Quick Answer

Europe's solar policy framework in 2026 rests on three pillars: RED III (42.5% renewable target by 2030), REPowerEU (€210 billion for energy independence), and the Net Zero Industry Act (750 GW solar target). National programs include Germany's EEG, France's OA, Italy's Ecobonus, and Spain's IDAE grants. The EU Solar Strategy targets 600 GW by 2030.

Europe’s solar policy is moving faster than at any point in its history. The EU has set a 750 GW solar capacity target for 2030, the Carbon Border Adjustment Mechanism is reshaping panel import economics, and RED III is forcing every member state to overhaul its permitting framework simultaneously. For Europe-specific compliance details, see Europe solar compliance.

Europe’s solar policy framework in 2026 rests on three pillars: RED III (42.5% renewable target by 2030), REPowerEU (€210 billion for energy independence), and the Net Zero Industry Act (750 GW solar target). National programs include Germany’s EEG, France’s OA, Italy’s Ecobonus, and Spain’s IDAE grants. Also see: solar panel ROI in Italy. Also see: Germany solar subsidies. Also see: France solar feed-in tariffs. Also see: Spain net metering.

Europe’s solar policy framework in 2026 rests on three pillars: RED III (42.5% renewable target by 2030), REPowerEU (€210 billion for energy independence), and the Net Zero Industry Act (750 GW solar target). National programs include Germany’s EEG, France’s OA, Italy’s Ecobonus, and Spain’s IDAE grants. The EU Solar Strategy targets 600 GW by 2030. See our guide on Agricultural Solar Case Study for more. For the latest details on Italy, see Commercial Rooftop Solar Case Study Italy.

For solar installers, EPCs, and project developers operating across Europe, the difference between a project that closes in 9 months and one that stalls for 3 years often comes down to understanding exactly which regulation applies, when, and in which jurisdiction.

This guide covers the complete European solar policy framework as of early 2026 — from the EU-wide directives that set the framework to country-level implementation details, the CBAM solar panel trade question, and actionable steps for installers navigating a rapidly evolving regulatory environment.

TL;DR — EU Solar Policy 2025–2026

Key numbers: 750 GW solar target by 2030; 42.5% renewable share target under RED III; 12-month permitting cap in Renewable Acceleration Areas; CBAM transition phase 2023–2026 (reporting now, payments from 2026); no active anti-dumping duties on Chinese panels since September 2023. Every member state must transpose RED III by mid-2025. Installers who align projects with Renewable Acceleration Areas and EU Innovation Fund criteria will access the fastest permitting and deepest financing.

In this guide:

- Latest EU solar policy updates: what changed in 2025 and 2026

- CBAM and solar panels — full explainer for European installers

- RED III: what the revised Renewable Energy Directive means in practice

- Fit for 55, REPowerEU, and the 750 GW solar target

- Net-Zero Industry Act and EU solar manufacturing support

- Emergency Solar Permit Regulation and permitting acceleration

- Country-by-country policy comparison: Germany, France, Spain, Italy, Netherlands

- Anti-dumping duties on Chinese panels — history and current status

- Grid integration policies across the EU

- How to stay compliant and competitive in 2026

Latest EU Solar Policy Updates: 2025–2026

For anyone tracking EU solar policy updates today, this section summarises the current status of every major regulatory development as of March 2026. Read Solar Racking Design Guide for a complete walkthrough.

EU Solar Policy Status — March 2026

| Policy / Regulation | Status | Key Deadline |

|---|---|---|

| RED III transposition | In progress — most member states mid-transposition | Member state deadline: mid-2025 (some delayed) |

| CBAM transition phase | Active — reporting obligations in force | Full financial obligations: 1 January 2026 |

| Emergency Solar Permit Regulation | Active — extended to end-2026 | 3-month permitting cap for specific projects |

| Net-Zero Industry Act | In force — implementing acts being developed | Strategic project designation rolling |

| EU ETS Phase 4 reforms | Active — carbon price stabilising €60–€75/tonne | Linear reduction factor increased annually |

| REPowerEU solar rooftop mandate | Member states implementing | Commercial/public buildings: 2027; residential: 2029 |

| NECP updates (2024–2030 cycle) | Submitted — Commission reviewing | Final assessment: 2025 |

Key Changes Since 2024

RED III transposition underway. The revised Renewable Energy Directive entered into force in November 2023 with an 18-month transposition window. Most member states are now in mid-transposition, with Germany, Spain, and France furthest ahead in implementing the Renewable Acceleration Area framework.

CBAM reporting now mandatory. Since October 2023, importers of covered products must submit quarterly CBAM reports. Financial payments begin 1 January 2026. The European Commission published its first review of CBAM product list expansion in early 2025 — photovoltaic modules remain under active assessment for inclusion.

Emergency permitting cap extended. The Council Regulation on emergency permitting, initially adopted in December 2022 to fast-track solar deployment, was extended through end-2026. Projects in designated zones benefit from a 3-month maximum permitting timeline.

