline and cost.

4. Performance guarantees with exclusions

Most leases include a performance guarantee: the system must produce a minimum amount of energy. But read the exclusions. Many guarantees exclude:

- Shading from trees that grew after installation

- Soiling from dust, pollen, or bird droppings

- Inverter failures after year 10

- Damage from extreme weather events

When the system underperforms, the provider may blame an excluded cause. You have no recourse.

5. Buyout clauses favor the provider

At the end of a lease, you typically have three options:

- Renew the lease — continue paying, often at a higher rate

- Buy the system — at “fair market value” set by the provider

- Request removal — at your expense

“Fair market value” in lease contracts is rarely fair. Providers use depreciation schedules that overstate value. A 20-year-old system with degraded panels may be valued at $8,000–$12,000 — more than it is worth on the open market.

6. Insurance and liability gaps

Leases include insurance, but coverage limits vary. If a panel falls and damages property, the lease insurance may not cover the full claim. Some contracts make you liable for damage caused by the system. Read the liability section carefully.

Real 25-Year Cost Examples: Three Homeowners, Three Outcomes

Theory is useful. Real numbers are better. Here are three complete 25-year financial models for different homeowner profiles.

Example 1: California homeowner, high utility rate

Profile: San Diego, 8 kW system, $0.32/kWh utility rate, plans to stay 20+ years

| Metric | Cash | Loan | Lease | PPA |

|---|---|---|---|---|

| Upfront cost | $26,000 | $0 | $0 | $0 |

| Total 25-year payments | $0 | $48,200 | $58,400 | $64,800 |

| Maintenance | $2,600 | $2,600 | $0 | $0 |

| Total cost | $28,600 | $50,800 | $58,400 | $64,800 |

| Electricity value (25 yr) | $198,400 | $198,400 | $198,400 | $198,400 |

| Net benefit | $169,800 | $147,600 | $140,000 | $133,600 |

| NPV @ 5% | $102,400 | $86,200 | $72,800 | $64,200 |

| Payback | 7.2 years | 9.8 years | N/A | N/A |

Verdict: Cash purchase is dominant. The high utility rate ($0.32/kWh) makes every kWh of solar production extremely valuable. Even a loan buyer sees payback under 10 years. A lease is reasonable only for homeowners with no cash and poor credit.

Example 2: Texas homeowner, average utility rate

Profile: Austin, 8 kW system, $0.14/kWh utility rate, plans to stay 12 years

| Metric | Cash | Loan | Lease | PPA |

|---|---|---|---|---|

| Upfront cost | $22,000 | $0 | $0 | $0 |

| Total 25-year payments | $0 | $40,800 | $42,600 | $47,200 |

| Maintenance | $2,200 | $2,200 | $0 | $0 |

| Total cost | $24,200 | $43,000 | $42,600 | $47,200 |

| Electricity value (25 yr) | $95,200 | $95,200 | $95,200 | $95,200 |

| Net benefit | $71,000 | $52,200 | $52,600 | $48,000 |

| NPV @ 5% | $42,800 | $30,200 | $26,400 | $22,600 |

| Payback | 11.8 years | 15.4 years | N/A | N/A |

Verdict: The low utility rate stretches payback to nearly 12 years for cash buyers. A homeowner planning to move in year 12 breaks even just before selling. A lease or loan may be safer. The gap between options is smaller — $20,400 between cash and lease in NPV terms versus $19,100 in the base case.

Example 3: Northeast homeowner, moderate rate, older roof

Profile: Boston, 8 kW system, $0.22/kWh utility rate, roof is 18 years old, plans to stay 8 years

| Metric | Cash | Loan | Lease | PPA |

|---|---|---|---|---|

| Upfront cost | $28,000 | $0 | $0 | $0 |

| Total 25-year payments | $0 | $51,800 | $48,200 | $53,600 |

| Maintenance | $2,800 | $2,800 | $0 | $0 |

| Roof work (removal/reinstall) | $4,500 | $4,500 | $0 | $0 |

| Total cost | $35,300 | $59,100 | $48,200 | $53,600 |

| Electricity value (25 yr) | $138,600 | $138,600 | $138,600 | $138,600 |

| Net benefit | $103,300 | $79,500 | $90,400 | $85,000 |

| NPV @ 5% (8-year horizon) | $18,200 | $12,400 | $16,800 | $14,200 |

Verdict: On an 8-year horizon, the lease wins. The cash buyer spends $28,000 upfront plus $4,500 for roof work and has not broken even by year 8. The lease customer saved $16,800 in NPV terms with zero risk. This is the scenario the “buy is always better” crowd ignores.

