Quick Answer

Effective solar financing pitches contrast monthly loan payment vs current utility bill: 'Your bill is $245. The loan payment is $189. You're saving $56/month from day one.' Close on the question: 'Would you rather pay your utility forever, or own your power in 12 years?' Always quote payment vs payment — never total cost vs total cost.

Generic solar pitch scripts will not close a financing deal. Most online “scripts” are situational openers. They tell you how to knock a door or start a cold call. They do not tell you what to say when a homeowner asks how much the loan payment is.

Effective solar financing pitches contrast monthly loan payment vs current utility bill: “Your bill is $245. The loan payment is $189. You’re saving $56/month from day one.” Close on the question: “Would you rather pay your utility forever, or own your power in 12 years?” Always quote payment vs payment — never total cost vs total cost.

The residential solar market changed in 2026. The Section 25D federal tax credit expired at the end of 2025. Reps can no longer default to “you get 30% back.” Now the pitch lives or dies on financing mechanics. Loan rates, lease escalators, PPA terms, and cash ROI are the new battleground.

This guide gives you 7 word-for-word financing pitch scripts. Each script is organized by financing type. Each includes data anchors, compliance guardrails, and a same-day close path. Use them as-is or adapt them to your market.

TL;DR — Solar Financing Pitch Scripts

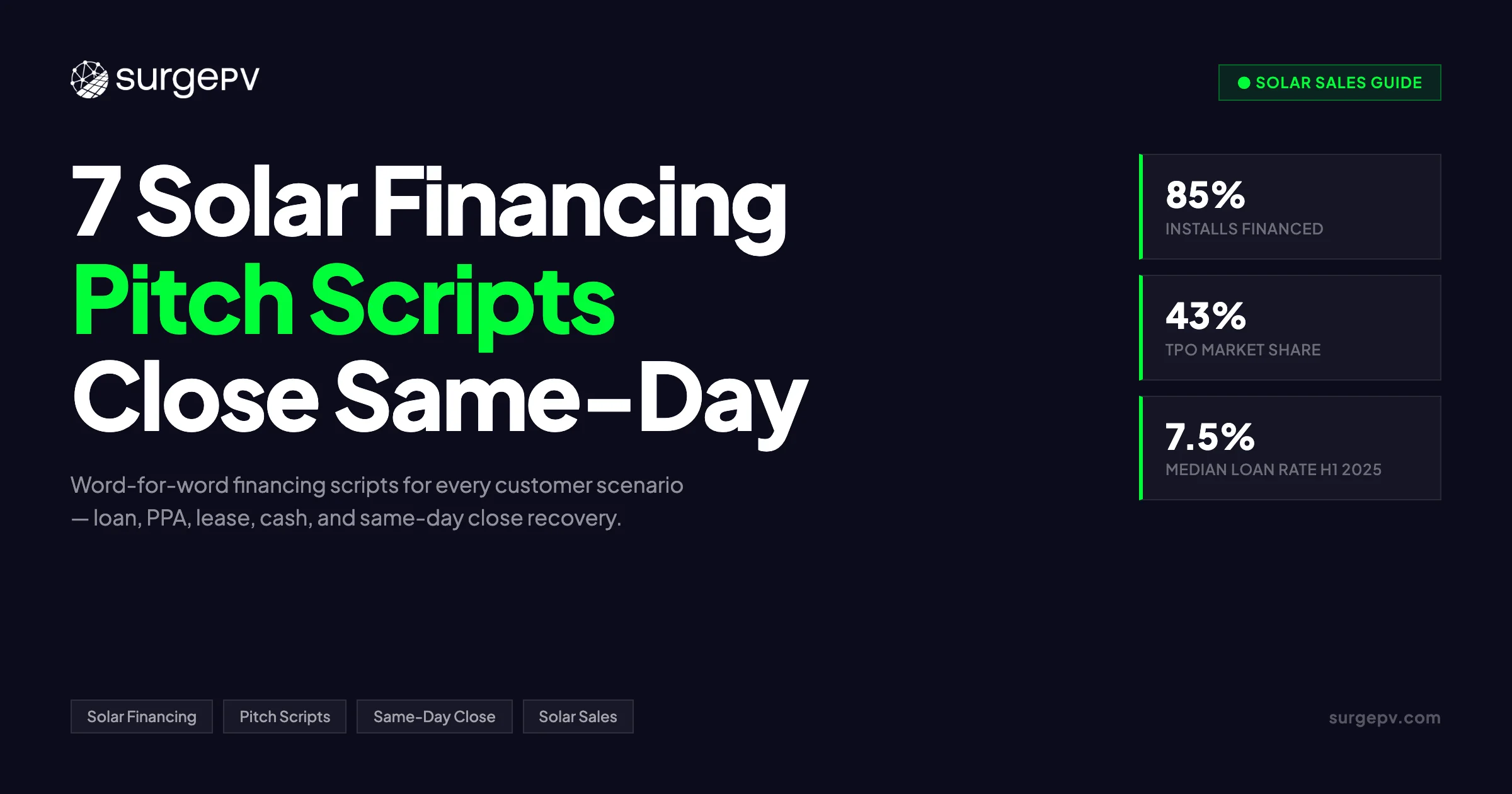

7 word-for-word scripts for loan, lease, PPA, cash, C-PACE, bill comparison and objections. NREL data shows loan customers save up to 30% versus lease customers. US solar customer acquisition costs sit at $0.35 per watt — 7× higher than Australia. Clear financing dialogue moves close rates from 25% to 35% faster than any other lever.

See our guide on Agricultural Solar Case Study for more. Read more about Floating Solar Farms France. For Australia-specific compliance details, see Australia comparisons/lgc-vs-stc.

In this guide:

- What changed in solar financing after the residential tax credit expired

- Script 1: Solar loan pitch script for homeowners

- Script 2: Zero-down solar lease pitch script

- Script 3: Solar PPA pitch script for same-day closes

- Script 4: Solar cash purchase pitch script