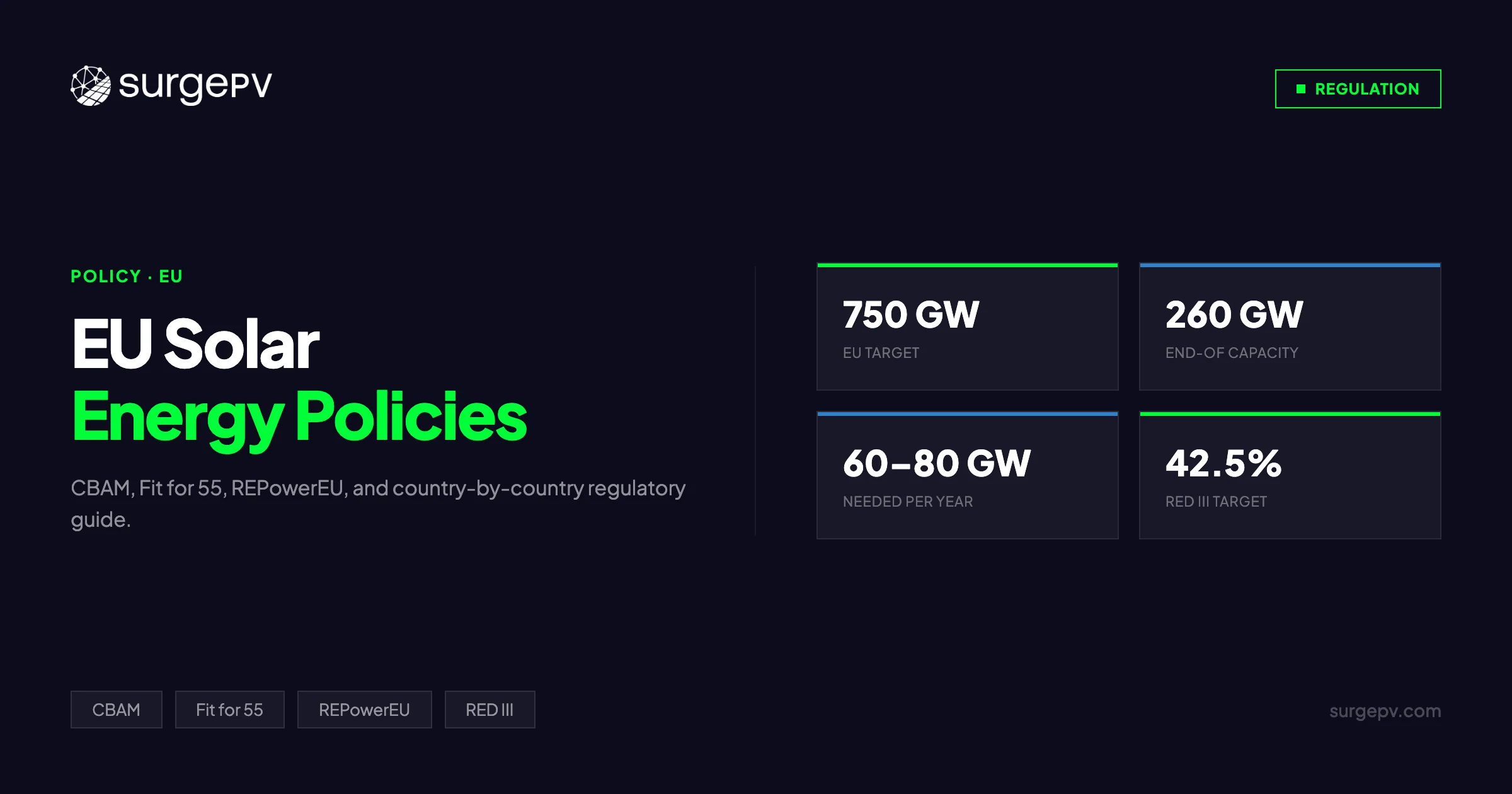

EU solar capacity crossed 330 GW. Europe surpassed 330 GW of installed solar capacity in 2025, driven by record deployment in Germany, Spain, and Poland. Annual additions reached 67 GW in 2024, but the 750 GW target requires sustaining 60–80 GW annually through 2030.

Key Takeaway — The 2026 Policy Threshold

2026 is a structurally important year for European solar policy: CBAM financial obligations begin, RED III transposition should be complete, and most member states’ updated NECPs take full effect. Projects initiated in 2025–2026 will operate under a materially different regulatory and cost environment than projects commissioned before 2023.

CBAM and Solar Panels: What European Installers Need to Know

The Carbon Border Adjustment Mechanism is the single most consequential trade policy development for European solar since the anti-dumping duties debate of 2012–2023. Understanding CBAM is now a core competency for anyone sourcing panels across EU borders.

What Is CBAM?

CBAM is the EU’s carbon border tax, designed to prevent “carbon leakage” — the risk that EU companies move production to countries with weaker carbon pricing to avoid EU ETS costs. It applies a carbon price to imports equivalent to what EU producers would pay under the EU ETS.

CBAM entered its transitional phase on 1 October 2023. Full financial obligations begin 1 January 2026.

The mechanism works as follows:

- An importer brings goods into the EU that were produced in a non-EU country

- The importer must purchase CBAM certificates equivalent to the embedded carbon in those goods

- Certificate prices track the EU ETS carbon price (currently €60–€75 per tonne of CO₂)

- If the exporting country already charges a carbon price for that production, the importer receives a credit

Which Products Are Currently Covered by CBAM?

The initial CBAM regulation (Regulation EU 2023/956) covers five product sectors:

- Iron and steel

- Aluminium

- Cement

- Fertilisers

- Electricity

- Hydrogen (added in final text)

Solar panels (photovoltaic modules) are not currently included in the CBAM product list.

However, the European Commission committed in the CBAM regulation to review and expand the product list by 2026. Given that solar panel production — dominated by Chinese manufacturers — is energy-intensive and produces significant embedded carbon, photovoltaic modules are among the most discussed candidates for CBAM expansion.

CBAM Indirect Impact on Solar Today

Even before direct CBAM coverage of solar panels, CBAM is already affecting solar costs in two ways:

Aluminium framing. Solar panel frames and mounting systems are made primarily from aluminium — a current CBAM-covered product. Aluminium imported from producers in countries without equivalent carbon pricing now carries a CBAM surcharge. This adds €2–€8 per panel to import costs, depending on the aluminium content and origin country’s carbon pricing level.