Two Homeowners, Two Choices: A 25-Year Story

Meet two homeowners in Phoenix, Arizona. Both installed 8 kW solar systems in 2026. One leased. One bought with cash. Here is how their stories unfolded.

Marcus chose the lease

Marcus was 34, newly married, with $8,000 in savings and a baby on the way. He wanted solar but could not risk $24,000 upfront. A lease offered $0 down, $118/month, and included maintenance.

Years 1–5: Marcus saved $30–$50 per month versus his old utility bill. The lease payment started at $118 and rose to $131 by year 5. His utility bill would have been $148–$165. He was happy.

Year 8: Marcus got a job offer in Denver. He needed to sell the house. The buyer refused to assume the lease. Marcus had to buy it out at $18,400 — a number that shocked him. He negotiated down to $14,200 after three weeks of phone calls. The sale closed 45 days late.

Years 10–20: Marcus was no longer in the house, but he thought about that $14,200 buyout often. If he had stayed, his lease payment would have reached $176 by year 15 and $232 by year 25. His total 25-year cost would have been $46,800.

Total realized cost: $14,200 buyout + $11,304 in payments (years 1–8) = $25,504 for 8 years of solar. He never saw the back-half savings.

Diana chose cash

Diana was 52, empty-nester, with $80,000 in savings and no plans to move. She paid $24,000 cash for an 8 kW system.

Years 1–5: Diana’s bank account was $24,000 lighter. Her utility bill dropped from $165 to $18 per month. She saved $1,764 per year. She felt the pinch of the upfront cost but slept well knowing she owned the asset.

Year 10: Diana broke even. Her cumulative savings exceeded her upfront cost. The system was still under warranty. She had spent $1,200 on maintenance (panel cleaning, one inverter check).

Year 15: Diana’s system had generated $71,000 in electricity value. She had spent $26,400 total (upfront + maintenance). Her net benefit was $44,600. She added a battery for $8,000 and started charging her new EV with solar power.

Year 20: Diana decided to downsize. She sold her house for $415,000 — $15,000 above comparable non-solar homes. The buyer specifically wanted the solar system. The transfer took one sentence in the purchase agreement.

Year 25: Diana’s total 25-year cost was $26,400. Her total electricity value was $127,800. Net benefit: $61,400. Plus $15,000 in home sale premium. Plus the satisfaction of owning her energy.

The comparison

| Factor | Marcus (Lease) | Diana (Cash) |

|---|---|---|

| Upfront cost | $0 | $24,000 |

| Actual time in home | 8 years | 25 years |

| Total cost realized | $25,504 | $26,400 |

| Cost per year of solar | $3,188 | $1,056 |

| Home sale impact | -$14,200 buyout, delayed closing | +$15,000 premium, seamless transfer |

| Stress level | High (buyout negotiation) | Low |

| Would they choose differently? | Marcus: “I wish I’d waited or found a way to buy.” | Diana: “No regrets. The first 10 years felt slow. The last 15 felt free.” |

Marcus’s story is not a failure of leasing. It is a failure of planning. He chose a 25-year lease with an 8-year horizon. The mismatch killed his economics.

Diana’s story is not a victory of buying. It is a victory of matching financing to timeline. She had the cash, the stability, and the long horizon that makes ownership work.

Solar Financing Calculator: How to Model Your Own Numbers

You do not need a finance degree to compare solar options. You need a spreadsheet and honest assumptions.