- Script 5: Commercial C-PACE financing pitch script

- Script 6: The solar bill comparison script

- Script 7: Solar financing objection rebuttal script

- Same-day close mechanics that make financing pitches stick

- Compliance guardrails every rep should follow

The State of Solar Financing in 2026: What Reps Must Know Before the Pitch

Residential solar financing shifted in 2026 after the Section 25D tax credit expired. Customer-owned systems made up nearly half of installs in early 2025. Third-party ownership grew as the deadline approached. Loan rates hover near 7.5%. Soft costs eat 65% of project value. Reps who master financing mechanics close 25–35% of first appointments.

The US residential solar market has two main ownership types. Customer-owned systems include cash and loan deals. Third-party ownership includes leases and PPAs. In the first half of 2025, customer-owned systems made up nearly half of all installs.

SEIA and Wood Mackenzie report 4,647 MWdc of residential solar in 2025. That is down 2% year-over-year. Wood Mackenzie forecasts a 19% contraction in 2026. The residential tax credit expired. The market is tighter.

RMI analysis from 2020 shows customer acquisition cost in the US sits at about $0.35 per watt. Australia hits $0.05. That 7× gap explains why soft costs dominate US project economics. Sales and marketing eat most of the margin.

Financing mix shifted in late 2025. Homeowners rushed to secure customer-owned systems before the tax credit expired. Many still moved toward zero-down options as rates stayed high. Third-party ownership remained eligible for the ITC.

EnergySage reports median quoted system price was $2.48 per watt in late 2025. EIA data shows the average US electric bill runs $144 per month. Utility rates climbed 2.8% annually over the last decade. These are your anchors. Not panel efficiency. Not inverter brands. Monthly payment versus monthly bill.

NREL’s 2015 “Banking on Solar” analysis found that loan customers save up to 30% compared to lease customers. Loan LCOE is 19–29% lower than PPA LCOE. Cash still wins outright. Most homeowners do not have $25,000 in savings.

Your job is to make the financing path feel obvious. The script does that by starting with numbers the homeowner already knows. Their bill. Their rate hikes. Their need for a fixed payment.