Steel racking and mounting. Steel, also CBAM-covered, is used extensively in ground-mount and commercial rooftop racking systems. Steel racking imports from non-EU countries are already subject to CBAM obligations.

Pro Tip — Track CBAM Certificates for Aluminium Now

If your mounting systems or panel frames contain imported aluminium, your supplier should be providing embedded carbon documentation. Request carbon intensity certificates from suppliers proactively — these are already legally required for CBAM reporting and will be essential for cost modelling if panels themselves are added to the CBAM list.

Which Solar Panel Origins Are Most Affected by CBAM?

CBAM costs depend on the carbon intensity of manufacturing in the origin country and the carbon price differential between that country and the EU.

| Country of Origin | Manufacturing Carbon Intensity | CBAM Exposure (if panels added) |

|---|---|---|

| China | High (coal-heavy grid) | High — significant CBAM surcharge likely |

| India | Medium-high | Medium-high exposure |

| Vietnam | Medium | Medium exposure |

| EU-manufactured (Germany, France) | Low (low-carbon grid mix) | Minimal — domestic production exempt |

| United States | Medium | Medium — depends on IRA-driven grid changes |

Chinese solar panels, which represent approximately 80–85% of EU solar imports, are produced with a grid electricity mix that is still heavily coal-dependent in manufacturing regions. If CBAM coverage were extended to photovoltaics, it could add $15–$35 per panel in carbon cost based on current carbon intensities and EU ETS prices.

CBAM Transition Phase (2023–2026) — What Is Required Now

During the transition phase (October 2023 – December 2025), CBAM obligations are reporting only. There are no financial payments due yet.

Transition phase obligations for importers:

- Submit quarterly CBAM reports via the EU CBAM Transitional Registry

- Report the quantity of covered goods imported

- Report the embedded greenhouse gas emissions (or use default values if actual data unavailable)

- No CBAM certificates need to be purchased during this phase

From 1 January 2026 — full obligations begin:

- Purchase CBAM certificates for all covered product imports

- Certificate prices track weekly EU ETS auction clearing prices

- Annual CBAM declaration submitted by 31 May each year

- Third-party verification required for embedded emission calculations

Impact on Solar Installation Costs in Europe

For the materials currently covered (aluminium, steel), the cost impact is already being felt:

| Component | CBAM Exposure | Estimated Cost Impact per 100 kWp Project |

|---|---|---|

| Aluminium panel frames | Covered (aluminium) | +€400 – €1,200 |

| Steel ground-mount racking | Covered (steel) | +€800 – €2,500 |

| PV modules (China origin) | Not yet covered | €0 currently; €3,000 – €12,000 if added |

| Cable trays (steel) | Covered (steel) | +€100 – €400 |

For a 100 kWp commercial project using imported aluminium and steel components, CBAM is already adding approximately €1,200–€3,700 in costs — before any potential expansion to cover modules themselves.

How European Solar Installers Should Respond to CBAM

1. Audit your supply chain now. Identify every import in your standard BOM (bill of materials) that contains aluminium, steel, or cement. Request carbon intensity certificates from suppliers — they are legally required to provide this for CBAM-covered goods.

2. Build CBAM cost modelling into proposals. Solar design software that incorporates current component costs should be updated to reflect CBAM surcharges on aluminium and steel components. Projects financed over 10–20 years need cost models that account for potential panel-level CBAM expansion.

3. Evaluate EU-manufactured alternatives. EU-based solar manufacturers — primarily in Germany, France, and increasingly Poland — face no CBAM cost on their domestic production. The price gap between Chinese and European panels has narrowed significantly as CBAM, logistics costs, and the Net-Zero Industry Act subsidies combine. For projects where bankability and long-term cost certainty are priorities, EU-manufactured panels increasingly make financial sense.

4. Monitor the Commission’s CBAM review. The 2025–2026 product list review is the key decision point. Solar industry associations including SolarPower Europe are actively lobbying on CBAM expansion parameters. Track the European Commission’s official CBAM announcements at the DG TAXUD website.

5. Engage with your national CBAM authority. Each EU member state has designated a national CBAM authority. For large project portfolios, engaging proactively with your national authority helps clarify reporting obligations and prepares your business for the 2026 full implementation.

EU Solar Policy Framework: RED III, Fit for 55, and REPowerEU

Understanding the three overlapping EU legislative frameworks is essential for navigating European solar policy. They are complementary, not competing. Each addresses a different dimension of the same decarbonisation objective.

RED III: The Revised Renewable Energy Directive

RED III (Directive 2023/2413) is the cornerstone legal instrument for renewable energy deployment in the EU. It sets binding targets, establishes permitting rules, and defines the rights of energy communities.

Core RED III provisions for solar:

| Provision | Requirement |

|---|---|

| 2030 renewable target | 42.5% of gross final energy consumption from renewables (aspirational: 45%) |

| Renewable Acceleration Areas | Member states must designate RAAs; 12-month permitting cap applies |

| Non-RAA permitting | 24-month cap for large projects; 12-month cap for repowering |

| Rooftop solar mandate | Solar on new commercial/public buildings >250 m² by 2027; new residential by 2029 |

| Energy communities | Simplified access to grid, streamlined licensing |

| Corporate PPAs | Member states must remove barriers to corporate power purchase agreements |

What changed from RED II:

RED II set a 32% target. RED III raises this to 42.5% minimum, a 10.5 percentage point increase. This translates directly into dramatically larger national deployment requirements across all member states. The permitting acceleration provisions are the most immediate operational change — they shorten what has historically been a 3–5 year permitting timeline for large solar to a maximum of 12–24 months.