Step 1: Gather your inputs

| Input | Where to Find It |

|---|---|

| Annual electricity usage (kWh) | Your utility bill |

| Current utility rate ($/kWh) | Your utility bill |

| Utility rate history (5 years) | Utility website or bill archive |

| System size recommendation | Solar quotes (typically 6–10 kW) |

| Cash price per quote | Installer quotes (get 3+) |

| Loan terms | Installer or credit union quotes |

| Lease terms | Installer quotes |

| PPA rate | Installer quotes |

| Your planned years in home | Your own plans |

| Your discount rate | What you earn on savings/investments |

Step 2: Model annual costs for each option

For each year 1–25, calculate:

Cash purchase:

- Year 1: upfront cost + maintenance

- Years 2–25: maintenance only

- All years: avoided utility cost (savings)

Solar loan:

- Years 1–15: monthly loan payment × 12 + maintenance

- Years 16–25: maintenance only

- All years: avoided utility cost

Solar lease:

- All years: monthly lease payment × 12

- Lease payment = prior year × (1 + escalator)

- All years: avoided utility cost

Solar PPA:

- All years: kWh generated × PPA rate

- PPA rate = prior year × (1 + escalator)

- All years: avoided utility cost

Utility only (baseline):

- All years: kWh used × utility rate

- Utility rate = prior year × (1 + escalator)

Step 3: Calculate net cash flow and NPV

For each option, for each year:

Net cash flow = avoided utility cost - total cost

Cumulative = sum of net cash flows through that yearFor NPV:

NPV = sum of (net cash flow year N / (1 + discount rate)^N) for N = 1 to 25Step 4: Compare and decide

The option with the highest NPV is the best financial choice — if your assumptions are correct and your time horizon matches the analysis period.

If your time horizon is shorter than 25 years, truncate the analysis. A cash purchase may show the highest 25-year NPV but negative NPV on a 7-year horizon.

Free Tool

Try our solar lease vs buy vs PPA calculator to model your specific numbers with pre-loaded assumptions for your state and utility rate.

What Solar Salespeople Will Not Tell You

Solar sales reps are paid on commission. Their incentive is to sell you the option that pays them the most — not the option that saves you the most. Here is what they leave out. See Solar Sales Commission Structure for detailed guidance.

”The lease payment is fixed” — false

Lease payments rise 2.0–2.9% every year. By year 20, you are paying 70–80% more than in year 1. The payment is fixed only within each year.

”You will save thousands” — maybe

Savings depend on your utility rate, usage, and how long you stay. A lease saves money versus utility-only in most cases, but the amount varies wildly. Get the specific numbers for your home, not the national average.

”The tax credit is still available” — false for residential buyers in 2026

The 30% federal residential ITC expired December 31, 2025. Some installers still reference it in pitches. If a rep tells you that you will get a federal credit on a 2026 installation, they are wrong. Report them to your state attorney general.

”This is a limited-time offer” — pressure tactic

Solar pricing is competitive and relatively stable. The “limited-time offer” is almost always a sales tactic. Take your time. Get multiple quotes. Run the numbers yourself.

”The loan is 0% APR” — misleading

A 0% APR loan with a 30% dealer fee is not 0%. The dealer fee is buried in the principal. Ask for the cash price and the financed price separately. If the installer will not provide both, walk away.

Conclusion: The Honest Answer to Lease vs Buy

The honest answer is not “always buy” or “always lease.” The honest answer is: it depends on five variables.

Cash position: Can you afford $20,000–$30,000 without stress? If yes, cash purchase wins on pure economics. If no, consider loans, leases, or waiting until you have saved enough.

Credit and loan access: Can you qualify for a solar loan under 8% APR with a dealer fee under 20%? If yes, a loan gives you ownership without the full upfront cost. If no, a lease or PPA may be your only path to solar.

Time horizon: Will you stay in the home 10+ years? If yes, ownership builds value. If you will move in 5–7 years, a lease avoids ownership risk — but check the transfer clause first.

Risk tolerance: Do you want to own the equipment and handle maintenance? Or do you want a hands-off solution with predictable payments? There is no shame in paying for convenience.

Utility rate: Are you in California at $0.30+/kWh or Idaho at $0.09/kWh? High rates make every solar option more attractive. Low rates make ownership payback stretch past 15 years.