HubSpot’s 2025 State of Sales report shows 35% of lost deals die on poor value for money. Another 37% die on poor product fit. The script fixes both. It shows transparent numbers. It names the rate. It names the fee. It does not hide the escalator.

A 2025 Gartner survey found that 74% of B2B buying teams show “unhealthy conflict.” Residential solar is not B2B. Buying committees still exist. Spouses. Adult children. Co-signers. A financing script answers their specific questions. That prevents the “we need to think about it” stall.

Industry data shows 80% of sales need 5 or more follow-ups. Yet 44% of reps give up after one try. A same-day financing close eliminates that risk. It captures the decision while emotion and math are both fresh.

That is the market reality. Here are the scripts.

Script 1: Solar Loan Pitch Script for Homeowners

This script anchors on monthly payment versus utility bill. It names the loan rate and dealer fee. It isolates the decision on savings, not panels. Use it after you review the homeowner’s last 12 months of bills. FICO above 680 gets the best rates.

Rep: “Most homeowners in this area pay about $144 a month to the utility. That rate goes up 2% to 3% every year. Your solar loan payment is $127 a month. Fixed. For 25 years. Does that number work for your budget?”

Homeowner: “It sounds good. What is the interest rate?”

Rep: “The rate is 7.49%. The dealer fee is 18%. That fee is wrapped into the loan. You pay zero out of pocket today. Over 25 years you save $31,000 compared to staying with the utility. I can show you that on screen right now.”

Homeowner: “What if I sell the house?”

Rep: “The loan transfers to the new owner. Or you pay it off at closing. Either way, the panels add value. Lawrence Berkeley Lab data shows solar adds about $15,000 to resale value. You are not stuck. You are ahead.”

Use this script when the homeowner has good credit. FICO above 680 gets the best rates. Pull a soft credit check before the appointment if your financier allows it.

Lead with the monthly payment. Not the system size. Not the panel count. Homeowners buy cash flow. They do not buy kilowatts.

Name the rate and the fee. Hiding the dealer fee kills trust. Sunrun and Trinity Solar complaints show that surprise fees are the top BBB issue. Transparency is your edge.

Show the numbers live. Use solar proposal software to model the loan side-by-side with their utility bill. Static PDFs feel like guesses. Live tools feel like facts.

End with the transfer question. Most homeowners ask it. Answer before they stall. The transfer option removes the biggest psychological barrier to a 25-year obligation.

If the rate is above 9%, pivot. Offer a larger down payment to buy points. Or move to a lease if the homeowner has sub-680 credit. Do not force a loan that eats all their savings.

NREL’s 2015 analysis shows loan LCOE beats PPA LCOE by 19–29%. That gap is your rebuttal if the homeowner compares your loan to a neighbor’s lease. The loan builds equity. The lease does not.

In post-ITC markets, the loan pitch changes. You cannot lead with a 30% tax credit. You lead with rate stability. The utility goes up. Your loan payment does not.

Script 2: Zero-Down Solar Lease Pitch Script

This script is for homeowners with sub-680 credit or zero savings. The lease payment is fixed at $100 to $150 per month. The homeowner saves 10% to 20% on day one. They do not own the system. The provider does. Be honest about modest savings.

Rep: “You pay nothing today. Zero down. Zero install cost. Your lease payment is $115 a month. Fixed. The utility would charge you $144 this year. Next year it will be $148. In year 10 it hits $185. Your lease stays at $115.”

Homeowner: “Do I get the tax credit?”

Rep: “The provider takes the tax credit. That is why they can offer zero down. You get the lower monthly bill and the maintenance coverage. If the panels underperform, they pay the difference. You are protected.”

Homeowner: “What happens when the lease ends?”

Rep: “You have three choices. Renew the lease. Buy the system at fair market value. Or ask them to remove it at no cost. Most people renew. By then the system is paid off and the renewal rate is usually under $50.”

Use this script when the homeowner cares about risk transfer. Leases shift performance risk to the provider. That is valuable for conservative buyers.