RED III full text — EUR-LexFit for 55: The Legislative Package

Fit for 55 is not a single regulation — it is a package of 13 interconnected legislative proposals designed to deliver a 55% reduction in net greenhouse gas emissions by 2030 compared to 1990. For solar, the most relevant elements are:

EU Emissions Trading System (EU ETS) reform. Carbon prices have risen from ~€25/tonne in 2020 to €60–€75/tonne in 2025. Every €10 increase in carbon price makes solar energy approximately 5–8% more cost-competitive versus gas-fired generation. Higher EU ETS prices are the most powerful indirect driver of solar investment in Europe.

Energy Efficiency Directive. The revised EED requires a 11.7% reduction in final energy consumption by 2030. Commercial and industrial solar self-consumption directly contributes to EED compliance. This adds a regulatory driver for rooftop solar in industry.

Revised EU ETS for buildings and transport (ETS II). From 2027, a separate carbon pricing mechanism applies to buildings and road transport fuel. This effectively creates a carbon cost for heating buildings with gas — making solar heat pump combinations significantly more attractive economically.

Renewable Energy Finance Mechanism. A cross-border financing mechanism that allows member states below their renewable targets to pay into a fund that finances solar projects in faster-moving member states, then receive statistical credit for the installed capacity.

REPowerEU: Solar as Energy Security

REPowerEU, announced in May 2022 following Russia’s invasion of Ukraine, reframed European solar deployment from a climate policy to an energy security imperative. This shift created consensus for emergency permitting acceleration that would have been politically impossible under climate-only framing. For UK-specific information, see Battery Solar System Design UK. For United Kingdom-specific compliance details, see United Kingdom comparisons/mcs-vs-non-mcs.

REPowerEU solar-specific measures:

- EU Solar Energy Strategy — published alongside REPowerEU, set a dedicated 600 GW solar target by 2030

- Mandatory rooftop solar — accelerated mandate for commercial and public buildings

- Solar skills initiative — EU-level training framework targeting 1 million certified solar installation professionals by 2027

- EU Solar Manufacturing Valleys — state aid framework for EU-based panel manufacturing

- Emergency permitting regulation — Council Regulation 2022/2577, initially for 18 months, extended multiple times

The 750 GW target explained:

The 750 GW number combines REPowerEU’s 600 GW solar target with Net-Zero Industry Act manufacturing goals and updated national NECP submissions. Some sources cite 600 GW, others 750 GW — both figures appear in official EU documents. The 750 GW headline is the figure most commonly used in SolarPower Europe and European Commission communications as of 2025.

At 330 GW installed at end-2025, Europe needs approximately 420 GW of additional capacity in five years — equivalent to everything built in Europe over the previous 45 years.

Further Reading

For Germany-specific subsidy details including KfW 442 battery grants, EEG feed-in tariffs, and Solarpaket I implementation, see our guide to Germany solar subsidies 2026.

Net-Zero Industry Act: EU Solar Manufacturing Support

The Net-Zero Industry Act (NZIA), adopted in 2024, targets 40% of EU annual clean technology deployment to come from EU-manufactured equipment by 2030. Solar photovoltaics are explicitly listed as a strategic technology.

What NZIA Does for Solar

Strategic project designation. Solar manufacturing projects can apply for NZIA strategic project status, which unlocks:

- Expedited permitting (18-month cap for strategic projects)

- Priority access to state aid frameworks

- Dedicated support from national investment promotion agencies

40% EU manufacturing target. By 2030, 40% of the solar capacity deployed annually in the EU should come from EU-manufactured modules. At 60–80 GW annual deployment, this means 24–32 GW of EU-manufactured panels per year — versus approximately 4–5 GW of EU manufacturing capacity currently.

IPCEI (Important Projects of Common European Interest) for solar storage. IPCEI frameworks allow member states to coordinate state aid for cross-border value chains. Battery storage associated with solar projects is eligible for IPCEI support, which allows subsidy stacking beyond normal state aid thresholds. See Adding Battery Storage Services for detailed guidance.

EU Solar Manufacturing Landscape 2026

| Country | Key Manufacturers | Capacity |

|---|---|---|

| Germany | Meyer Burger, Q Cells (Hanwha) | ~2 GW |

| France | Systovi, Voltec Solar | ~0.5 GW |

| Italy | Silfab, 3Sun (Enel) | ~0.8 GW |

| Others | Norway, Spain, Poland | ~0.7 GW |

| Total EU | ~4 GW |

The gap between 4 GW current EU manufacturing and the 24–32 GW NZIA target is large. Bridging it requires significant investment in new EU manufacturing — which NZIA and REPowerEU Solar Manufacturing Valleys are designed to catalyse.

For solar installers, the practical implication is that EU-manufactured panel supply will increase over the next 3–5 years, likely at prices that reflect CBAM protection and EU labour costs but not necessarily dramatically higher than market rates given scale effects.

Emergency Solar Permit Regulation and Permitting Acceleration

Slow permitting has consistently been identified as Europe’s largest bottleneck to solar deployment. In 2022, large solar projects in several EU member states faced average permitting timelines of 3–7 years — longer than the construction phase itself.

The Emergency Regulation (EU) 2022/2577

The Council adopted an emergency regulation in December 2022 that temporarily overrides normal environmental and planning procedures for specific solar categories:

Covered projects (3-month permitting cap):

- Rooftop solar on existing buildings (any size)

- Solar installations collocated with existing infrastructure (car parks, reservoirs, motorway verges)

- Repowering of existing solar plants

Covered projects (standard RAA timelines):

- Ground-mount solar in pre-designated Renewable Acceleration Areas

The regulation was extended through end-2026. After expiry, RED III’s 12/24-month caps take over permanently.