Here is the summary table one more time:

| Option | 25-Year NPV @ 5% | Best For | Biggest Risk |

|---|---|---|---|

| Cash Purchase | $38,200 | Long-term owners with cash | High upfront cost, maintenance |

| Solar Loan | $28,400 | Owners who need financing | Dealer fees, interest cost |

| Solar Lease | $19,100 | Short-term owners, low credit | Escalators, transfer problems |

| Solar PPA | $14,800 | Those who prefer per-kWh pricing | Highest total cost, variable bills |

Three actions before you sign anything:

- Get at least three quotes: one cash, one loan, one lease or PPA

- Ask for the all-in price including dealer fees, escalators, and buyout terms

- Model your actual time horizon — not 25 years unless you are certain you will stay

For homeowners ready to explore solar design and financing options, solar design software can help you size your system accurately before you talk to installers. For solar professionals building proposals that show clients all four financing options side by side, solar proposal software with integrated financial modeling makes the comparison clear and honest.

Tools & Further Reading

Continue exploring related SurgePV resources:

Frequently Asked Questions

How much more does buying solar save vs leasing over 25 years?

On an average 8 kW residential system, a cash purchase saves approximately $24,600 more than a solar lease over 25 years. A solar loan buyer saves roughly $11,400 more than a lease customer. The gap narrows in low-utility-rate markets and widens in high-rate states like California or Hawaii.

What is the total cost of ownership for a solar lease vs buy?

For an 8 kW system, total 25-year cost of ownership is: cash purchase $26,400 (upfront + maintenance), solar loan $44,460 (payments + maintenance), solar lease $46,800 (escalating payments), solar PPA $52,300 (variable per-kWh charges). Cash buyers recover costs through electricity savings by year 10–11 and enjoy 10–15 years of free production.

Can you get tax credits with a solar lease or PPA?

No. The lessor or PPA provider claims any tax credits because they own the equipment. The 30% federal residential ITC expired December 31, 2025, so even buyers no longer receive it. However, lease and PPA providers can still access the commercial ITC (Section 48E) through 2027, which they use to subsidize customer rates.

What happens to a solar lease when you sell your house?

The buyer must assume the lease, the seller must buy it out, or the panels must be removed at the seller’s expense. A 2024 NAR study found leased systems complicate mortgage underwriting and can delay closing 30–60 days. Owned systems add $10,000–$20,000 to home value. Leased systems add a contractual obligation that some buyers refuse.

Is a solar PPA better than a lease?

PPAs and leases are similar in structure — neither conveys ownership. PPAs charge per kWh generated (typically $0.12–$0.18/kWh), while leases charge a fixed monthly fee. PPAs can save more in low-production months but cost more in high-production months. Over 25 years, PPAs and leases produce nearly identical total costs for most homeowners.

What is NPV and why does it matter for solar financing?

NPV (Net Present Value) discounts future cash flows to today’s dollars using a discount rate (typically 4–6%). A positive NPV means the investment creates value. For solar, NPV captures the time value of money: savings 20 years from now are worth less than savings today. Cash purchases produce the highest NPV. Leases and PPAs often show negative NPV when compared to utility-only scenarios at high discount rates.

When is a solar lease actually the better choice?

A solar lease makes sense when: (1) you cannot afford any upfront cost and do not qualify for loans, (2) you plan to move within 5–7 years and want to avoid ownership risk, (3) your roof condition is marginal and you want the provider to assume equipment risk, (4) you value hassle-free maintenance over maximum savings, or (5) you live in a low-utility-rate market where ownership payback exceeds 15 years.

What are hidden costs in solar leases and PPAs?

Hidden costs include: annual payment escalators (2.0–2.9%) that compound over 20–25 years, early termination penalties of $15,000–$25,000, roof work restrictions requiring provider approval for $500–$2,000 removal fees, buyout clauses set at “fair market value” favorable to the provider, and performance guarantees that exclude certain failure modes. Always read the full contract before signing.

How do I calculate my own solar lease vs buy numbers?

Start with your annual electricity usage and local utility rate. Get quotes for all four options: cash, loan, lease, and PPA. Model 25 years of costs using a 2.5% utility escalator and 0.5% system degradation. Apply a 4–6% discount rate for NPV. Include maintenance for owned systems ($2,400 over 25 years) and lease escalators (2.0–2.9%). Compare total NPV, not just year-one savings.

Does the 30% federal tax credit still exist for solar in 2026?

No. The 30% federal residential Investment Tax Credit (Section 25D) expired on December 31, 2025. Homeowners who installed solar in 2025 could still claim it. For 2026 installations, no federal residential tax credit exists. Some states still offer rebates and credits. Lease and PPA providers can access the commercial ITC (Section 48E) through 2027.