Be honest about savings. EcoWatch secret shopper data shows Trinity Solar lease customers save only about $5,000 lifetime. Loan customers save $26,500. Cash customers save $31,500. Do not oversell the lease. Promise modest savings and deliver them.

Sunrun data from late 2025 shows 94% of new customers choose a PPA or lease. The lease is not dead. It is a tool for specific credit profiles.

If the homeowner asks about home sale, answer directly. The lease transfers. The buyer must qualify. Some buyers hesitate. Disclose this early. It prevents surprises at closing.

Name the escalator. Some leases include a 2.9% annual escalator. Name it. Show the math. A $115 payment with a 2.9% escalator hits $154 in year 10. Still beats the utility. But the homeowner must know.

Script 3: Solar PPA Pitch Script for Same-Day Closes

This script sells kilowatt-hours, not panels. The homeowner pays per kWh produced. The rate is 10% to 20% below utility. There is no loan. There is no lease payment. The PPA is pure service. It is the fastest path to a same-day close.

Rep: “The PPA is simple. You buy the power. Not the panels. The rate is $0.13 per kWh. Your utility charges $0.166. That is a 22% discount on every unit you use. You pay only for what the system makes. Nothing else.”

Homeowner: “What if the system makes too much?”

Rep: “Excess goes to the grid. You get a credit. Net metering still applies in this state. In month one your bill drops. No loan application. No lien. Just a lower rate.”

Rep: “I can turn this on today. The install crew is booked three weeks out. If you sign now, I lock your rate before the utility raises theirs next quarter. Shall we start the paperwork?”

The PPA is the fastest same-day close. There is no credit check. No debt-to-income calculation. The decision is simple math.

Use this when the homeowner is rate-sensitive but debt-averse. Retirees often prefer PPAs. They do not want a 25-year loan at age 68.

Name the PPA escalator. Most PPAs include a 2.9% annual increase. Show the year-by-year comparison against utility inflation. Even with the escalator, the PPA wins for 20 years.

PPAs fit the post-ITC world. The provider keeps the commercial credit under Section 48E. The homeowner gets the savings. Everybody wins.

If your state has weak net metering, adjust the script. Show the bill with the true-up. Do not promise zero bills. Promise lower bills.

Add a backup savings clause. “If your usage drops, your PPA bill drops. If your usage rises, you still pay $0.13. The utility would charge you $0.18 for that same extra unit.” That frames the PPA as downside protection. Also see: Us Residential Solar Market Trends 2026.

Use this script on warm summer days. High AC bills create pain. Pain creates urgency. The PPA offers instant relief with no debt.

Script 4: Solar Cash Purchase Pitch Script

Cash delivers the highest lifetime savings. NREL data shows cash customers save about $31,500 over 25 years. This script targets homeowners with liquid savings and low risk tolerance. No rates. No fees. No escalators. Lead with the payback period. It builds confidence in the first 60 seconds.

Rep: “The system costs $24,800. You pay it once. You own it. There is no interest. No dealer fee. No monthly payment to a bank. Your only bill is a $10 connection fee to the utility.”

Homeowner: “That is a lot of money upfront.”

Rep: “It is. Here is the return. You currently pay $1,728 a year to the utility. The system covers 98% of that. Your payback is 8.7 years. After that, electricity is nearly free for 16 years. Total 25-year savings: $31,500. That is a 12.4% annual return. Show me a CD that pays that.”

Homeowner: “What about maintenance?”

Rep: “Panels have a 25-year warranty. Inverters are 12 years. I will include a 10-year monitoring plan. Your total maintenance risk is under $2,000 over 25 years. I will put that in writing.”

Cash buyers care about payback period. Lead with it. Do not bury it on page 3 of a proposal. State it in the first 60 seconds.

Use generation and financial tool to model the payback in real time. Change the discount rate. Show conservative and optimistic scenarios. Cash buyers love sensitivity analysis.

The cash pitch also works for HELOC customers. Some homeowners borrow against equity at 6%. That is cheaper than solar loan dealer fees. Mention it if they are curious.