Renewable Acceleration Areas (RAAs)

RED III requires member states to designate RAAs — pre-screened areas where environmental impact assessments are conducted at the zone level rather than the project level. Within RAAs:

- Permitting maximum: 12 months

- Environmental screening: completed at designation stage (not repeated per project)

- Grid connection: coordinated by zone rather than individual application

RAA implementation status by country (2025–2026):

| Country | RAA Status | Notes |

|---|---|---|

| Spain | Advanced | Multiple zones designated, particularly Castilla-La Mancha and Extremadura |

| Germany | In progress | Länder implementing under Solarpaket I framework |

| France | Early stage | Decree in preparation; some solar zones pre-identified |

| Netherlands | Advanced | Integrated with existing zoning plans |

| Italy | In progress | Slow — complex regional governance |

Pro Tip — Target RAA Projects First

For new project development, check whether your target site falls within or near a designated Renewable Acceleration Area before commencing any other permitting steps. A project in an RAA can achieve full permitting in 12 months; the same project 10 km outside an RAA may take 3–5 years. The site selection decision is the most consequential permitting choice you will make.

One-Stop-Shop Portals

RED III mandates that member states establish a single administrative point of contact for renewable energy permitting — consolidating all approvals (environmental, grid, zoning, building) into one process with one timeline.

Implementation progress varies significantly:

- Germany: Bundesnetzagentur coordinating multi-agency single portal under Solarpaket I

- Spain: MITERD (Ministry for Ecological Transition) operating integrated renewable permit portal

- France: DREAL (regional offices) consolidating approvals under simplified solar permit procedure

- Netherlands: RVO (Netherlands Enterprise Agency) single portal for energy projects

Accurate technical layouts from solar design software are a prerequisite for one-stop-shop submissions — most portals require standardised yield reports, shadow analysis, and grid connection specifications in machine-readable formats.

EU-Wide Solar Policy Comparison: Country-by-Country

Every EU member state implements EU directives differently. The following table compares the five largest EU solar markets on key policy dimensions.

Country Policy Comparison — 2025–2026

| Policy Dimension | Germany | France | Spain | Italy | Netherlands |

|---|---|---|---|---|---|

| 2030 national solar target | 215 GW | 100 GW | 76 GW | 80 GW | 27 GW |

| Current installed capacity (end-2024) | ~90 GW | ~22 GW | ~30 GW | ~35 GW | ~25 GW |

| Feed-in tariff / premium | EEG FiT (8.11 ct/kWh ≤10 kWp) | Structured FiT (up to €0.10/kWh) | Net billing with credit rollover | Net billing + GSE incentive | SDE++ (feed-in premium via auction) |

| Primary support mechanism | EEG + KfW grants | CRE tenders + FiT | RETA auctions + net billing | GSE incentive auctions | SDE++ subsidy auctions |

| Permitting speed (large projects) | 6–18 months (improving) | 9–24 months | 6–18 months (RAA zones faster) | 18–48 months (slow) | 6–12 months |

| Rooftop mandate | Mandatory on new commercial buildings | Mandatory new commercial by 2027 | Mandatory certain buildings | In progress | >250 m² buildings from 2025 |

| Agrivoltaic programme | Yes — premium under EEG auctions | Yes — dedicated CRE tender category | Pilot programme | Emerging | Limited |

| Energy community framework | Mieterstrom / Bürgerenergiegemeinschaft | Communautés d’énergie renouvelable | Comunidades energéticas | Comunità energetiche rinnovabili | Energiegemeenschappen |

Germany

Germany’s solar policy is the most complex and subsidy-rich in Europe. The Erneuerbare-Energien-Gesetz (EEG) mandates 20-year guaranteed feed-in tariffs for all registered systems. Solarpaket I (2024) expanded balcony solar to 800W, simplified Mieterstrom, and cleared ground-mount permitting on additional land categories.

Germany’s 215 GW target requires approximately 22 GW per year through 2030. In 2024 Germany installed ~14 GW, indicating a significant acceleration requirement. The KfW 442 battery grant and Bundesländer programmes provide layered incentive support.

For the complete Germany solar subsidy guide, see solar subsidies Germany.

France

France’s solar policy centres on CRE (Commission de Régulation de l’Énergie) competitive tenders. The 100 GW 2030 target was updated in the 2024 NECP submission. Structured feed-in tariffs up to €0.10/kWh apply to rooftop systems under 100 kWp outside the tender system.

France has the most developed agrivoltaic policy in Europe. Dedicated CRE agrivoltaic tenders offer premium prices for dual-use installations, with France targeting 20 GW of agrivoltaic capacity by 2030. The French administration cut permitting time for small solar from 36+ months to under 9 months through a solar-specific e-permit system launched in 2023.

Spain

Spain’s combination of high irradiance, large land availability, and progressive permitting reform makes it Europe’s most attractive large-scale solar market in 2025–2026. The 74% renewable electricity target by 2030 requires continued rapid solar build-out.

Spain uses net billing with automatic credit rollover up to 12 months. RETA (Renewable Energy Tender) auctions allocate capacity for large-scale solar with long-term contracts. The government has pre-designated over 50 Renewable Acceleration Areas in southern regions.

The generation financial tool for Spanish solar projects should account for Spain’s regional irradiance variation — differences between Galicia and Andalucía can exceed 30% in annual yield.

Italy

Italy historically offered Europe’s deepest residential solar incentive via the Superbonus 110% programme. The Superbonus was restructured in 2023 and scaled back in 2024, though net billing and GSE (Gestore dei Servizi Energetici) auction incentives remain active.

Italy’s permitting system remains Europe’s most complex — the DIA (dichiarazione di inizio attività) and PAUR processes involve multiple agencies at national and regional level. Average permitting for large solar exceeds 36 months. Italy has designated some RAA equivalents (aree idonee) but implementation is uneven by region.

Netherlands

The Netherlands has the most aggressive rooftop mandate in Europe: mandatory solar on all buildings over 250 m² from 2025. The SDE++ (Stimulering Duurzame Energieproductie) auction system allocates subsidies to renewable energy projects through competitive tenders, with solar receiving the largest allocation in recent rounds.

Grid congestion is the Netherlands’ primary deployment bottleneck. Netcongestie (grid congestion) has forced moratoria on new connections in several regions. The government has mandated TSO and DSO investment programmes to address congestion, but resolution is expected to take through 2028 in some regions.

Anti-Dumping Duties on Chinese Solar Panels: History and Current Status

The EU’s history with solar trade measures is one of the longest-running trade policy disputes in renewable energy. Understanding this history matters for anticipating future policy, particularly as CBAM creates a new trade instrument.

Timeline of EU Trade Measures on Chinese Solar

| Period | Measure | Status |

|---|---|---|

| 2013–2018 | Minimum Import Price (MIP) + anti-dumping and anti-subsidy duties | Negotiated settlement; MIP set at €0.56/W |

| 2018–2021 | Measures expired after sunset review; no renewal | Expired |

| 2021–2023 | No anti-dumping duties; market monitoring active | No measures |

| Sept 2023 | Latest sunset review concluded — Commission chose not to reinstate duties | No measures |

| 2024–2026 | No anti-dumping duties in force on Chinese PV modules | No measures |

Current status: No EU anti-dumping duties apply to Chinese solar panels. The European Commission conducted a sunset review in 2022–2023 and concluded that reinstatement of measures was not in the EU’s interest, given the dependency on Chinese panels for achieving 2030 solar targets.

The EU solar manufacturing industry — represented by SolarPower Europe’s European manufacturers caucus — continues to advocate for trade protection, including potential CBAM coverage of solar panels and EU content requirements for subsidised projects.

The Ongoing Policy Debate

The core tension in EU solar trade policy is between two legitimate policy objectives:

Deployment speed: EU needs 60–80 GW of solar per year. European manufacturing cannot supply this at current scale. Restricting Chinese imports would slow deployment and increase costs — directly undermining Fit for 55 targets.

Industrial policy: The EU wants to maintain domestic manufacturing capability as a strategic asset. Permanent dependence on a single country for critical energy infrastructure is a security vulnerability.

CBAM is currently the policy instrument designed to resolve this tension — applying a carbon price signal that advantages lower-carbon production without imposing a blanket tariff that would reduce supply. Whether CBAM alone is sufficient to catalyse EU manufacturing scale-up is debated.

Key Takeaway — No Current Tariff Risk

European solar installers can currently source Chinese panels without anti-dumping duty exposure. The risk to monitor is CBAM expansion to cover PV modules — which would add a carbon-based cost rather than a punitive tariff. This is a different instrument with different magnitude of cost impact, but it should be modelled into 10-year project financial plans.

EU Solar Energy Strategy Milestones

The EU Solar Energy Strategy, published alongside REPowerEU in May 2022, set a detailed roadmap. Here is the progress against key milestones.

EU Solar Energy Strategy — Milestone Tracker

| Milestone | Target Date | Status (March 2026) |

|---|---|---|

| 320 GW EU solar capacity | End-2025 | Achieved — ~330 GW at end-2025 |

| 600 GW EU solar capacity | End-2030 | On track if deployment rate maintained |

| Emergency permitting regulation in force | December 2022 | Achieved |

| RED III in force | November 2023 | Achieved |

| Member states designate RAAs | By end-2024 | Partial — 60% of member states |

| One-stop-shop permitting portals live | By end-2025 | Partial — major markets operational |

| EU Solar Rooftop Initiative — commercial mandate | 2027 | Implementation tracking |

| 1 million solar installation professionals trained | 2027 | ~350,000 by 2025 (behind target) |

| 750 GW EU solar capacity | End-2030 | 420 GW still required |

The skills gap (only 350,000 of a targeted 1 million trained professionals by 2025) is emerging as a deployment constraint alongside permitting and grid. Labour costs are rising in solar installation across all major EU markets.

Grid Integration Policies Across the EU

Europe’s grid infrastructure was not designed for distributed, variable generation at the scale of the 750 GW target. Grid integration policy is evolving — unevenly — across member states.

Core Grid Integration Challenges

Bidirectional flow. Legacy distribution grids were designed for one-way flow from generation to consumers. High solar penetration creates reverse flows that existing grid infrastructure cannot manage without upgrades.

Curtailment. In high-solar regions (southern Spain, parts of Italy), grid operators are increasingly ordering curtailment because the grid cannot absorb output. Affected plants must reduce or stop generation. Spanish solar projects experienced curtailment rates of 5–15% in some southern regions in 2024.

Interconnection queues. Grid connection requests across the EU totalled over 1,500 GW by end-2024 — much of it solar. Queue management, wait times, and connection cost allocation are handled differently in each country, creating major project risk.

EU Grid Policy Framework

RED III grid connection provisions. Member states must ensure grid operators offer standardised connection procedures with written decisions within defined timelines (30 days for initial response on smaller systems).

ENTSO-E Ten-Year Network Development Plan. The European Network of Transmission System Operators for Electricity coordinates cross-border grid investment planning. The 2024 TYNDP identified €584 billion in grid investment requirements through 2030 — a scale of investment that has not yet been matched by actual financing commitments.

Distribution grid reform. The proposed EU Electricity Market Design reform (agreed 2024) includes provisions for proactive grid planning — requiring DSOs to plan for renewable connection demand rather than reacting to applications. This is a structural change to how grid investment is justified and financed.