In post-ITC markets, cash buyers still win. They lost the 30% credit. But they also avoid interest. Their net savings remain the highest of any ownership option.

If the homeowner hesitates, offer a hybrid. 50% down. 50% loan. It cuts interest costs while preserving cash reserves.

Cash also speeds up the sale. No lender approval. No credit check delays. The install starts as soon as the permit clears. For homeowners who value control, that speed beats the interest savings.

Mention property tax benefits where they apply. Some states exempt solar from property tax assessment. The home value rises. The tax bill does not. Put that in the proposal.

Script 5: Commercial C-PACE Financing Pitch Script

C-PACE covers 100% of project cost in 40 US states. Repayment attaches to the property tax bill over 20 to 25 years. This script targets building owners and facility managers. Rates run 5.5% to 6.5%. The payment stays with the building if you sell.

Rep: “C-PACE is not a loan. It is a property tax assessment. It covers the full system cost. Zero upfront capital. The repayment stays with the building. If you sell, the next owner takes over the payments.”

Facility Manager: “What is the rate?”

Rep: “Rates are typically 5.5% to 6.5%. Terms run 20 to 25 years. The solar savings start in month one. The assessment payment is often lower than the utility savings. You are cash-flow positive from day one.”

Facility Manager: “What about non-recourse?”

Rep: “C-PACE is non-recourse to the owner. It does not appear on your balance sheet as debt. It does not trigger loan covenants. RMI calls it a customer acquisition tool, not just financing. It opens doors that traditional credit closes.”

Use this script for commercial properties with strong tax assessments. Office buildings. Warehouses. Retail centers. The building must be in a C-PACE-enabled district.

Anchor on cash flow, not payback. CFOs care about monthly operational savings. They care about EBITDA impact. C-PACE preserves capital for core business investments.

RMI notes that US commercial customer acquisition costs are high. C-PACE lowers friction. It removes the capex barrier. That makes it a sales tool first and a finance product second.

Be clear on eligibility. C-PACE requires lender consent if there is an existing mortgage. Some lenders refuse. Check before you pitch.

For UK and EU consultants, mention green asset financing. The logic is the same. The names differ. SurgePV’s solar design software models C&I cash flow in both regions. Read more about Battery Solar System Design UK. For United Kingdom-specific compliance details, see United Kingdom comparisons/mcs-vs-non-mcs.

C-PACE also works for retrofits. LED lighting. HVAC upgrades. Battery storage. Bundle them with solar. The assessment covers the whole package. CFOs love one payment for multiple upgrades. Read Adding Battery Storage Services for a complete walkthrough.

Mention the transferability again at the close. “You are not stuck with this building for 20 years. The assessment moves.” That removes the long-term commitment objection before it arises.

Script 6: The Solar Bill Comparison Script

This script shows the utility bill and the solar financing payment side-by-side. It is the most powerful same-day close tool. Homeowners believe their own bills. They do not believe your brochure. Show three columns: utility, loan, and lease. Let the homeowner read the numbers in silence.

Rep: “Pull out your last electric bill. I am going to show you something. You paid $156 last month. In July you paid $198. The 12-month average is $167. Here is what solar does.”

Open your laptop. Use your solar proposal software. Show three columns. Utility. Solar loan. Solar lease.

Rep: “Column one is your utility. Year one: $167 per month. Year 10: $218. Year 20: $289. Total 25-year spend: $71,400. Column two is the loan. $139 per month. Fixed. Total 25-year spend: $41,700. You keep $29,700.”

Let the homeowner read the numbers. Silence is your friend. Do not talk over the math.

Rep: “Column three is the lease. $119 per month. Fixed. Total 25-year spend: $35,700. You keep $35,700. Which column feels right to you?”

The question forces a choice. Not a yes-no. A this-or-that. It is called an alternative close. It cuts decision fatigue.

Use Clara AI to generate the comparison in under 30 minutes on-site. Do not say “I will email this later.” Later kills deals. Industry data shows 80% of sales need 5 follow-ups. Yet 44% of reps quit after one. Show the numbers now. Close today.