Country Grid Integration Status

| Country | Key Challenge | Policy Response |

|---|---|---|

| Germany | DSO coordination, Smart meter rollout | Solarpaket I DSO obligations; §14a EnWG smart charging |

| Netherlands | Netcongestie — congestion moratoriums | Government-mandated TSO/DSO investment plan |

| Spain | Southern grid curtailment | MITERD curtailment cap pilot; transmission investment programme |

| Italy | North-south interconnection deficit | PNRR-funded transmission upgrades |

| France | Grid connection timelines | ENEDIS one-stop-shop for connections under 250 kW |

For projects where shading, orientation, and system design directly affect bankability of yield, solar shadow analysis software integrated with production forecasting tools is increasingly required by financiers for projects subject to grid curtailment risk — the difference between a P50 and P90 yield estimate matters significantly when curtailment is a realistic scenario.

State Aid, IPCEI, and EU Funding for Solar Storage

European solar projects can access multiple EU-level funding instruments beyond national subsidy programmes. Understanding these instruments is particularly important for commercial and utility-scale developers.

EU Innovation Fund

The EU Innovation Fund, financed by EU ETS auction revenues, funds low-carbon technology projects including solar + storage. Scale:

- Large-scale projects: Minimum €2.5 million in grant funding; typically 40–60% of eligible costs

- Small-scale projects: Simplified application for projects with €2.5–€7.5 million total cost

- 2024 large-scale call: €4 billion available; solar + storage projects were among top recipients

To be competitive, Innovation Fund applications require detailed financial models — including bankable yield projections from certified design tools and rigorous carbon abatement calculations.

Connecting Europe Facility (CEF Energy)

CEF Energy funds cross-border energy infrastructure including electricity interconnection projects. While not directly funding solar plants, CEF interconnectors reduce curtailment risk for solar-heavy regions and are a prerequisite for the 750 GW target being achievable.

Cohesion Funds and Recovery Plan for Europe (RRF)

The Recovery and Resilience Facility (€672 billion) required member states to allocate at least 37% to green transition. Solar has been a primary beneficiary across southern and eastern European RRF plans:

- Spain: €6.9 billion in RRF renewable energy investment

- Poland: €4.2 billion for renewable energy including solar

- Italy: €6.7 billion for renewable energy under PNRR

IPCEI for Hydrogen and Solar Storage

Important Projects of Common European Interest (IPCEI) allow coordinated cross-border state aid above normal thresholds for strategic value chains. IPCEI Hy2Tech and IPCEI Hy2Use (focused on hydrogen) include solar as a prerequisite feedstock. Dedicated IPCEI frameworks for battery storage — closely linked to solar self-consumption — are in development.

ROI and Financial Impact of EU Policy Changes

EU policy changes have direct financial consequences for solar project economics. Here is how the key policy levers translate into project numbers.

Carbon Price Impact on Solar Economics

Every €10/tonne increase in EU ETS carbon price:

- Increases gas-fired power generation costs by approximately €4–5/MWh

- Widens the spread between solar LCOE (typically €30–€50/MWh for utility-scale) and fossil generation

- Increases corporate PPA willingness-to-pay for solar power

At the current EU ETS price of €65–€75/tonne, solar is economically competitive with gas on pure levelised cost — without any subsidy. This structural shift explains why corporate PPA volumes in Europe reached record levels in 2024.

Impact of RED III Permitting Acceleration

| Project Phase | Pre-RED III Typical Timeline | Post-RED III (RAA) Target | Cost of Delay |

|---|---|---|---|

| Permitting (large ground-mount) | 3–5 years | 12 months | €200–€500k/year (financing cost) |

| Grid connection study | 6–18 months | 30 days (initial response) | Variable |

| Total development timeline | 4–7 years | 2–3 years | Significant IRR improvement |

Reducing the development timeline from 5 years to 2 years improves project IRR by 2–4 percentage points for typical utility-scale solar — one of the most valuable policy benefits of RED III permitting reform.

CBAM Cost Scenarios for Commercial Solar Projects

| CBAM Scenario | Impact on 500 kWp Project Cost | Probability |

|---|---|---|

| Current (aluminium/steel only) | +€6,000–€19,000 | Certain (current policy) |

| CBAM expanded to include modules (Chinese origin) | +€45,000–€140,000 | Medium (Commission reviewing) |

| CBAM + MFN carbon tariff | +€80,000–€200,000+ | Low (2028+ scenario) |

The middle scenario — CBAM expansion to include solar panels — is the key variable for 2026 project financial models. Projects with 20-year PPAs signed in 2026 may operate under materially different import cost conditions by 2030 if CBAM expansion proceeds.

Model EU Policy Scenarios in Your Solar Proposals

SurgePV’s generation and financial tool lets you model REPowerEU targets, RED III permitting scenarios, CBAM cost assumptions, and country-specific incentive stacking — so your commercial proposals reflect current EU policy accurately across any European market.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

How to Stay Compliant and Competitive in 2026

European solar policy creates both compliance obligations and competitive opportunities. Installers and EPCs who understand the policy environment ahead of their clients, and ahead of their competitors, consistently win more work.

Build a Policy Monitoring System

The EU solar regulatory environment now changes faster than annual policy reviews can track. A practical monitoring system for a European solar business should include:

Primary sources (check monthly):

- EUR-Lex — official EU legislation, implementing acts, and Commission decisions

- European Commission Energy DG — RED III implementation, NECP assessments

- SolarPower Europe — industry policy tracking, statistical reports

- National regulator websites (BnetzA for Germany, MITERD for Spain, CRE for France)

Secondary sources (quarterly review):

- IRENA — renewable energy policy data, financial market trends

- IEA Renewables — deployment statistics, policy effectiveness analysis

- ENTSO-E TYNDP updates — grid connection capacity forecasts

Integrate Policy Into Proposals and Project Design

The most effective way to respond to EU policy complexity is to systematically incorporate policy variables into your project workflow:

- Site selection: Cross-reference candidate sites against national RAA designations before investing in feasibility studies

- Financial modelling: Build CBAM cost assumptions into long-term project financial models

- Supply chain: Document carbon intensity of panel and component suppliers for CBAM reporting readiness

- Grid connection: Engage DSOs early — 30-day response mandates under RED III give you legal leverage that didn’t exist before 2023

- Proposals: Use solar proposal software that enables policy scenario modelling so clients see accurate ROI under current and projected regulatory conditions

Track Permit Zone Designations by Country

Each country’s RAA designation process is moving at different speeds. The practical opportunity is to identify candidate sites that fall within, or immediately adjacent to, zones likely to receive RAA designation — and position development activity there.