If the homeowner picks the loan, ask for a soft credit pull. If they pick the lease, print the agreement. If they are unsure, show the cash option. Always have all three ready.

Body language matters during the silence. Do not fidget. Do not check your phone. Sit still. Let the homeowner think. Confidence in silence signals confidence in the numbers.

If they ask about inflation, show it. Utility inflation averages 2.8% annually. Solar financing is fixed. The gap between the two lines grows every year. That visual is more powerful than any verbal claim.

Use this script at the kitchen table. Not the front porch. The homeowner needs their bills. They need a flat surface for the laptop. They need to feel safe. The kitchen is where financial decisions happen.

Script 7: Solar Financing Objection Rebuttal Script

This script handles the four most common financing objections. “Too expensive.” “I need to think about it.” “I need to talk to my spouse.” “My credit is bad.” Each rebuttal isolates the real concern. Do not argue. Isolate. Then solve.

Objection: “Solar is too expensive.”

Rep: “Too expensive compared to what? Your current bill, or the cash price?” Wait for the answer. If they say the bill, show the monthly payment. If they say the cash price, move to a loan or lease.

Objection: “I need to think about the financing.”

Rep: “Of course. What specifically are you weighing? The monthly payment, the loan term, or something else?” Isolate the variable. If it is the payment, re-run the numbers with a longer term. If it is the term, show the total savings difference.

Objection: “I need to talk to my spouse.”

Rep: “Absolutely. What is their biggest concern usually — the monthly cost or the long-term commitment?” Get the objection secondhand. Address it before they leave. Offer to schedule a 10-minute call with both tonight.

Objection: “My credit is bad.”

Rep: “How bad is bad? FICO above 600 still gets a loan. Below 600, we have a lease. No credit check. Same savings. Let me show you.”

Do not argue. Isolate. Every objection is a question wearing a mask. Your job is to unmask it.

HubSpot’s 2025 State of Sales report found that 35% of deals die on poor value for money. Price usually means value. If the homeowner understood the savings, price would not matter. Use the bill comparison script first. Then use this rebuttal script second.

Train on these scripts before real calls. Practice the words. Do not improvise. Improvisation kills consistency.

Stop losing deals to “I need to think about it”

Reps who run live bill comparisons on-site close 35% of first appointments. Reps who email PDFs later close under 20%.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

How to Close Solar Financing Deals on the Same Day

Same-day closes need live bill comparison, financing pre-qualification, and a clear low-risk next step. Reps who use proposal software on-site close faster than reps who email PDFs later. Speed to numbers beats speed to pitch. Stop talking once the homeowner says yes. Send a one-page summary within one hour.

Same-day closes need three things. Live bill comparison. Financing pre-qualification. A clear low-risk next step. Reps who use proposal software on-site close faster than reps who email PDFs later.

Bring a tablet or laptop. Show the homeowner their roof on satellite imagery. Drop panels in real time. Run the shade analysis. Then open the financing tab. Shadow analysis software identifies shading issues before installation. Read [Solar Shading Analysis Guide](/blog/solar-shading-analysis-guide) for a complete walkthrough.

Pre-qualify before you arrive. Most financiers offer a soft credit check link. Text it to the homeowner the day before. Know their approved tier before you shake hands.

Use the alternative close. Do not ask “Do you want to move forward?” Ask “Does the loan or the lease feel better to your budget?” The former invites a no. The latter invites a choice.

Have the paperwork ready. Digital signature platforms let you start the loan application on the spot. Lease documents print in minutes. Do not let logistics kill momentum.

Set a deadline. “If we start this week, I can secure the install crew for the 15th. Next week they are booked until the 30th.” Deadlines create urgency without pressure.

Follow up in 24 hours if they do not sign. Not 48. Not 72. One day. Send a one-page summary. Not a 12-page proposal. One page. Three numbers. Monthly payment. Total savings. Payback period.

The average sales win rate is 21%. Top solar teams hit 35%. The gap is not product knowledge. It is speed. Speed to numbers. Speed to trust. Speed to close.