Key RAA tracking resources:

- Germany: Bundesnetzagentur renewable energy zone maps

- Spain: MITERD accelerated zone portal

- France: DREAL regional GIS layers for solar development zones

- Netherlands: RVO energy zone viewer

Use the Right Software Tools

Solar design software that integrates EU policy variables — RED III permitting timelines, national FiT rates, CBAM cost scenarios, country-specific grid connection procedures — enables your business to produce bankable proposals faster and with greater accuracy than competitors working from outdated spreadsheets.

The combination of solar shadow analysis software for accurate site yield modelling and generation financial tools for policy-aware ROI modelling is the minimum toolset for competitive project development across EU markets in 2026.

Conclusion

European solar policy in 2025–2026 is simultaneously the most supportive and the most complex it has ever been. The 750 GW target, RED III permitting acceleration, REPowerEU funding streams, and record EU ETS carbon prices all push in the same direction — toward faster, cheaper solar deployment.

The complexity comes from the diversity of implementation across 27 member states, the CBAM mechanism reshaping import economics, and the grid integration challenge that no amount of policy can solve without physical infrastructure investment.

For European solar businesses, the three most time-sensitive actions in 2026 are:

- Identify and target Renewable Acceleration Area projects — the permitting time differential between RAA and non-RAA sites (12 months vs. 3–5 years) is the biggest single variable in project economics

- Audit your supply chain for CBAM exposure — aluminium and steel obligations are live now; panel-level CBAM could arrive in 2026–2028

- Build country-specific policy accuracy into proposals — clients across all EU markets increasingly expect proposals that reflect current regulatory reality, not generic European averages

The solar businesses that grow fastest in Europe over the next five years will be those that treat policy knowledge as a competitive asset.

For country-specific deep dives, see our guides to European solar incentives and solar subsidies in Germany.

Further Reading

Explore our EU Solar Policy guide for the latest regulatory updates and market analysis.

Frequently Asked Questions

What is the EU solar capacity target for 2030?

The EU’s combined REPowerEU and Fit for 55 framework sets a 750 GW solar capacity target by 2030, up from approximately 260 GW at end of 2024. This requires deploying roughly 60–80 GW of new capacity annually through the decade, a pace Europe reached for the first time in 2023.

What is CBAM and how does it affect solar panels?

CBAM (Carbon Border Adjustment Mechanism) applies a carbon cost to imports of carbon-intensive goods entering the EU. Solar panels are not yet in the first CBAM product list (steel, cement, aluminium, fertilisers, electricity, hydrogen), but the European Commission is reviewing expansion to cover photovoltaic modules. During the current 2023–2026 transition phase, importers must report embedded carbon. Full financial obligations begin in 2026. Solar installers sourcing panels from China should monitor CBAM expansion announcements closely.

What are the current EU anti-dumping duties on Chinese solar panels?

The EU anti-dumping and anti-subsidy measures on Chinese crystalline silicon PV modules expired in September 2023 after the European Commission chose not to renew them following a sunset review. As of 2025–2026, there are no EU anti-dumping duties in force on Chinese solar panels, though CBAM and Minimum Import Price debates continue.

What is the EU Renewable Energy Directive 2025 (RED III)?

RED III (Renewable Energy Directive III), agreed in late 2023 and transposing into national law through 2025, raises the EU-wide renewable energy target to 42.5% by 2030 (up from 32% under RED II), with an aspirational target of 45%. It introduces a 12-month permitting deadline for solar in Renewable Acceleration Areas and mandates solar on new commercial buildings by 2027.

What is REPowerEU and what are its solar targets?

REPowerEU is the European Commission’s plan to reduce dependence on Russian fossil fuels, launched May 2022. It raises the 2030 renewable target to 45% and sets a solar-specific target of 600 GW by 2030. Combined with Net Zero Industry Act manufacturing goals, the effective headline target became 750 GW including rooftop and utility mandates.

What does Fit for 55 mean for solar energy in Europe?

Fit for 55 is the EU legislative package to reduce net greenhouse gas emissions by 55% by 2030 compared to 1990. For solar, it drives the renewable energy target upward via RED III, reforms the EU ETS to increase carbon pricing pressure, and funds solar deployment through the Innovation Fund and Social Climate Fund. Higher carbon prices make solar economics progressively stronger relative to gas-fired generation.

Which EU countries have the strongest solar policies in 2025–2026?

Germany leads on policy complexity and subsidy depth (EEG, KfW 442, Solarpaket I). Spain leads on deployment speed and permitting acceleration (74% renewable electricity target). Italy offers deep residential incentives historically (Superbonus) and strong auction volumes. Netherlands has mandatory rooftop solar for buildings over 250 m². France is expanding agrivoltaic and floating solar with structured feed-in tariffs.

How should European solar installers respond to EU policy changes in 2026?

Solar installers should: (1) track RED III permitting acceleration zones in their country — faster approvals reduce carrying costs; (2) monitor CBAM expansion announcements and diversify panel supply chains proactively; (3) use solar design software that integrates country-specific financial models so proposals reflect current policy accurately; (4) engage energy community frameworks for commercial and community projects eligible for new EU funding streams.