Speed also means knowing when to stop talking. Once the homeowner says yes, stop selling. Pull out the tablet. Start the application. Every extra word adds doubt.

Send the summary within one hour if possible. Not a proposal. A summary. One page. Three numbers. That speed signals professionalism. It also locks in the verbal commitment before doubt creeps in.

Practice the transition from pitch to paperwork. “Great. Let me pull up the application. This takes about four minutes.” Smooth transitions reduce buyer’s remorse. Jerky transitions create cold feet.

Compliance Guardrails Every Solar Financing Pitch Needs

The CFPB documented high-pressure tactics and tax credit misrepresentation in a 2024 report. Transparent scripting is a compliance safeguard. Never promise a zero bill. Never hide the dealer fee. Always disclose the escalator. Name every fee in writing. Verbal promises do not hold up in court.

Start every pitch with a script. Not a vibe. Scripts create consistency. Consistency creates defensibility. If a customer complains, you can show exactly what you said.

Never promise a zero electric bill. Grid connection fees remain. Usage spikes happen. The CFPB’s top complaint: “I was told I would not have to pay an electric bill and now I pay more.” Avoid that sentence entirely.

Name every fee. Dealer fees. Origination fees. Escalators. Prepayment penalties. Put them in writing. Verbal promises do not hold up in court.

Do not misrepresent tax credits. The residential ITC expired. Do not mention a 30% federal credit unless you are selling commercial under Section 48E. If you sell in the UK, mention zero VAT on batteries. Do not make up US incentives.

Record your calls if local law allows. Review them weekly. Coached reps improve faster. You do not need enterprise software. A shared folder and a checklist works.

Document savings assumptions. Utility inflation rate. System degradation. Net metering changes. Put them in the proposal. Homeowners sign them. That signature protects you.

Trinity Solar and Sunrun both face BBB complaints about misleading savings. Your defense is documentation. Show your work. Let the numbers speak.

Train reps on these scripts monthly. Roleplay the objections. Test the rebuttals. Solar sales is a skill. Skills decay without practice.

Keep a complaint log. Track every objection. Track every refund request. Patterns emerge. If three homeowners in one month complain about the same fee, your script is broken. Fix it.

Update scripts when laws change. The ITC expired. Net metering rules shift by state. PACE eligibility expands. A script from 2024 is a liability in 2026. Review quarterly.

Share wins in team meetings. Which script closed the deal? Which rebuttal turned a no into a maybe? Peer learning is faster than top-down training. Reps trust reps.

Conclusion

- Audit your current script. Does it name the rate, the fee and the escalator? If not, rewrite it today.

- Pick one financing type. Practice the script out loud 10 times before your next appointment.

- Open your solar proposal tool. Build a side-by-side comparison template for loan, lease and utility. Use it on every call.

Frequently Asked Questions

How do you pitch solar financing to homeowners?

Start with their current electric bill. Show the monthly payment for a solar loan, lease or PPA side-by-side against their utility rate. Anchor on total 25-year savings, not panel specs. Use a live proposal tool so the homeowner can see the numbers change in real time.

What are the disadvantages of a solar loan?

Solar loans carry interest that reduces net savings compared to cash. Homeowners with sub-680 credit scores may face rates above 9%. The loan is also attached to the property, which can complicate a sale if the buyer does not want to assume it.

What do you say when a customer says solar is too expensive?

Isolate the objection first. Ask: “Too expensive compared to your current electric bill, or compared to paying cash upfront?” Then show the financed monthly payment against their average utility bill. If the solar payment is lower, the issue is not cost. It is cash flow.

Is it better to finance or pay cash for solar?

Cash delivers the highest lifetime savings. NREL data shows loan customers still save up to 30% versus lease customers over 25 years. For homeowners who cannot pay cash, a zero-down loan with a fixed rate below utility inflation is usually the better financial move.

How do solar sales reps close deals same day?

Same-day closes require three things: a live bill comparison the homeowner can verify, financing pre-qualification before the appointment, and a clear next step that feels low risk. Reps who use proposal software to model scenarios in front of the customer close faster than reps who email a PDF later.